With greater focus on Canada’s grocery giants’ profits amid the pandemic and stubbornly high inflation, it’s important to ask: are grocery stores really doing that well? TLDR: Yes, but so are food manufacturers. Farmers, not so much.

Last week, Loblaws and Metro promised to freeze prices on their house brands through the holiday season. The thing is that this seems to be common practice every year in the industry.

To boot, the Competition Bureau is initiating a study of rising grocery store prices. Unfortunately, it’s only a “study”, not an “investigation” and, as such, the bureau can’t compel additional data from companies; it can only ask very nicely.

This is unlike the Federal Trade Commission in the U.S., which can compel additional private information for its studies. Also, the Competition Bureau is only studying grocery stores, which is a fairly myopic view of food prices. Food price hikes can just as easily be caused by food manufacturers or farmers, as well as grocery stores, as we’ll see below.

Profits: up, up and away

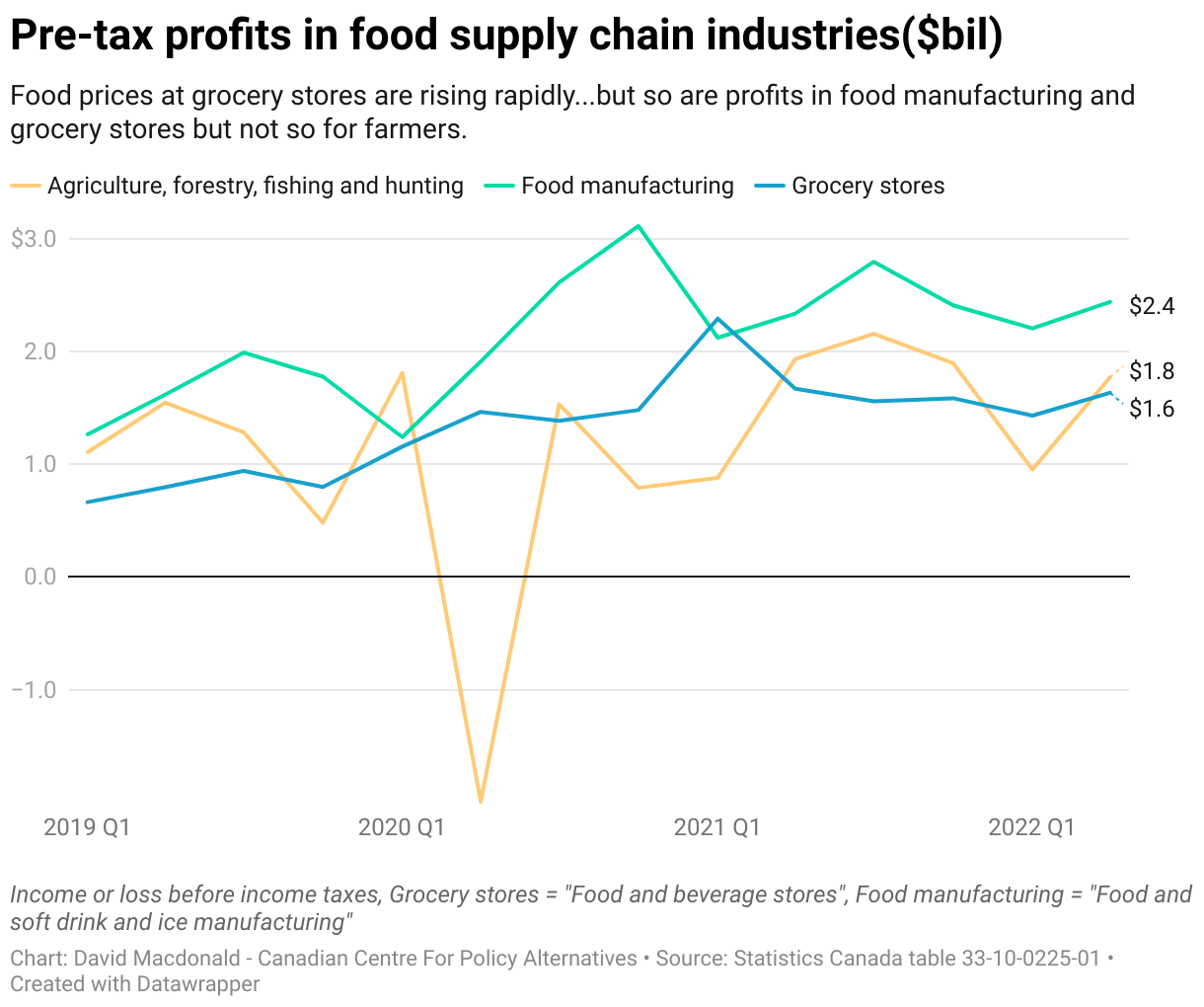

In the first two quarters of 2022, grocery stores made an average $1.5 billion. That’s roughly twice as much as their pre-pandemic profits ($800 million, on average, a quarter in 2019).

In the chart below you can see an uptick in profits (income before income taxes) by quarter after the pandemic lockdowns for food and beverage stores (grocery stores), food and soft drink and ice manufacturing, as well as agriculture, forestry, fishing, and hunting (farmers).

For the first two quarters of 2022, food manufacturers’ average profits reached $2.3 billion a quarter—much higher than the average $1.7 billion a quarter in profits in 2019.

Interestingly, grocery stores seem to have managed to yield particularly high profits in the first quarter of 2021, when they hit an all-time high, largely at the expense of food manufacturers. The manufacturers took a hit that month, although that didn’t last, as they likely caught up with inflation and managed to raise their prices to grocery stores to capture some of it.

A margin here, a margin there

Perhaps more importantly than profits going up is that profit margins also went up. (You’d expect profits to go up over time, just due to population growth and a growing economy).

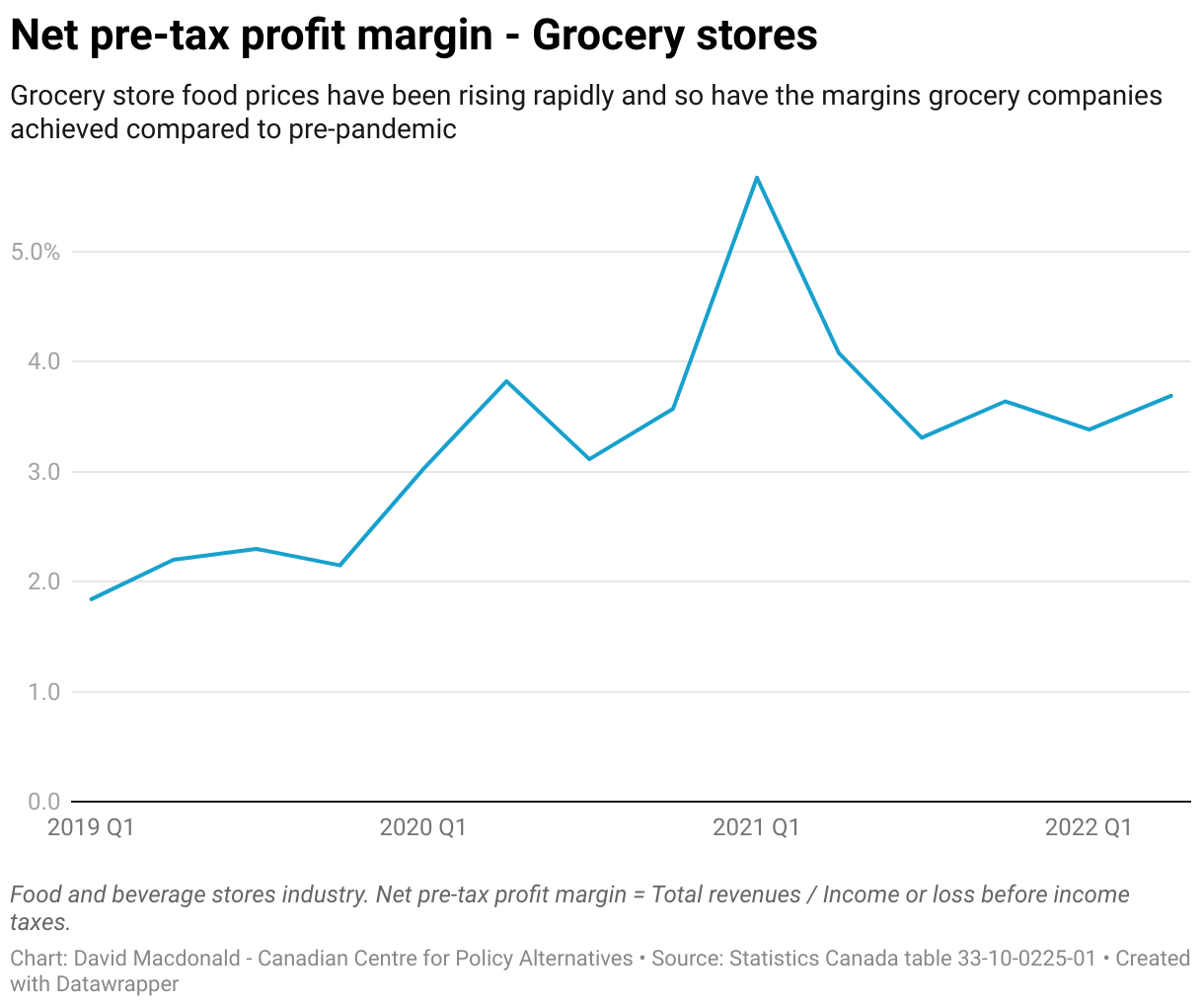

Pre-pandemic profit margins for the grocery store industry were in the 2% to 2.5% range, but they shot up when the pandemic started to hit a high of almost 6% in the first quarter of 2021. This is actually an all-time high for this data series, which goes back to 2010. They have since come down a bit, to 3.5% for the past year or so, but this is well above the 2%-2.5% range where they stood before the pandemic hit.

The industry is fond of saying that groceries are a low-margin business, ie. the margins are under 5%, which is generally the case. But since the pandemic, they’ve almost doubled those margins. Just because it’s low margin doesn’t mean you can’t turn a profit.

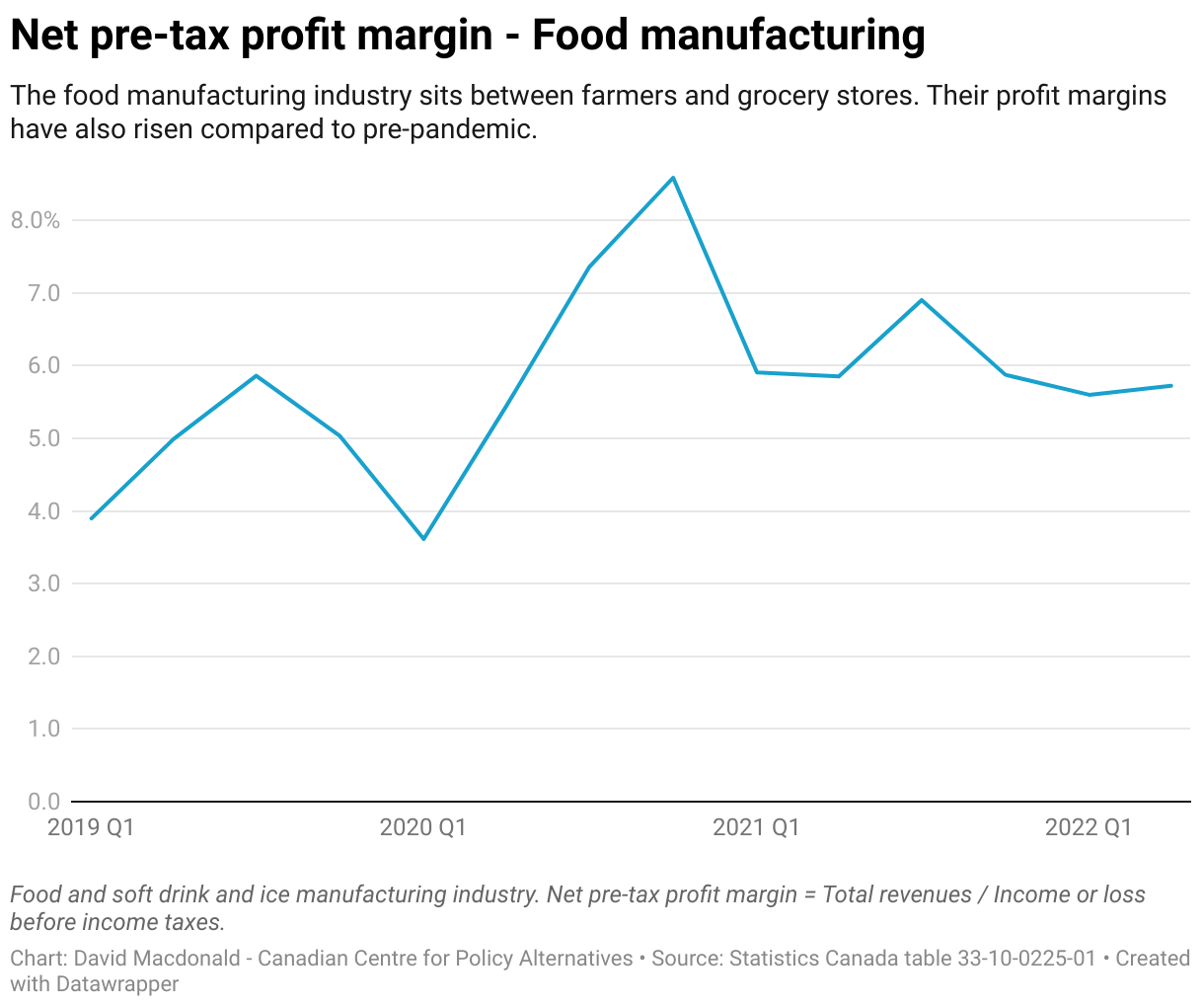

It’s a similar story for food manufacturers, although their margins are a bit more volatile quarter to quarter. Average margins for food manufacturers stood at 4.9% in 2019, before the pandemic. They hit an all-time high of 8.6% in the fourth quarter of 2020, but margins have since settled down to an average of 5.7% for the first two quarters of 2022. Margins are certainly higher now than pre-pandemic, but not by quite as much as the grocery store industry.

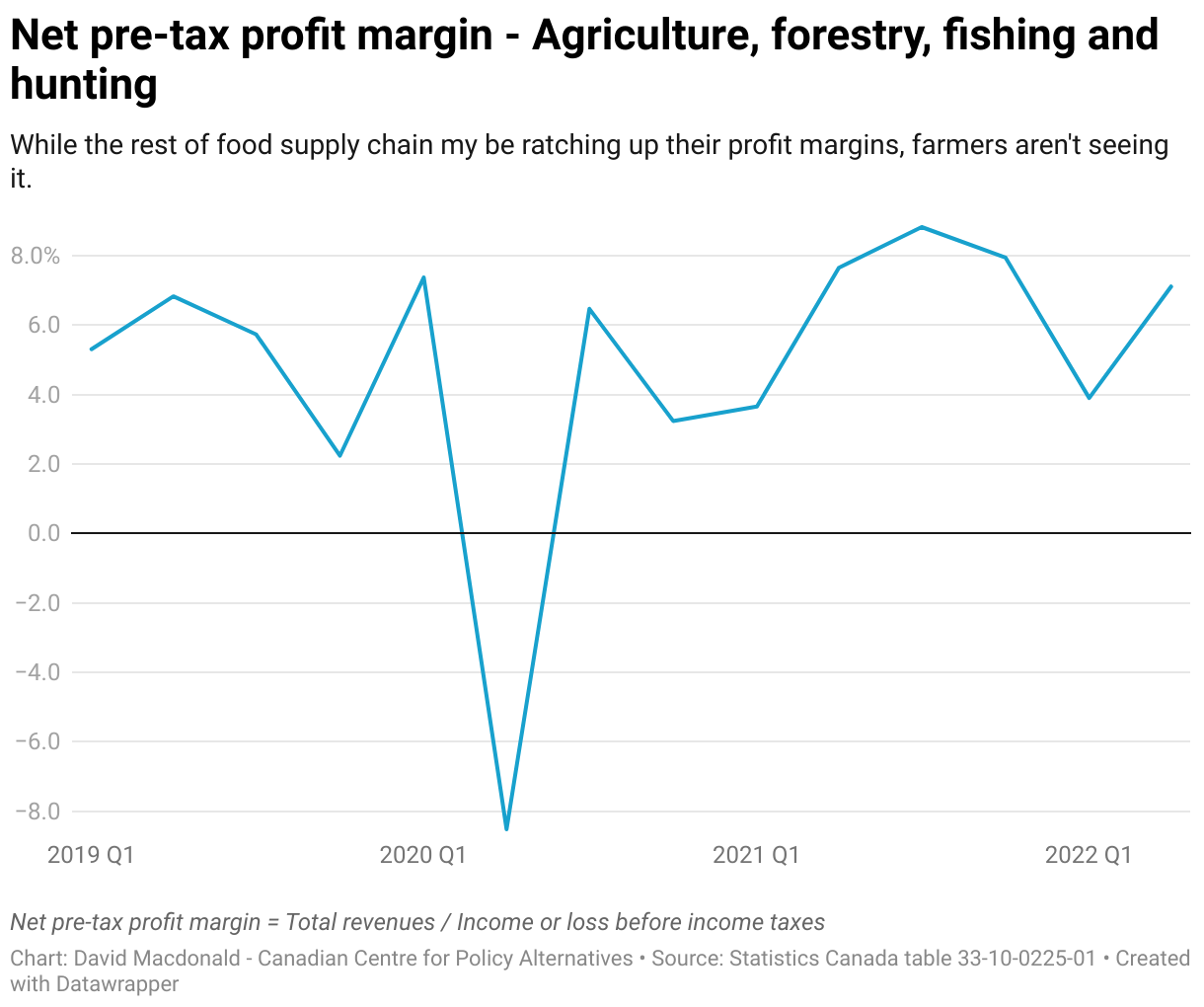

The financial reality has been decidedly worse for the agricultural industry (which includes forestry, fishing, and hunting): as with profits, margins plunged at the start of the pandemic and have been quite volatile, with no clear trend. In 2019, average profit margins were 5% and they were 5.5% for the first two quarters of 2022.

What does this tell us about who’s winning and who’s losing in the food profit industry? Of the three sectors represented in the data, it’s certainly not farmers who are winning. Food manufacturers are certainly benefitting and have higher profit margins. They are seeing higher absolute profits. On a relative basis though, grocery stores are benefitting the most, based on their change in profit margins.

Some context

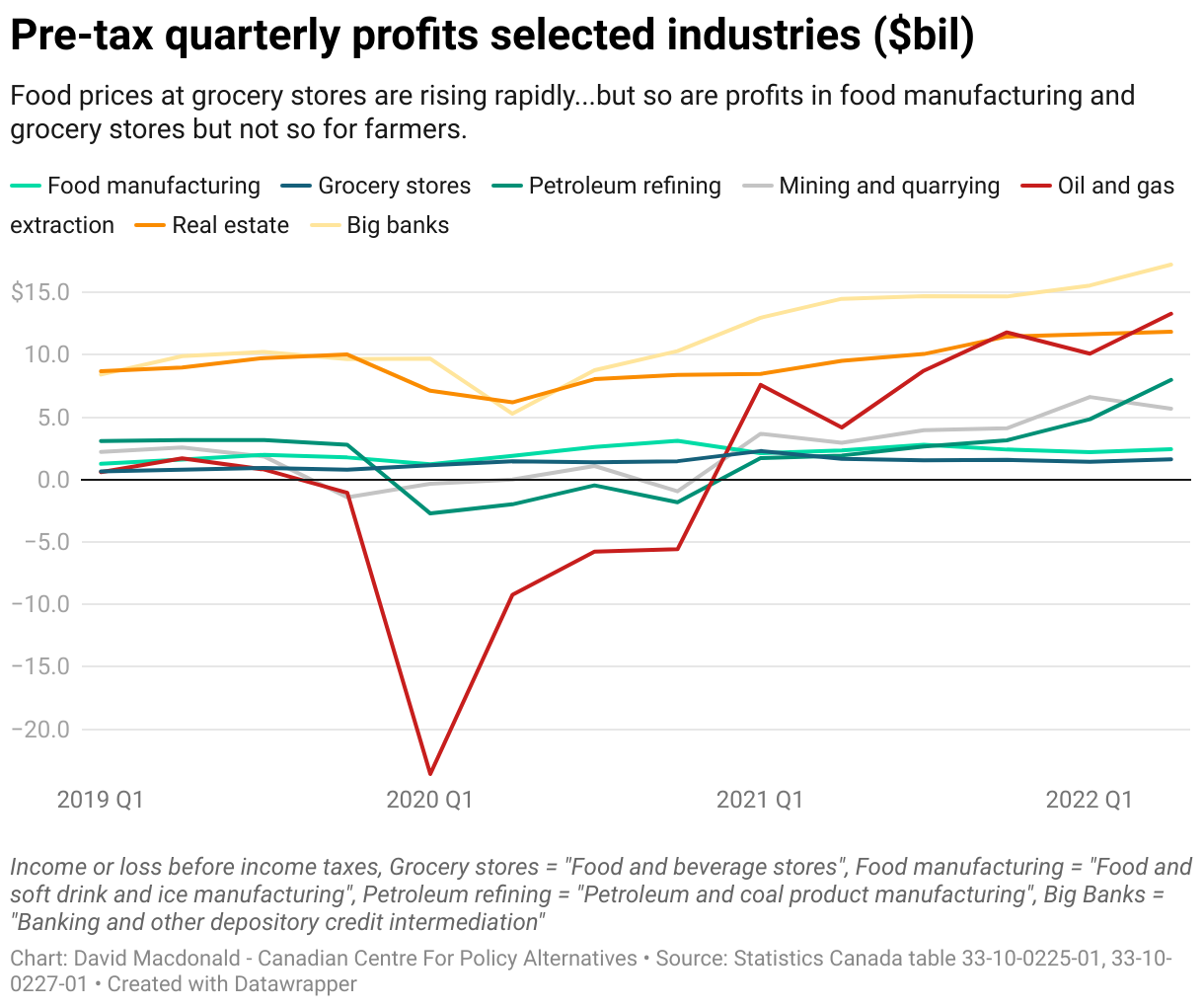

While this analysis is about food prices and food supply chain profits, this is really the tip of the iceberg. Compared to the big players (oil, banks, real estate, mining), profits in grocery stores and food manufacturers is like sitting at the kids table. Oil extraction and oil refining companies are making “…more money than god”—although Canada’s big banks top them. Real estate profits are not too shabby either (although that’s likely to end soon).

Almost everyone in corporate Canada is banking profit, unlike almost all Canadians who are paying for it in higher prices.

If the federal government is looking to expand the national excess corporate tax to sectors beyond banking, grocery stores (along with oil & gas, mining, real estate) are obvious candidates.