Canada is expanding public health coverage to dental care—but it’s not universal.

Executive summary

As part of the March 2022 Liberal-NDP Supply and Confidence Agreement, the federal government is creating a national public dental care plan—the most significant expansion of public health care in decades. This new plan holds the potential to fill a tremendous need: An estimated 12.9 million Canadians do not have dental insurance (either public or private); 1.2 million of them are children under the age of 12. However, this analysis shows that the current dental plan will fall far short of the need.

This new federal insurance plan is unfolding over three distinct phases between 2022 and 2025. No matter the phase, only families making under $90,000 will be able to access the insurance, creating a real barrier to access dental services.

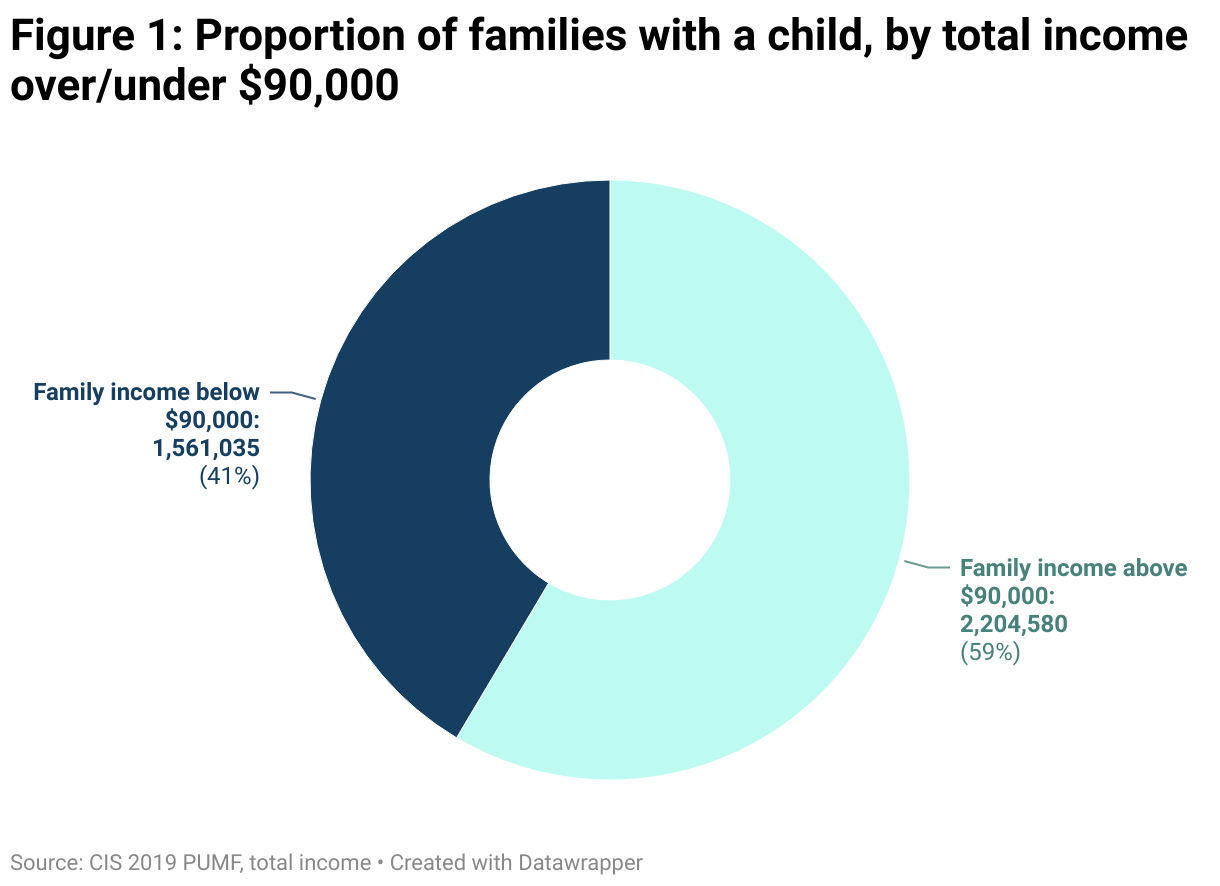

A family income of $90,000 annually for families with children isn’t unusual in Canada: 59 per cent of families with children made over $90,000 in 2019, amounting to 2.2 million families. Earning $45,000 for each parent isn’t a tremendous salary in Canada. But making more than that precludes those families from receiving federal dental care coverage.

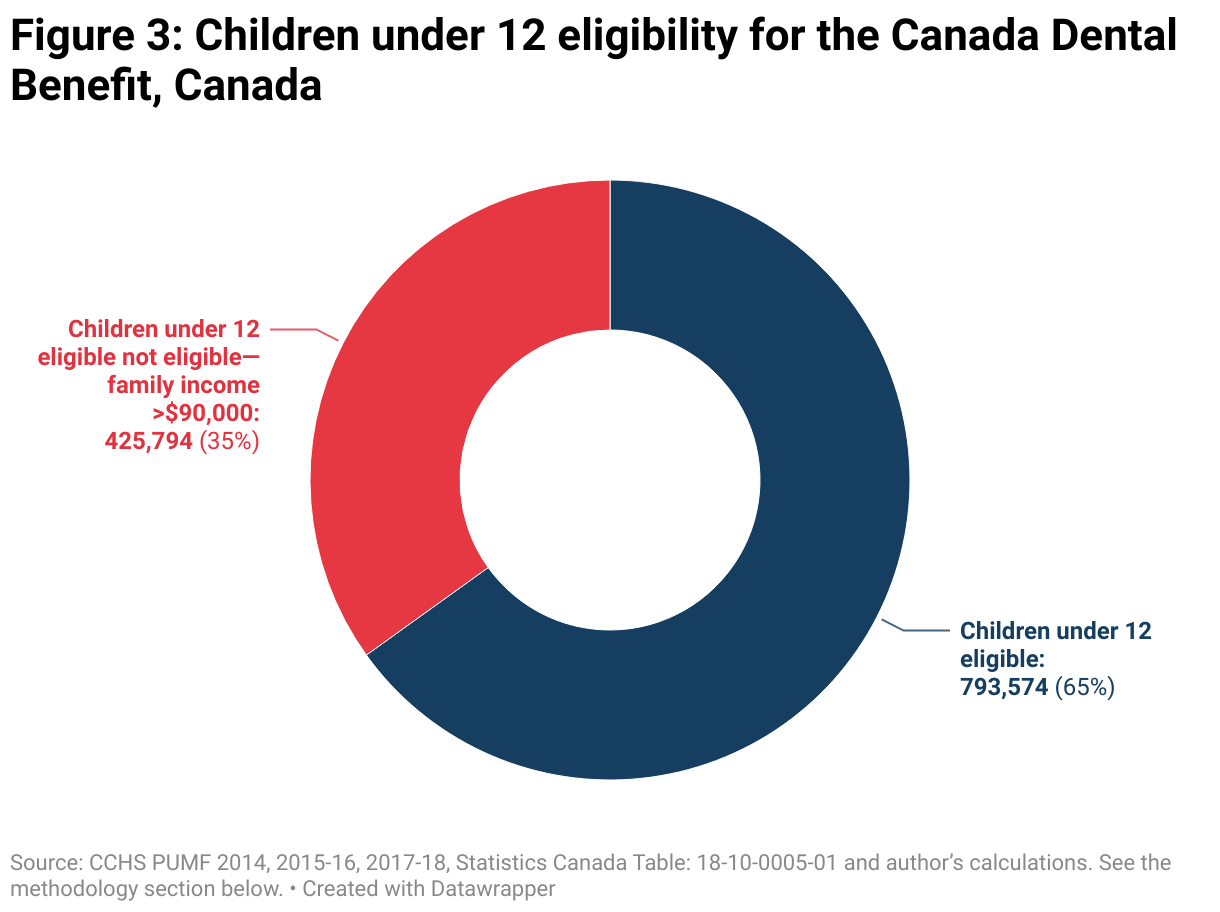

The first phase, underway through to June 2024, is called the Canada Dental Benefit (CDB). It’s a cash transfer of $1,300 a child if that child sees a dentist; 65 per cent of children under 12 without other dental insurance—794,000 young children—could get the $1,300 transfer. 382,000 young children have actually received support so far. However, 35 per cent—426,000 young children—without dental insurance cannot access it because their families make over $90,000.

In phases two and three, the dental plan changes from cash transfers to an actual insurance plan and expansion of Canadians who are eligible for the plan.

Phase two, now named the Canada Dental Care Plan (CDCP), is actual insurance. This second phase covers not just young children, but any children under 18, seniors and people with disabilities. It has just started in 2024.

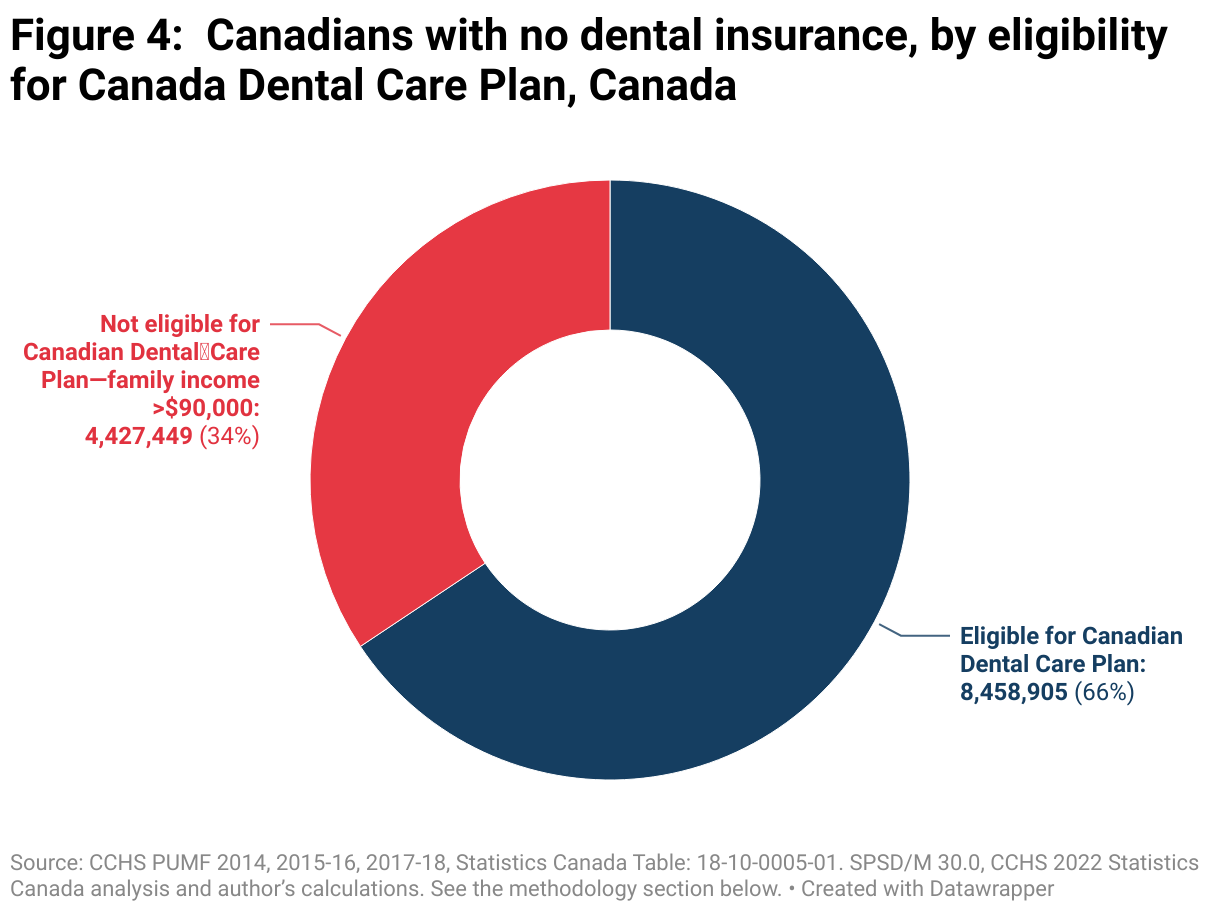

In phase three, the only eligibility restriction is the $90,000 family income cap and the lack of other dental insurance. Phase three of the CDCP will cover 8.5 million people but will leave another 4.4 million out of the plan due to the income restriction. A further 1.4 million people might have their inadequate provincial public dental insurance supplemented by the new federal plan. Upon full implementation, 9.8 million people will either gain dental insurance or have it supplemented by the CDCP.

It would cost an estimated $1.45 billion on top of the $3.3 billion presently budgeted for the 2025-26 year to include the people without dental insurance who won’t qualify for the CDCP.

Our content is fiercely open source and we never paywall our website. The support of our community makes this possible.

Make a donation of $35 or more and receive The Monitor magazine for one full year and a donation receipt for the full amount of your gift.

The choice is twofold: (1) Continue to create new medical care programs with a fill-in-the-gaps model and an income cap, like Canada is currently doing on dental care, or (2) Align new medical care programs with the principles of the Canada Health Act, which is based on the underlying principle of health care for all.

The findings in this analysis of Canada’s nascent national dental care plan might also be relevant to the much anticipated announcement of a national pharmacare plan. Income restrictions could leave millions of Canadians out of both plans while a universal program would align with the principles of the Canada Health Act—everyone should be eligible for these programs.

Introduction

A new commitment to public dental insurance was one of the key parts of the March 2022 Supply and Confidence Agreement between the NDP and Liberal parties. This new form of insurance is unfolding over three distinct phases between 2022 and 2025.

At each phase, the categories of who receives dental care coverage expand to cover more people. However, some of the basic design elements remain the same when it comes to considering who is excluded from this plan. Canada’s new dental care plan only covers Canadians who aren’t insured through an existing private plan or who are poorly covered by a public plan (Appendix 1 provides a discussion of the interaction between existing provincial fill-in-the-gap dental programs and the new federal plan). There are also family income restrictions: if a family makes below $90,000 annually, it gets coverage with co-payments; a family whose income is below $70,000 annually gets coverage without co-payments. All families whose income is over $90,000 a year will be left out of all phases of the new federal plan—even if they aren’t currently covered by a dental insurance.

Across the three phases, eligibility differs, but it retains those basic criteria.

Phase one: In the first phase, the plan is called the Canada Dental Benefit (CDB). Children under 12 years of age are the intended recipients for this phase. This was initially meant to be an insurance plan, but, likely due to an implementation schedule that was too ambitious, it was rolled out as a straight cash transfer. It had two application periods and a family could receive $650 per child under 12 years in each period. The first period ran from December 1, 2022 to June 30, 2023 and the second runs from June 30, 2023 to June 30, 2024. If a family makes under $90,000 and the child received dental care in Canada, they received a flat $650 a period or a possible maximum of $1,300 over both periods. This cash transfer is irrespective of the actual dental costs incurred in a particular period. If dental expenses exceed $650, an additional payment is possible. At the time of writing, phase one is nearing completion, with 382,000 children benefiting.

Phase two: The second phase, called the Canada Dental Care Plan (CDCP), will come in the form of actual insurance, where the program will directly pay dental clinics for expenses incurred, in contrast to the flat amount from the CDB in phase one. Dental coverage appears to be similar to what the federal government already provides through its Non-Insured Health Benefit program (NIHB). The NIHB provides health benefits (including dental) to First Nations and Inuit clients. In the case of the CDCP, it will be provided by the private insurance provider Sun Life. By the end of 2024, the CDCP will have phased in coverage for people with disabilities, children under the age of 18, and seniors—although only for those without private dental insurance and whose family income is below $90,000.

Phase three: Stage three will commence in 2025 and the plan will keep its name as the Canada Dental Care Plan. However, in 2025, it will expand to everyone without private dental insurance whose family income is below the $90,000 limit.

In short, the Canada Dental Care Plan is a “fill-in-the-gaps” approach to improving access to dental care and only focuses on providing coverage for people who have no private dental insurance and whose family doesn’t make over $90,000. There is no effort by the government to take over the private dental care system and more actively control costs. There is no move to remove out-of-pocket expenses for all Canadians, as is the case with universal health care. This is purely an application-based program that fills in dental insurance for those under a certain income level. It is not universal.

There are more impediments to accessing dental care in Canada than just the lack of private insurance. Many communities do not have an adequate dental workforce to meet the population’s needs, something Medicare would attempt to address but the CDCP doesn’t. Also, many people with private coverage may still lack access to care due to high out-of-pocket expenses. There is also a complete lack of regulation of private coverage in Canada, so the quality of coverage varies significantly; the CDCP doesn’t address this.

Nonetheless, this is one of the most important expansions of health care coverage by the federal government in decades. In contrast to almost all other health care programs, outside of First Nations communities and the military, it is entirely governed by federal policy, with no provincial involvement, which is a rarity in Canadian health care policy.

One of the other unique and concerning features is the income requirement. No other part of public health care is restricted by income. There is no situation in Canada where you go to a hospital or visit a doctor in Canada and you pay for treatment out-of-pocket if your family makes too much. The Canada Health Act is clear on this point: “It is hereby declared that the primary objective of Canadian health care policy is to protect, promote and restore the physical and mental well-being of residents of Canada and to facilitate reasonable access to health services without financial or other barriers.”

The income restriction, as we’ll see, creates a meaningful, and under-studied, barrier to access dental services. A family income of $90,000 for families with children isn’t unusual in Canada. As shown in Figure 1, 59 per cent of families with children made over $90,000 in 2019, amounting to 2.2 million families. They won’t have access to new federal dental care coverage. Of course, higher earners are more likely to have employer-sponsored dental insurance. Families with children generally make more because they are more likely to be made up of two adults. Earning $45,000 for each parent isn’t a tremendous salary in Canada. But making more than that precludes those families from receiving federal dental care coverage.

The goal of this analysis is to determine how many people don’t have dental insurance but are nonetheless left out of the federal dental insurance plan at each phase of implementation. The Canada Community Health Survey (CCHS) asks Canadians about their dental care insurance coverage. The most recent Statistics Canada analysis of the 2022 CCHS data provided useful estimates of the population over age 12 without dental insurance at different income levels. It does not include any estimates for children under age 12. These percentages are used to calculate the count of Canadians covered by the CDCP in its final stage.

Several recent studies have examined the question of dental insurance coverage. The CD Howe 2018 study utilized the 2013-14 CCHS PUMF to examine coverage rates in Ontario for those 12 and older. Zivkovic et al. 2020 used the same PUMF to estimate the impacts of better insurance for those 12 and older in Ontario. Statistics Canada in 2018 reported that 64.6 per cent of Canadians over the age of 12 had dental insurance of some kind. More recently, the Parliamentary Budget Office (PBO) costed out some versions of the phases below to check federal cost calculations. Although it did use the 2013-14 CCHS PUMF in some of their calculations, it used a variety of other private sources as well. The PBO did not estimate how many people without insurance would be excluded from new federal dental programs due to the $90,000 income cap. An inquiry to the Ministry of Health 2023 estimates the beneficiaries of the CDCP in phases two and three. These provide comparable estimates to those calculated below for likely beneficiaries. However, those who remain uncovered are not calculated, nor are those who might see their provincial dental insurance supplemented.

This analysis includes all Canadians without dental insurance, including those under age 12, something missing in all prior analysis on this topic. It provides specific counts of who’s in and who’s out. It also estimates the count of people who are receiving provincial government dental insurance that may be supplemented by the CDCP.

Note that the calculations below are calculating eligibility, not take up. This is an application-based program; if you don’t apply, you don’t get it, even if you’re eligible. The application approach applies to all three phases. So the number of people benefiting from this new federal program will be less than the number of people who are eligible for the program, as calculated below. Initial take up rates for the CDB have been problematically low in phase one, as outlined elsewhere.

There are an estimated 12.9 million Canadians who do not have dental insurance (either public or private). There are an additional 1.4 million Canadians who receive dental insurance through provincial government fill-in-the-gaps programs. In phases two and three, the federal plan will supplement provincial programs, which often provide quite poor coverage. A full discussion can be found in the Appendix.

Phase one: Coverage for children under 12: December 2022-June 2024

As noted above, phase one runs through June 2024. The total benefit is $1,300 a child under 12, in two rounds of $650 each. This is not insurance, it’s a cash transfer to families who have seen a dentist in Canada during the eligible time frame. Of the 12.9 million people who do not have dental insurance, 1.2 million are children under 12.

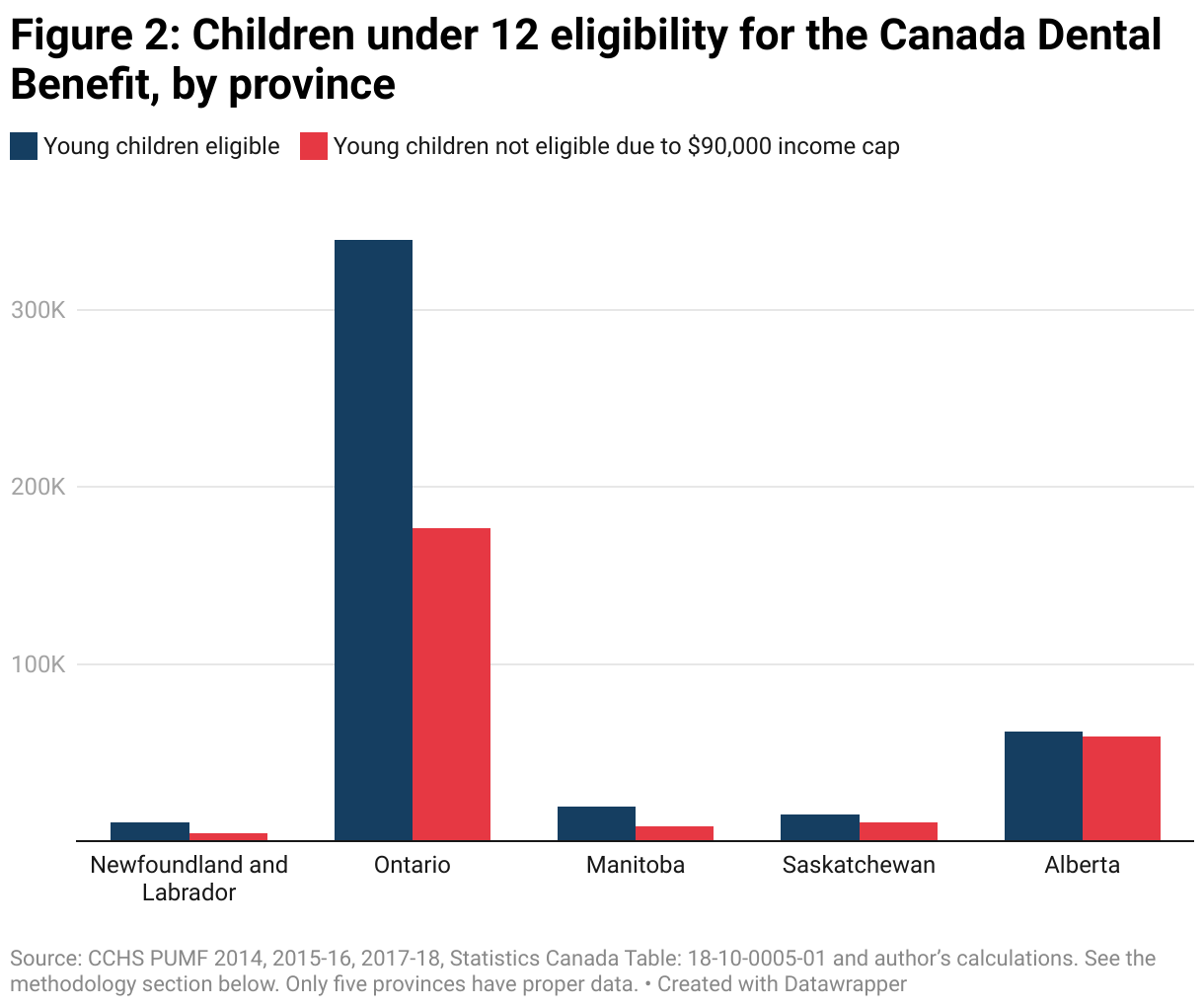

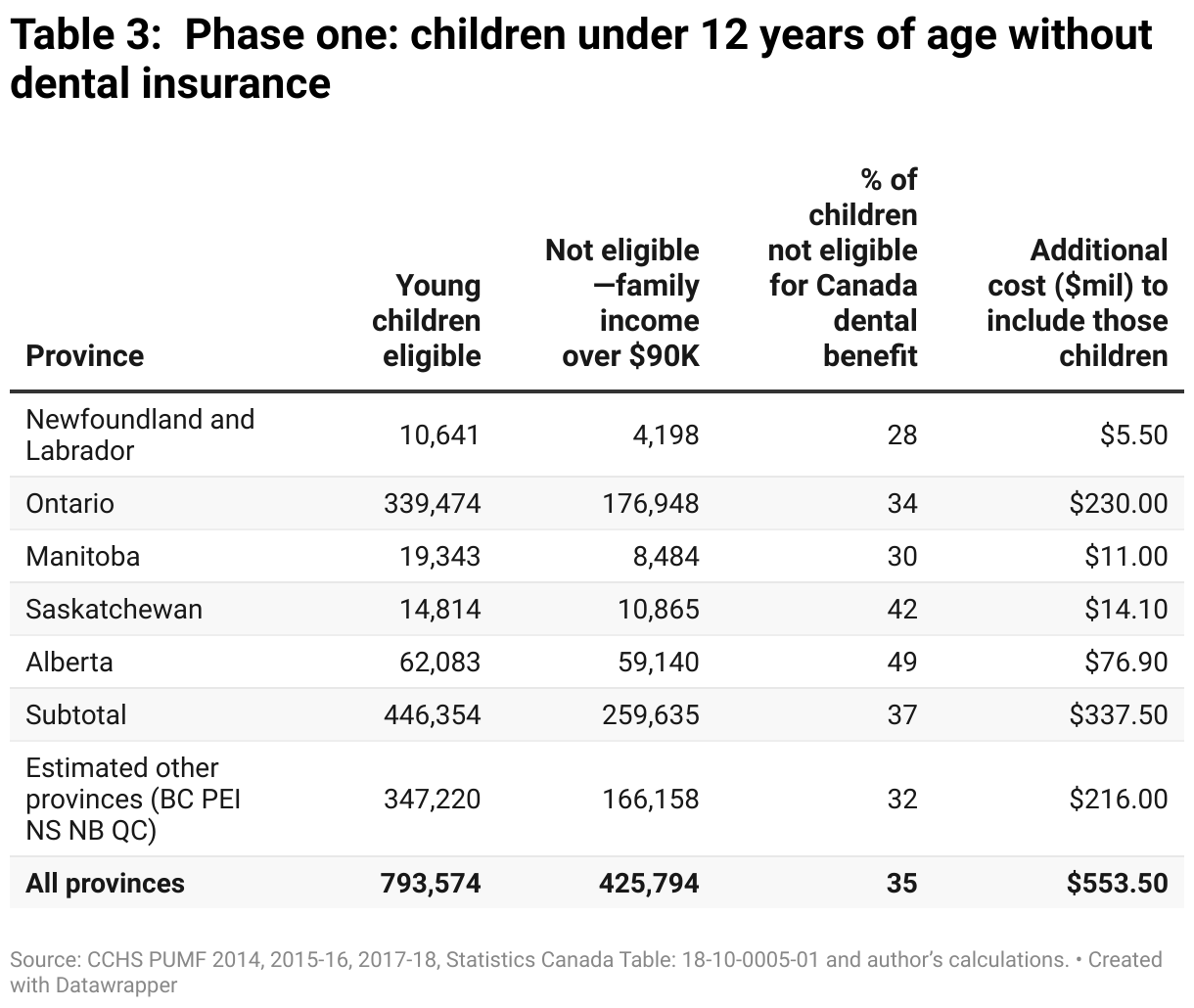

Unfortunately, detailed data is only available in five of 10 provinces. Due to the income cap, ineligibility rates vary substantially by province, as shown in Figure 2, from a low of 28 per cent and 30 per cent, respectively, for Newfoundland and Labrador and Manitoba to a high of just under half of families with young children in Alberta. In other words, 49 per cent of families with young children in Alberta that don’t have dental insurance aren’t eligible for the existing Canada Dental Benefit because their family income is over $90,000.

Various factors will be behind varying ineligibility rates. The most important one is likely the income restriction itself. Incomes are higher in Alberta compared to Newfoundland and Labrador, so it simply is more likely that the average family hits the $90,000 threshold in Alberta but not in Newfoundland and Labrador. Different industries and unionization rates impact the provision of workplace insurance. The mix of these varies by province. Also, the availability of provincial government-provided dental insurance will change the counts.

Provincial governments provide various types of fill-in-the-gaps dental insurance, although with varying criteria. For example, Nova Scotian children aged 14 and under without private insurance are automatically enrolled in the province’s Children’s Oral Health Program, where they do not face out-of-pocket expenses unless it is for a non-covered procedure like braces. This means fewer children will need to apply for the federal benefits in Nova Scotia. By comparison, in Ontario, children in families with income below $26,551 can apply for the province’s Healthy Smiles program. Therefore, more Ontario children will need to apply to the federal plan.

If we assume that there is a similar proportion of young children in households making over $90,000 and don’t have dental insurance in provinces without data, we can obtain the national estimates (see Figure 3). In the CDB, which is currently available to Canadians, 65 per cent of children under 12, but without dental insurance, could get the $1,300 transfer. However, this also means that 35 per cent, or 426,000 young children, without dental insurance could not access the CDB because their families made more than $90,000.

Phase one is almost complete. If the federal government wanted to extend the CDB to all families with young children who don’t have dental insurance, it would cost an estimated $554 million more a year (see the methodology). This is based on a 100 per cent take up rate. As such, this estimate may be better presented as an upper bound since the coverage rate, so far, seems much less than 100 per cent.

Phase two: Children, seniors or those with disabilities: January-December 2024

Phase two will entail a name change to the new Canada Dental Care Plan (CDCP). Phase two is actual insurance, not a cash benefit, and will be administered by the private insurer Sun Life. The formulary for insurance will likely be similar to that of the existing Non-Insured Health Benefit program (NIHB), another federal program that already provides dental insurance.

Technically, there is overlap between the end of phase one in June 2024 and phase two. A family can apply to both Canada Dental Benefit and the new Canada Dental Care Plan. They will be able to get both the CDB for its second period worth $650, and insurance, starting in January 2024.

This second phase covers not just young children, but any children under 18, seniors and people with disabilities. It has just started in 2024.

Given the complexity of the criteria for phase two, detailed counts of who is included or not are not estimated.

Phase three: All Canadians: estimated January 2025-onwards

The long-term form of the Canada Dental Care Plan starting in 2025, phase three, will provide dental coverage for everyone who doesn’t have dental insurance but whose family income is below $90,000.

As noted above, there are 12.9 million people in Canada without dental insurance who could certainly use it, but the income cap will restrict many from accessing it.

In phase three, the only eligibility restriction is the $90,000 family income cap and the lack of other dental insurance. Phase three of the CDCP will cover 8.4 million people but will leave another 4.4 million out of the system due to the income restriction.

To include those people, it would cost an estimated $1.45 billion on top of the $3.3 billion presently budgeted for the 2025-26 year.

In addition to covering Canadians without any insurance, the CDCP will also supplement existing provincial government fill-in-the-gaps dental insurance. These programs are often inadequate and the federal government CDCP generally provides better coverage. At this point, federal and provincial governments are negotiating as to who will cover what, but in the end, those accessing these provincial programs will likely see improved dental insurance, although they had insurance already.

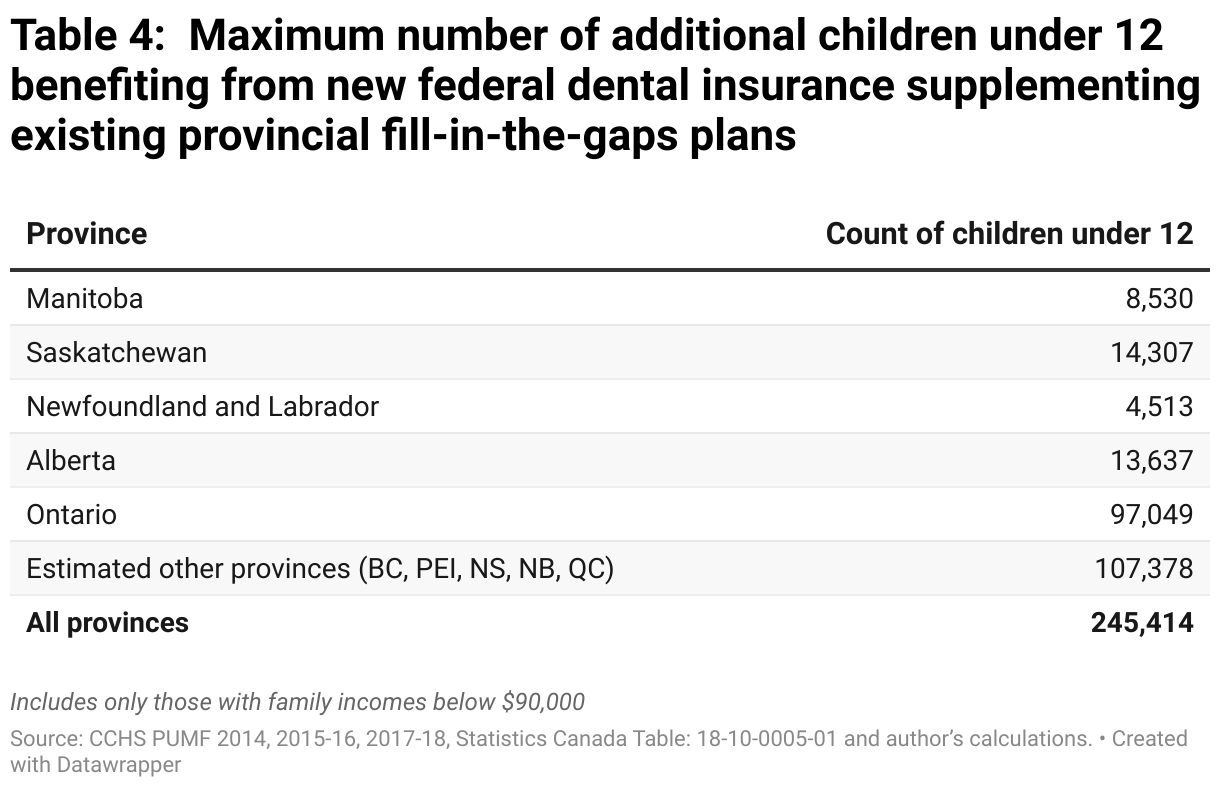

As shown in table 1, there are 245,000 children under the age of 12 and 1.1 million people over age 12 who rely on provincial dental insurance plans. The CDCP will likely improve coverage for these 1.4 million Canadians.

In total, there are 9.8 million Canadians who could benefit from the CDCP, if they apply. This includes people whose family income is under 90,000 and don’t have dental insurance but also those who receive provincial government dental insurance, although that insurance is likely inferior to the CDCP. Nonetheless, there are 4.4 million Canadians who don’t have dental insurance and will remain without it even after phase three of the CDCP because their family makes over $90,000.

Conclusion

It’s worth remembering that Canada’s dental insurance program is still very much under development. Its phase-in dates and design have already changed several times. Once fully implemented, the CDCP will help almost 10 million Canadians access dental care. The income restriction creates a troubling precedent for better medical coverage. Historically, public medical coverage has been for all, not just those who can’t afford it.

Although these aren’t examined here, deductibles, the procedures covered, total expense caps on dental insurance could create other impediments to accessing dental care, beyond the income restriction. Moreover, if caps like the $90,000 one implemented here don’t grow with inflation, fewer and fewer people will be able to access them over time. Initial estimates suggest this will result in 147,000 people being cut off of coverage in the first four years of the program alone. If the formulary for dental procedures isn’t indexed to inflation, it can lead to discrepancies in fees paid out between private and public plans, something that has already happened with provincial-level public dental plans.

The creation of an income cap percentage doesn’t have to be limited to federal dental insurance. There has been plenty of pressure building on the government to take concrete actions on pharmacare from the NDP. There have been notably fewer specifics on pharmacare compared to dental care, where a year-by-year plan was laid out in the Supply Confidence agreement. The findings in this document should inform the consideration of similar program design for pharmacare.

The choice is twofold: (1) Continue to create new medical care programs with a fill-in-the-gaps model and an income cap, like Canada is currently doing on dental care, or (2) Align new medical care programs with the principles of the Canada Health Act, which is based on the underlying principle of health care for all. A universal dental care and pharmacare program can create greater public buy-in, simplify eligibility rules, and ensure that everyone who needs access to those programs can do so without having to open their wallet for anything more than their health care card.

Methodology

Two broad approaches are used to derive the counts used above. For the counts of people aged 12 and over, the proportions from the 2022 analysis of the Canada Community Health Survey (CCHS) from Statistics Canada is used in conjunction with estimates from SPSD/M 30.0 for the counts of people in census families with a net adjusted family income of less than $90,000. However, this excludes young children aged less than 12. To estimate those proportions previous CCHS PUMFs are utilised, and those calculations are revealed in Table 3.

Costing in phase one simply uses the full cash value of $1,300 per eligible child.

Costing in phase three is provided using the average Non-Insured Health Benefit (NIHB) per capita dental costs. The formulary implemented in the CDCP will likely be similar to the NIHB. Initial costs on the CDCP may be higher than the NIHB average though given pent up demand for dental care services.

The CCHS examines dental care only in select provinces in a given two-year cycle. As a result, five provinces have relatively recent data on dental coverage and five are missing. Table 2 examines when data for which provinces became available and which are used in this analysis. The Public Use Microdata Files (PUMF) of CCHSs from each of these cycles form the basis of this analysis.

For the five provinces where dental insurance coverage data isn’t in the CCHS, we assume that the coverage rates above and below $90,000 in household income are the same, on average, as the provinces with data.

The CCHS only includes data on those 12 and older, which is an obvious problem since all three phases of the dental care plan examined will include children under 12. However, the survey does report if the household of the respondent contains at least one child under six and one child between five and 12. This is used to derive a count of children under 12, but the maximum count can only be two children. Alternatively, the CCHS provides the total count of people in the household (including children under 12) and it includes the household type. The household type can be used to derive a count of adults, i.e. a household with two parents has two adults. From this a count of children can be derived which is adjusted for the fact that there is as 12 out of 18 chance that that child is under the age of 12, as children here could be up to the age of 18. Between these two approaches, a best estimate of the count of children under 12 is created and an updated household weight is derived.

The CCHS income statistics are on a household basis, but the federal benefits will operate on a census family basis for the income test. The CCHS household version of income will put more people in higher-income quintiles, thereby underestimating those below the $90,000 income threshold.

The CCHS places the individual in five categories of total household income at $20,000 increments, starting from $20,000 through $80,000. The CCHS does not report the exact household income value. The category thresholds are inflation adjusted to 2023 dollars. The fourth income category, after inflation adjustment, is where the $90,000 test falls. We assume a uniform distribution in that fifth category and allocate counts based on the distance of 90,000 from the inflation-adjusted thresholds.

Appendix

In the report figures above, people benefiting from the various phases of the federal insurance are only those who have no other form of dental insurance. However, this isn’t entirely correct. Provinces and territories provide their own fill-in-the-gaps dental insurance programs, generally for children and/or low-income seniors. Often, the coverage from the provincial or territorial programs isn’t as good as it will be under phase two and phase three of the federal program. Negotiations are underway for the federal plan to supplement existing provincial plans, with one level of government being the first payer and the other being the second payer.

As such, the beneficiaries count of the federal plan in phases two and phase three will be higher than suggested above in that some families have some public insurance, but that coverage will be improved due to the federal plan.

Those over 12 who are covered by provincial government insurance are estimated using the 2022 Statistics Canada proportional calculations of people who “Have public dental insurance only” combined with the SPSD/M 30.0 population estimates of family income under $90,000, as above. However, the counts of children under 12 required reliance on previous CCHS PUMFs, as above.

The CCHS PUMFs report on whether dental insurance is government-sponsored versus private or employer-sponsored plans. In the 2014 CCHS, there is only a broad category of ‘government-sponsored’ insurance, which likely applies to more than just the provincial plans that the federal plan might supplement. For instance, those receiving the NIHB would be receiving government-sponsored insurance, but this wouldn’t benefit from the new federal dental plan because that plan and the NIHB will have similar formularies. Data for Manitoba and Saskatchewan are drawn from the 2014 PUMF.

In the 2015-16 and 2017-18 CCHS PUMFs, a more disaggregated listing of government plans, including “children/seniors” and “social service clients”, is available. These two categories likely better approximate the provincial plans that might be supplemented by the new federal coverage. Data for Ontario, Newfoundland and Labrador and Alberta come from these years. Depending on how the provincial and federal plans interact, the counts for these provinces likely represent a maximum of additional beneficiaries.

With those provisions in mind, Table 4 provides the counts of children under 12 whose household makes under $90,000 and who receive provincial government-sponsored insurance. These young children might receive an additional benefit from phases two and three of the federal plan as it supplements provincial plans. As such, the counts in Table 4 represent a maximum number of additional beneficiaries.

Acknowledgements

The author would like to thank the following people for their comments on an earlier version of this analysis: Brandon Doucet, Tracy Glynn, and Steven Staples.