In the absence of costed election platforms, political promises need to be scrutinized carefully for an “impossible trinity.” That is, the federal government can only do two of the following three things: cut taxes, increase spending, and reduce the budget deficit. Something has to give due to basic accounting.

Proposals for multi-billion-dollar tax cuts have figured prominently in the first weeks of the campaign, as analyzed by my colleague David Macdonald. Parties are also promising new spending, including for the military, east-west infrastructure connections and affordable housing. No leader has yet to state exactly how they would pay for these initiatives, although the NDP have stated they would re-institute the higher capital gains inclusion rate for gains above $250,000 that was cancelled before the election.

Prior to the election, many lamented the size of the federal deficit, which swelled to $61.9 billion in 2023-24. The larger deficit was attributed to two major accounting changes, which added more than $21 billion in red ink due to contingent liabilities for harms caused to Indigenous Peoples and costs from the COVID-19 pandemic. The federal deficit is projected to be $48.3 billion for 2024-25, with a baseline deficit of $42.2 billion (or 1.3 per cent of GDP) in the 2025-26 year that just began.

All of these figures are from last December, before accounting for the impacts of the second Trump administration. Larger federal deficits will ultimately be needed to provide a fiscal backstop to the negative economic hit from the Trump tariffs and overall deterioration of investor and consumer confidence. First, let’s take a step back to look at Canada’s fiscal capacity and the evolution of federal revenues, expenditures, and deficits/debt.

The bottom line is that the federal government remains in a good position to handle an economic shock wave—but we should be concerned about tax cuts eroding Canada’s fiscal capacity, especially in light of the need to forge stronger east-west connections. If Canada further engages in retaliatory tariffs in response to U.S. tariffs, this could also raise substantial revenue towards assisting workers and affected sectors, though magnitudes are hard to estimate at this time.

Federal revenues and expenditures

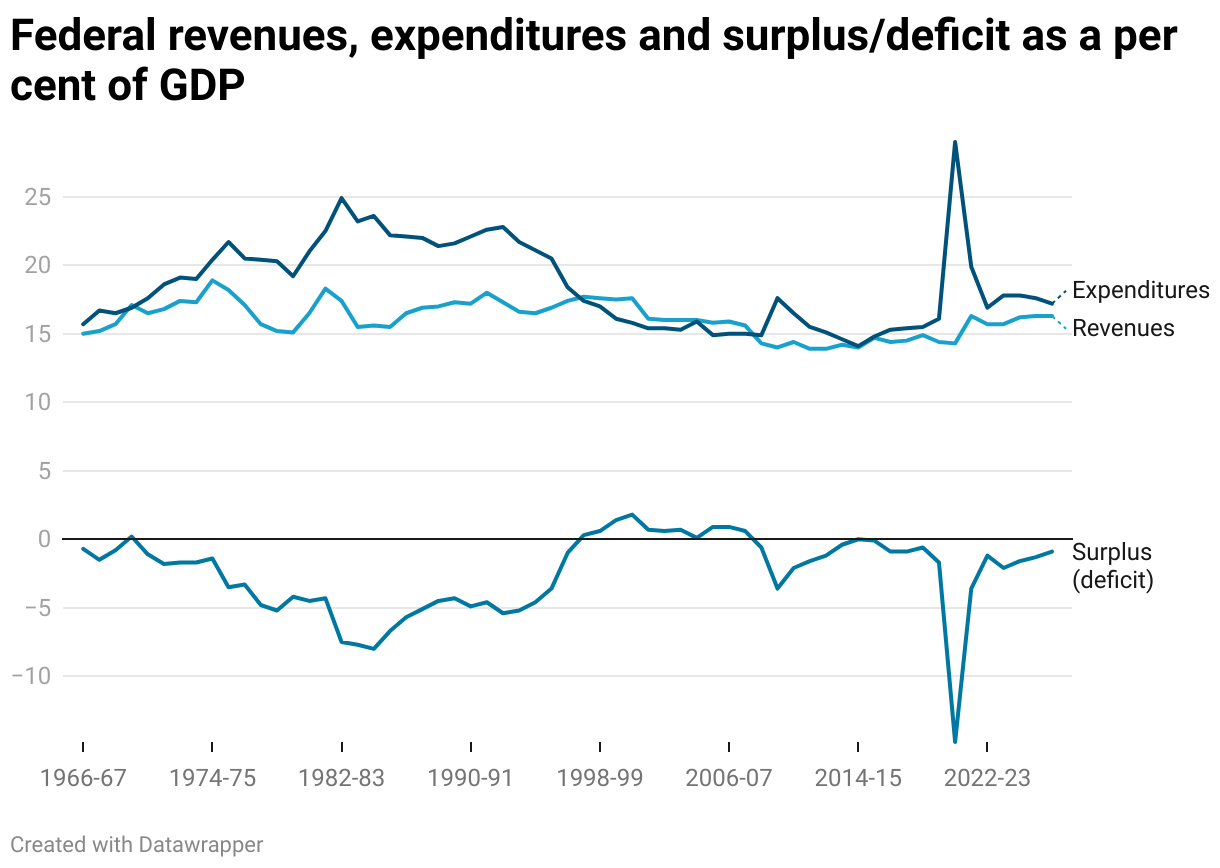

Figure 1 shows federal revenues and expenditures along the top, as well as the resulting surplus or deficit, as a percentage of GDP. The first thing to notice is how federal tax cuts have eroded fiscal capacity over the past quarter century. As late as 2000-01, federal revenues were 17.6 per cent of GDP before falling to a low of 13.9 per cent in 2012-13, reflecting personal and corporate income tax cuts made by both Liberal and Conservative governments, as well as the reduction in the GST from seven per cent to five per cent made by the Conservatives.

Federal revenues have since recovered somewhat to 16.2 per cent of GDP in the 2024-25 fiscal year. Nonetheless, if the federal government had as much revenue relative to GDP as it did in the late 1990s, that would represent an additional $38 billion. That would be enough money to fully implement a pan-Canadian child care program, comprehensive public pharmaceutical drug coverage and eradicate homelessness—with plenty left over for other priorities.

The loss of federal fiscal capacity also shows up on the expenditure side. In 2024-25, federal expenditures amounted to 17.8 per cent of GDP and are projected to decline further to 17.2 per cent in 2026-27. In contrast, federal expenditures were notably much higher during the entire period between 1971-72 to 1996-97.

That said, two recent events stand out for federal expenditures, which jumped to 17.6 per cent of GDP in 2009-10 due to federal response to the Great Financial Crisis, and a much larger bump to 29 per cent of GDP occurred in 2020-21, reflecting the COVID-19 pandemic. These events demonstrate that federal expenditures can be much higher if we choose to make them so. In both cases, after their peak, expenditures resumed falling steadily as a percentage of GDP.

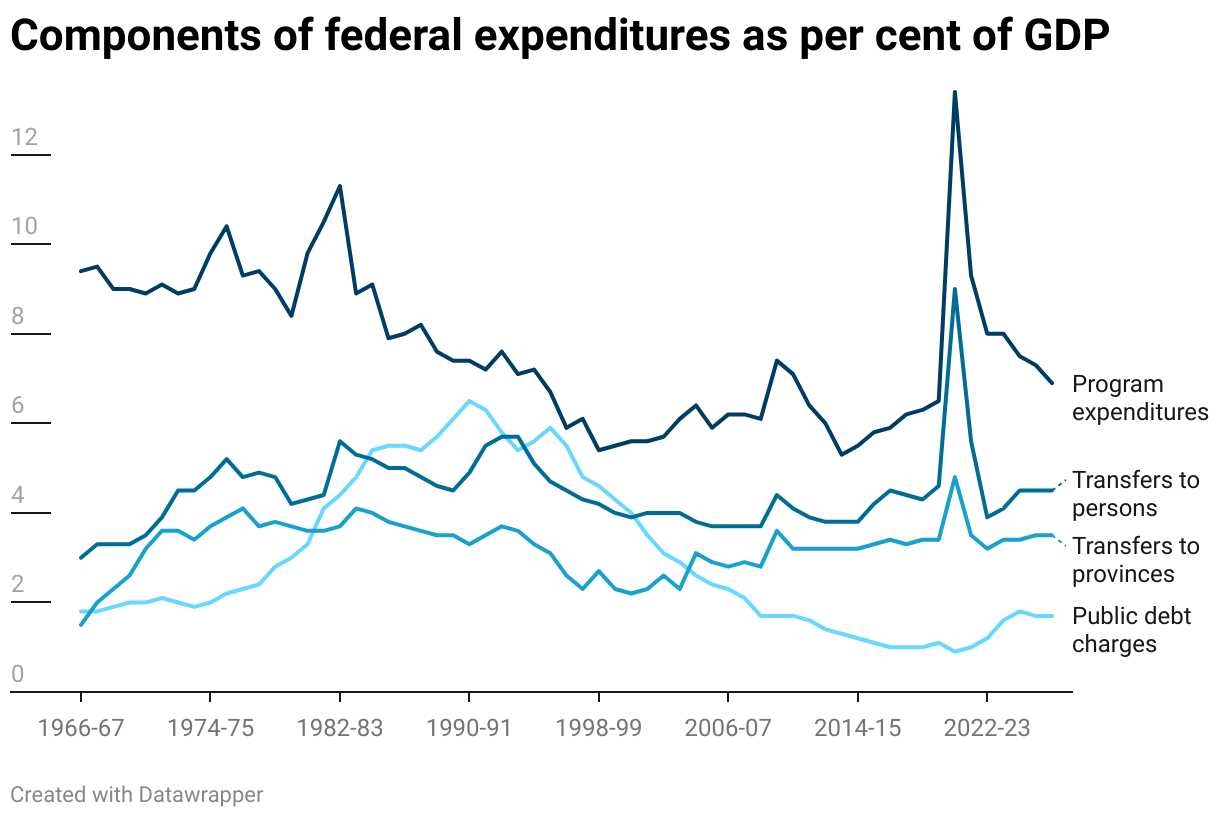

Figure 2 breaks down federal expenditure into its major categories. Federal direct program spending, at 7.5 per cent of GDP in 2024-25, is up from the 2000s but remains well below the levels of the 1960s to 1980s. There is a lot of scope for the federal government to take a more active role in channeling resources, where needed, to respond to current challenges.

Much of what the federal government does is provide transfers to the provinces for health care and social programs, and transfers to persons for child benefits, old age security and unemployment insurance. Transfers to persons are a full percentage point of GDP lower than they were before spending restraint began in the mid-1990s, whereas transfers to the provinces have held up somewhat better.

Federal debt service payments accounted for 1.8 per cent of GDP in 2024-25—the same as 1966-67 and 1967-68, and lower than any year after that up to 2007-08. This is largely due to today’s debt being financed at much lower interest rates than the 1990s.

Federal deficits and debt

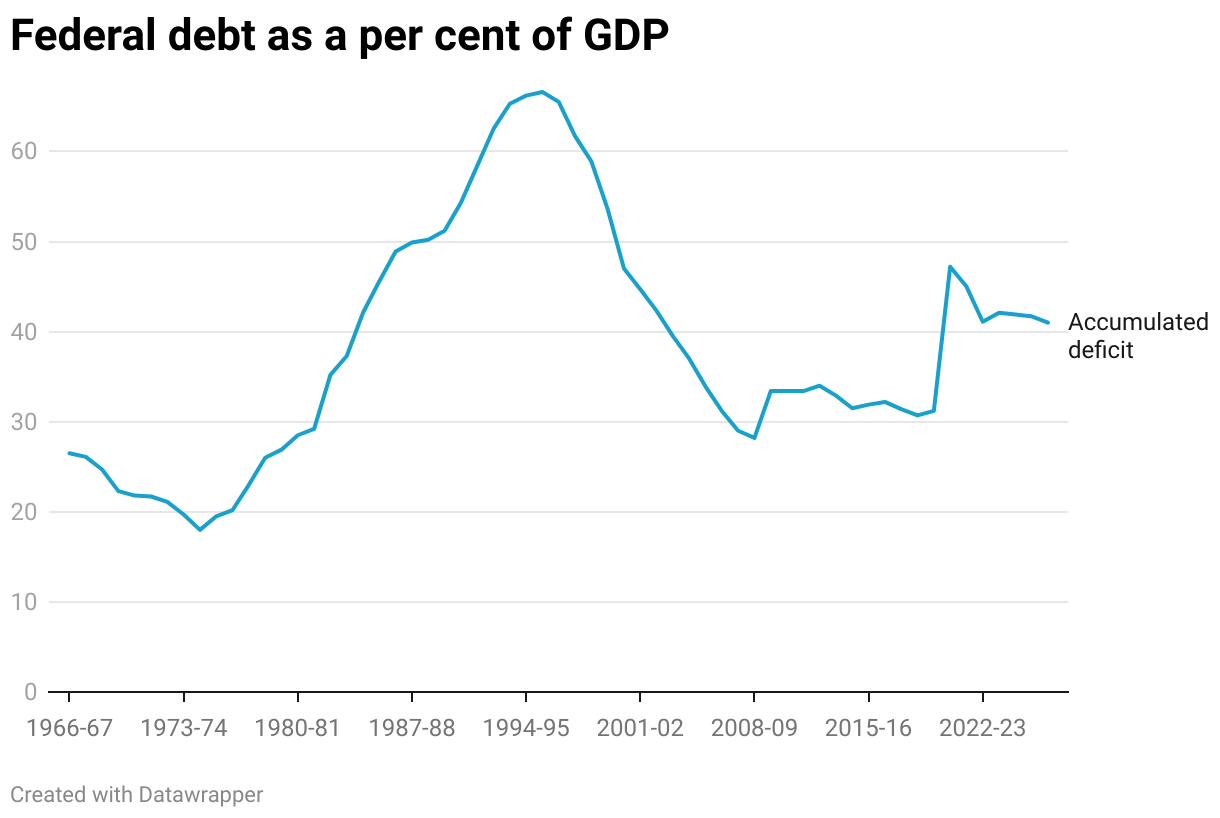

Both the 2008 financial crisis and COVID-19 warranted a major federal response, in terms of larger deficits to support aggregate demand in the overall economy. From a COVID-related high of 47.2 per cent, the federal level of debt-to-GDP (also called the accumulated deficit) is estimated to fall to 41.0 per cent in 2026-27. Put another way, in recent years federal debt has grown at a slower pace than the overall economy. Even though there have been federal deficits, they have been relatively small in magnitude.

Federal debt-to-GDP, at 41.9 per cent in 2024-25, is middling relative to the past six decades. Current levels are well below those of the 1980s and 1990s, when the federal debt was a front-page issue. Indeed, the federal debt-to-GDP ratio peaked at 66.6 per cent in 1995-96. The subsequent drop to 28.2 per cent of GDP in 2008-09 shows how quickly public debt can fall if the economy is doing well.

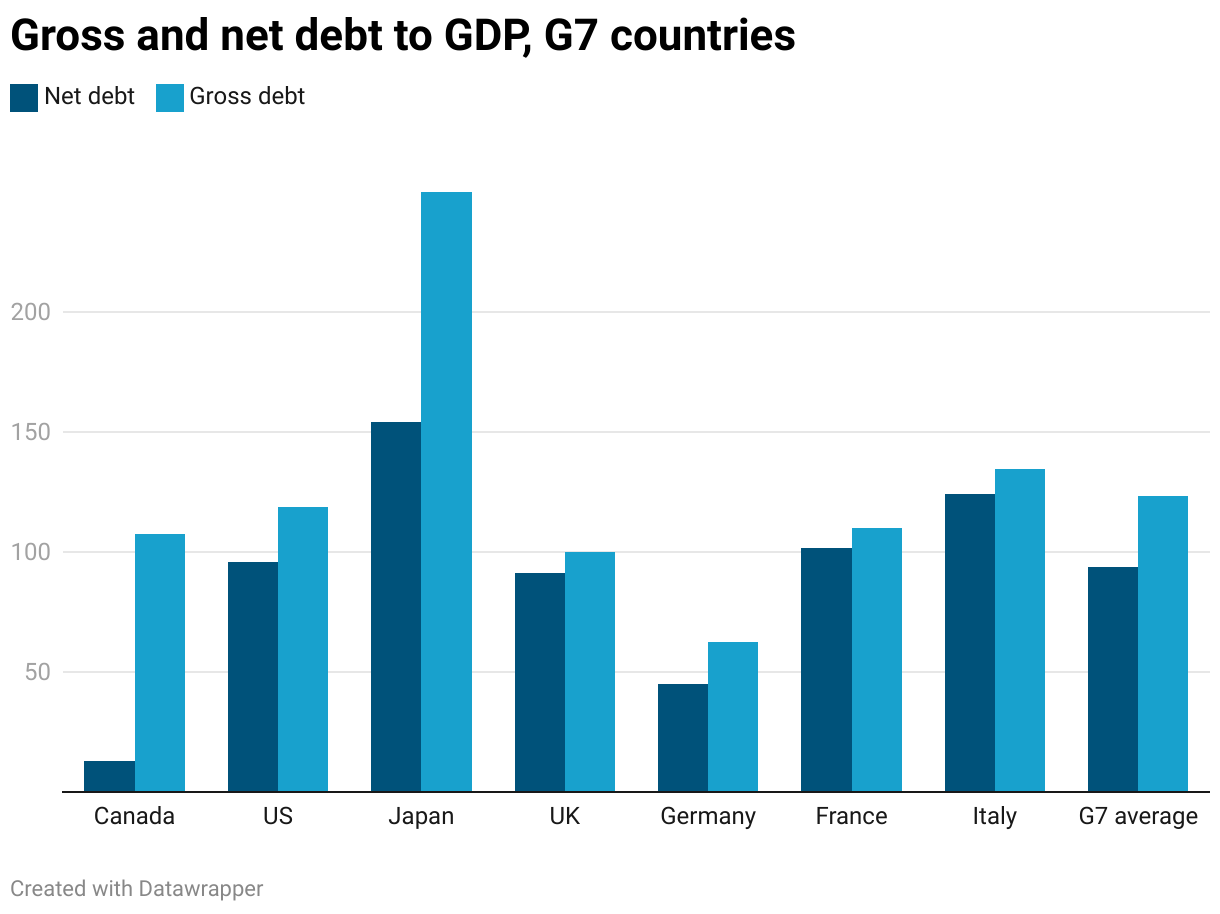

Another way of looking at total debt is in comparison to other countries. Figure 2 shows two measures of total Canadian debt (including provincial/territorial governments). Canada’s gross debt in 2023 was 107.5 per cent—an amount that is lower than the United States and the weighted average of G7 countries. Japan has an astonishingly large gross debt-to-GDP ratio after a prolonged period of slower growth and still manages to be a strong economy.

Figure 2 shows that Canada is nowhere close to any kind of “debt wall.” Gross debt only tells us part of the story—we also have to deduct the vast financial assets held by governments to get a measure of net debt. Here, Canada vastly outperforms other G7 countries, with net debt of only 13 per cent of GDP, compared to 95.7 per cent for the United States and 94 per cent for the G7 average. Non-financial assets like land, buildings and natural resources are also not included in net debt.

Tax cuts erode fiscal capacity

One of the major economics lessons of the 20th century and the Great Depression is that governments need to act in a counter-cyclical manner. In a crisis, governments shouldn’t be tightening their belts, they need to run deficits to support demand.

These Keynesian policies have been good for Canada, as the country has done well weathering the twin storms of the 2007-09 financial crisis and the 2020-21 COVID-19 pandemic. The federal government’s fiscal position remains solid as the Trump tariffs begin to take hold of the economy.

Income tax cuts along the lines of those promised by the Liberals and Conservatives, as well as raising the basic personal amount (the threshold for paying income tax), will provide some stimulus, if deficit-financed. But too much of the tax cuts goes to higher-earning households that are less likely to spend (and more likely to save) the proceeds.

In contrast, low-income households typically don’t earn enough income to benefit from income tax cuts. Low-income households tend to directly spend any financial support or income transfers (for example, a refundable tax credit) in the local economy.

Canadians would be better off without the tax cuts and, instead, with stronger public spending, which will have a more stimulative impact on the economy. The federal government can and should do more of the heavy lifting when fighting recessions, as it did during the COVID-19 pandemic. This is also true for funding national programs that help weave the country closer together and reduce inequality.

Tax cuts thus further undermine federal fiscal capacity at a time when we need a strong federal presence to act in opposition to the Trump tariffs. The good news is that the federal government has substantial room to support workers and the transition away from reliance on the U.S.