Our content is fiercely open source and we never paywall our website. The support of our community makes this possible.

Make a donation of $60 or more and receive The Monitor magazine for one full year and a donation receipt for the full amount of your gift.

Read the full Alternative Federal Budget 2024 here.

Introduction

In the summer of 2023, inflation came back within the federal government’s guidelines of between one per cent and three per cent. Unfortunately, only a week before this data was released, the Bank of Canada again raised its overnight rate. This drop to sub three per cent inflation had been predicted months earlier, based mostly on base effects and wasn’t a surprise to the Bank of Canada.1 This signals that the bank may not be operating on the one to three per cent range but, rather, it may want to see the inflation rate at or below two per cent before rates decrease. More increases may well be in order if the headline rate remains at roughly three per cent, which is the forecast for the fall of 2023.

Rate hikes now will have no impact on inflation in the near term since the lag times for impact are tremendous. The full impact of rate hikes aren’t for 11 quarters—almost three years—with 75 per cent of the impact hitting within nine quarters or more than two years, according to the bank’s own research.2 Changes in the summer of 2023 won’t have an impact until 2025. There are clearly prices that need controlling, like high housing prices, but higher interest rates are a poor mechanism, particularly when lags are so long. Having mortgage holders and renters pay so much more in interest that their slashed spending elsewhere causes a recession is certainly not the best route.

The cost of living is hardly the only concern for Canadians. While poverty rates plummeted during the pandemic economic shutdowns due to massive temporary federal income supports, they are now rising. Climate change is alternatively burning our forest and then flooding our rivers. Long-term care and health care remain of great concern, with ERs closing and staffing shortages endangering patients. Historic under- investment in First Nations’ communities on reserves have created some of the lowest income places in Canada. These issues aren’t something the market will resolve; they are unavoidably public problems that governments have been attempting to manage, but the scale is far too small.

Overview

The simplistic logic of the “government as a household” that needs to only spend as much as it raises from taxes every year is erroneous and often used to block critical investments. In reality, the federal government isn’t like a household, but it is like a member of one. The other members are provincial governments, individuals and the corporate sector. Each one trades with the others and every transaction has two sides: a deficit and a surplus. If you’re receiving money, you’re on the surplus side; if you’re paying it, you’re on the deficit side. In this way, every deficit in one sector exactly equals any surplus in another sector. Simply looking at one member of the household—say, the federal government’s deficit— completely ignores that another sector got that money as a surplus. We can’t tell if a deficit was good or bad unless we know who was on the other side of the transaction and how that money was spent. A federal deficit creating a surplus among households may seem positive unless it is all due to tax cuts for the rich.

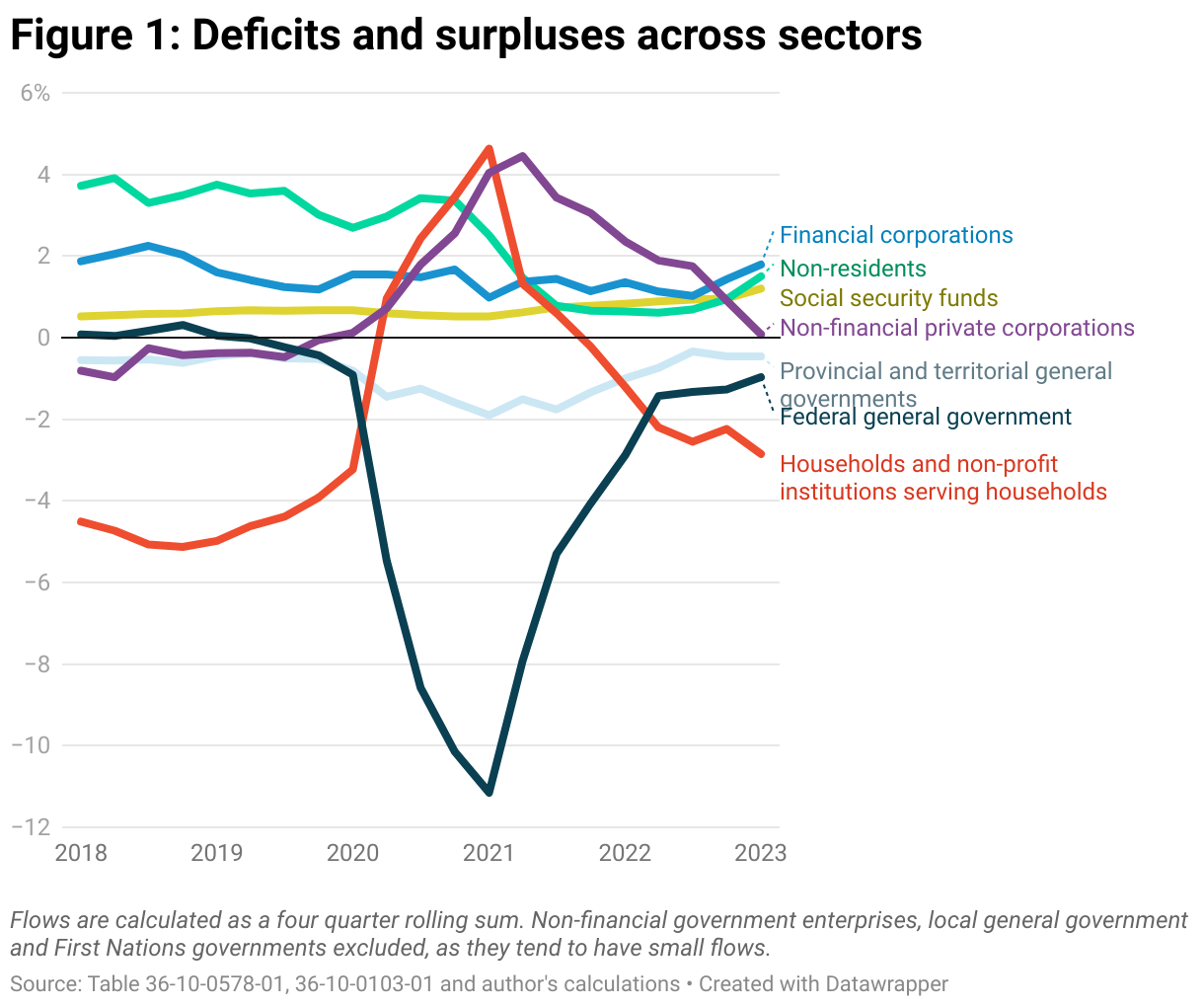

On a technical perspective, this is called the financial flow accounts. They are presented in Figure 27.1 and show which sectors were in deficit and which sectors received those deficits as surpluses. The sum of all deficits and surpluses in a given quarter is always zero, since all money ends up somewhere.

During the pandemic economic shutdown, the federal government ran a substantial deficit, but this money went somewhere and created a corresponding surplus initially among individuals—due to programs like the Canada Emergency Response Benefit (CERB) and the Canada Recovery Benefit (CRB). It also created a surplus in the corporate sector through the larger CEWS program, which had far fewer strings attached than worker programs. Here a federal deficit created surpluses that ended up in shareholder payouts and executive bonuses, which isn’t the best use of a deficit.

In 2021, as the CERB and CRB programs were rapidly wound down, the surplus for households dropped substantially and the federal deficit started to shrink.

The federal deficit was also caused by massive new pandemic transfers to the provinces. Provincial transfers for health care, long-term care, municipal transit, child care and schools meant that provincial deficits didn’t change much over the pandemic.

This was also the period when inflation took off. On the one hand, the historic surplus enjoyed by non-residents (i.e. people outside of Canada because we imported more than we exported) dropped during the pandemic because people couldn’t shop due to economic shutdowns and then continued to drop after the re-opening, due to supply chain issues.

On the other hand, corporate profits, i.e. surpluses in the corporate sector, went through the roof as they pushed households into a deficit situation but also captured those supply chain issues with higher prices.

Effective surtaxes on excess corporate profits for exactly this type of reason could have made federal deficits smaller while capping corporate surpluses, but there weren’t any in place at the time (see the Taxation chapter). In more recent quarters, corporate surpluses have petered out as inflation has come back down, hopefully ending this period of rapid price increases, which were effectively captured by corporate profits.

In the most recent quarters, federal deficits have been much smaller, but smaller federal deficits means smaller surpluses elsewhere. Households have been driven back into a deep deficit situation since 2021. The financial sector is now picking up more of the federal deficit as a surplus—it didn’t enjoy the same surplus as the non-financial corporate sector did during the pandemic. Also, non-residents are upping their capture of federal deficits.

Federal deficits, per se, aren’t good or bad—they are only one side of a transaction. To properly evaluate the utility of a deficit, we need to understand which sector is on the other side gaining a surplus and what that surplus went towards. It’s misrepresentative to say, out of the gate, that federal deficits are bad and federal surpluses are good because it fails to understand the rest of the economy and the role that the federal government plays in it.

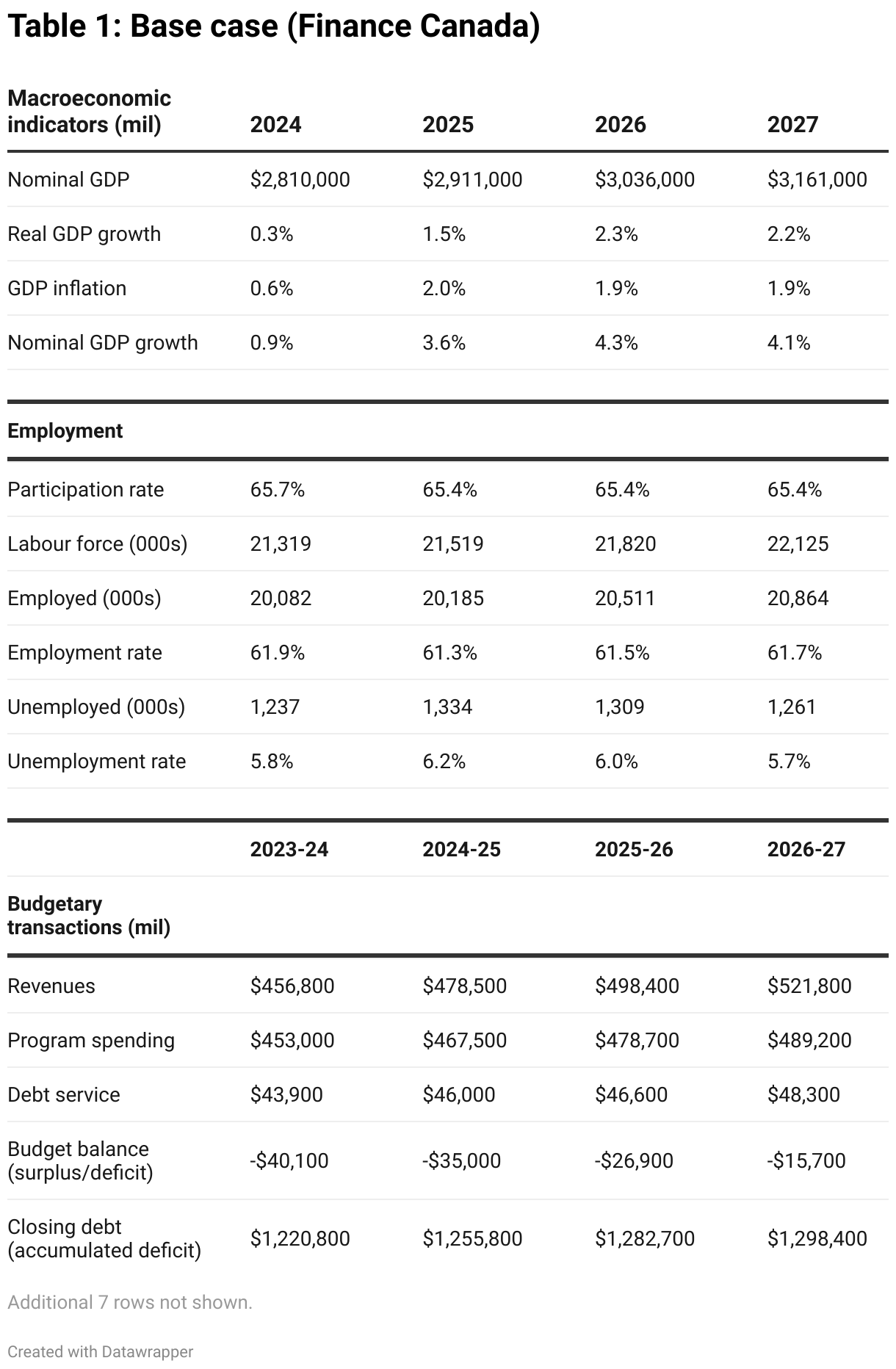

Economic projections: the base case

The Alternative Federal Budget (AFB) relies on the most recent Finance Canada projections on the state of the economy and federal finances, in this case, the 2023 federal budget. This represents the base case upon which the AFB is added, as shown below.

In the base case, at best there is no real GDP growth in 2024 and at worst there is a recession. It all depends on the timing of the no-growth scenario next year and how it is allocated across quarters. So far in 2023, we’ve seen almost no real GDP growth, excluding the January figures.

Finance Canada also projects that inflation will be entirely vanquished by 2024, coming in at only 0.6 per cent for the year. The inflation in Table 27.1 is GDP inflation, or changes in all prices, not just for goods and services sold to consumers, but nonetheless, it is quite low.

Growth into 2025 remains low, showing the protracted impact of high interest rates on economic growth for years to come. Throughout the projection horizon, the deficit is falling. Debt service charges are rising, due to higher interest rates, but the debt-service-to-GDP is falling nonetheless. In the aggregate, the debt-to-GDP ratio has fallen rapidly from its peak of 48 per cent in 2020. Generous pandemic supports allowed for a rapid economic recovery. It also rapidly drove down the relative debt back to where it stood in 2002.

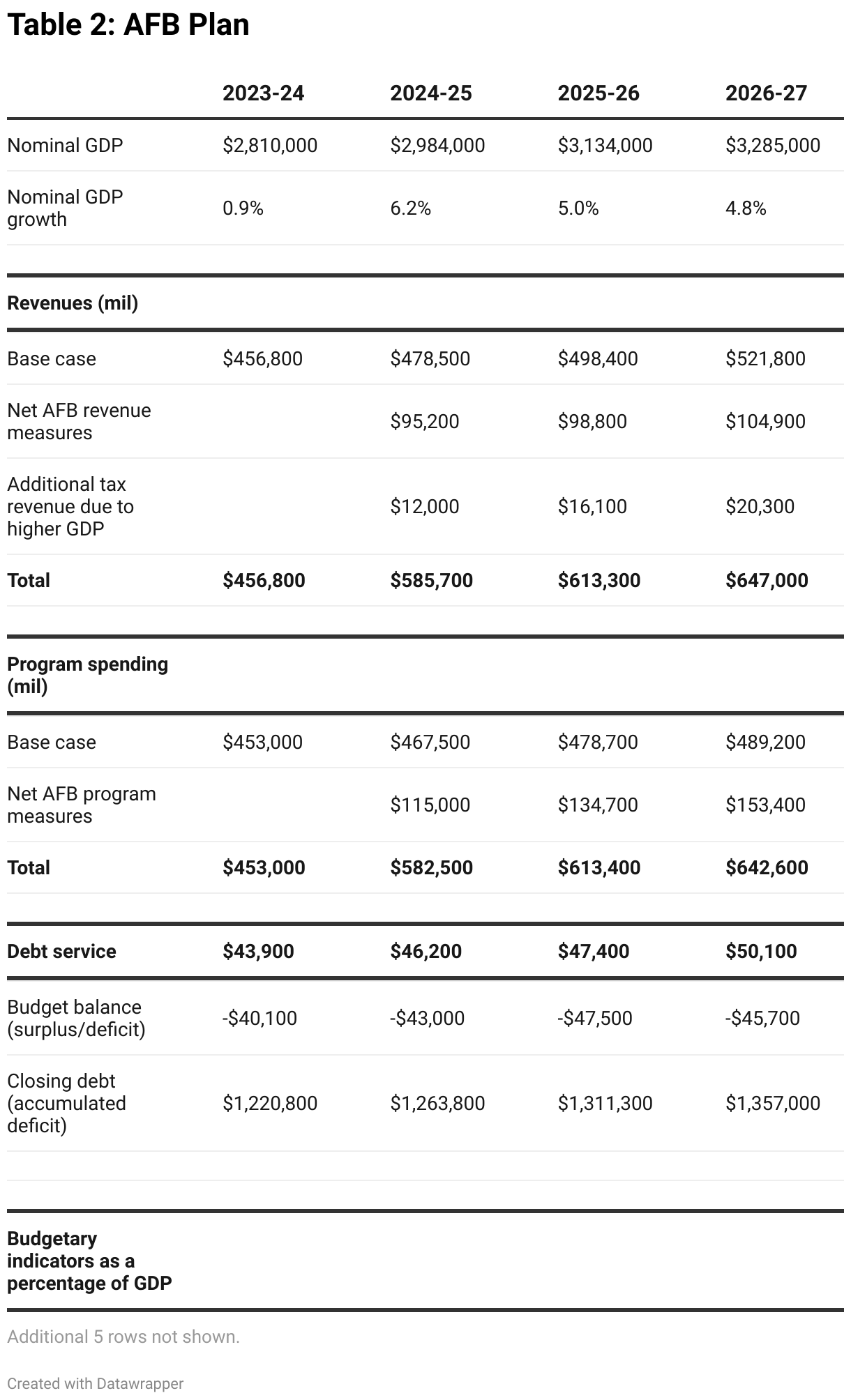

Economic projections: the AFB impact

The aggregate impact of all AFB chapters, which is cost out in Table 27.4, are summarized in Table 27.2. This shows all changes in both revenues and expenditures placed atop the base case estimates of Finance Canada above. The net impact of AFB measures on GDP, employment and income taxes paid are also estimated using Statistics Canada Input/Output total multipliers.3

Instead of middling nominal growth in 2024-25, the AFB substantially increases GDP growth in that year, accomplishing critical tasks, such as building out the national affordable child care plan, addressing climate change and making substantive progress on the infrastructure gap in First Nations communities. Higher nominal GDP growth continues in the second and third years of the AFB projection horizon.

The higher GDP is driven by a larger federal deficit, which creates larger private sector surpluses. Those surpluses in the pockets of Canadians and businesses drive more money through the economy, picking up growth in the process.

The AFB plans for a substantially larger role for the federal government in managing critical areas. It would increase federal program expenditures to GDP to almost 20 per cent, from their present level of 16 per cent.

However, the AFB would offset this new spending with new revenue in two forms: first, through higher taxes for wealthy Canadians and corporations and, second, through higher employment levels that would result in more income taxes paid. The result is that federal revenues to GDP under the AFB would also rise to just under 20 per cent, from their present level of 16 per cent.

The debt servicing costs are higher and incorporate Finance Canada’s projections on higher interest rates generally. However, the economy is also larger as the AFB invests in growth. The net result is that the debt- servicing-to-GDP ratio remains the same in the base case as the AFB case, with higher debt costs being easier to manage because we’ve got a more active economy.

The deficit remains stable, at roughly $45 billion a year—1.5 per cent of GDP. Meanwhile, the path for the debt-to-GDP ratio remains almost identical to the Finance Canada base case. While the debt is higher under the AFB, so is economic growth and the two offset each other. There are different paths to a lower debt-to-GDP ratio: one that tackles crises head on, driving economic growth in the process, and one that remains content with band-aid solutions to massive issues. The AFB chooses the former.

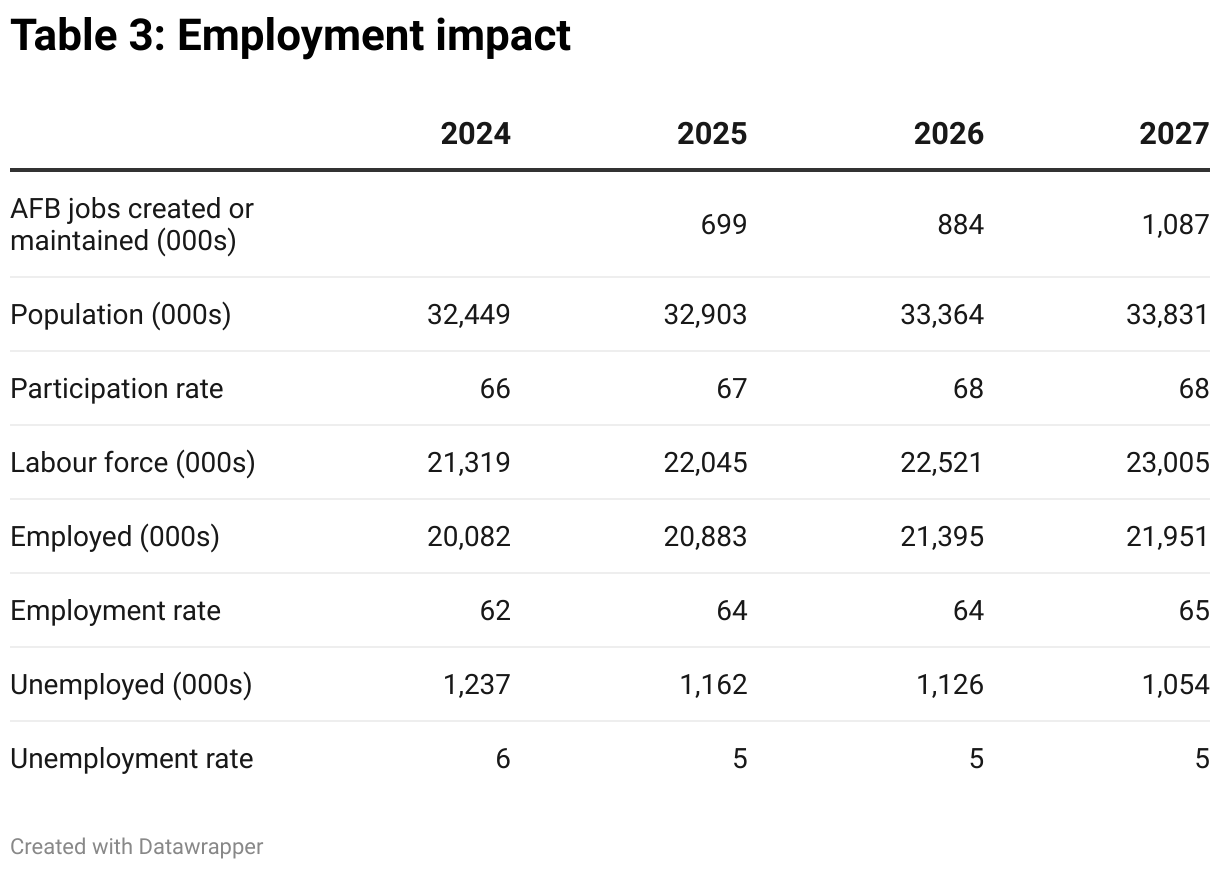

The AFB drives economic growth in addressing the defining issues of our time—like climate change, the health care crisis and housing costs— but that also creates jobs in the process. The Finance Canada base case sees unemployment climb to 6.2 per cent in 2024-25, from its 2023 level in the low five per cent range. Unemployment prior to the pandemic was in the high five per cent range, illustrating that a strong job market is possible without inflationary pressures.

The AFB doesn’t see employment as a problem—it’s a necessary part of the role of the federal government to provide job opportunities and keep the job market tight. As such, the AFB creates just over a million more jobs by the third year, pushing the unemployment rate to under five per cent.

Targeted poverty reduction in the AFB4

This section focuses on total poverty rates, with little analysis of sub- populations besides age. Broad averages obscure much higher poverty rates that can be found in various sub-groups. For instance, racialized and Indigenous Canadians face higher poverty rates than the general average and white Canadians face lower rates. Certain areas of the country, like First Nations communities, face unthinkable levels of poverty in a rich country like Canada and yet they are explicitly excluded from national poverty statistics in most data sources.

In many cases, understanding and tracking poverty across various subgroups requires better data disaggregation than what is currently available. Statistics Canada has recently made important strides with the expansion of the Canada Income Survey to the territories and the inclusion of a racialized flag in the Labour Force Survey. Unfortunately, this better disaggregated data hasn’t filtered down to Statistics Canada’s tax modelling software SPSD/M, limiting the amount of sub-population poverty impacts, particularly on racialized, Indigenous, and disability populations that can be estimated in the AFB. Hopefully, future iterations of the software can provide better differentiation of sub-populations to better understand the impact of the AFB on poverty rates.

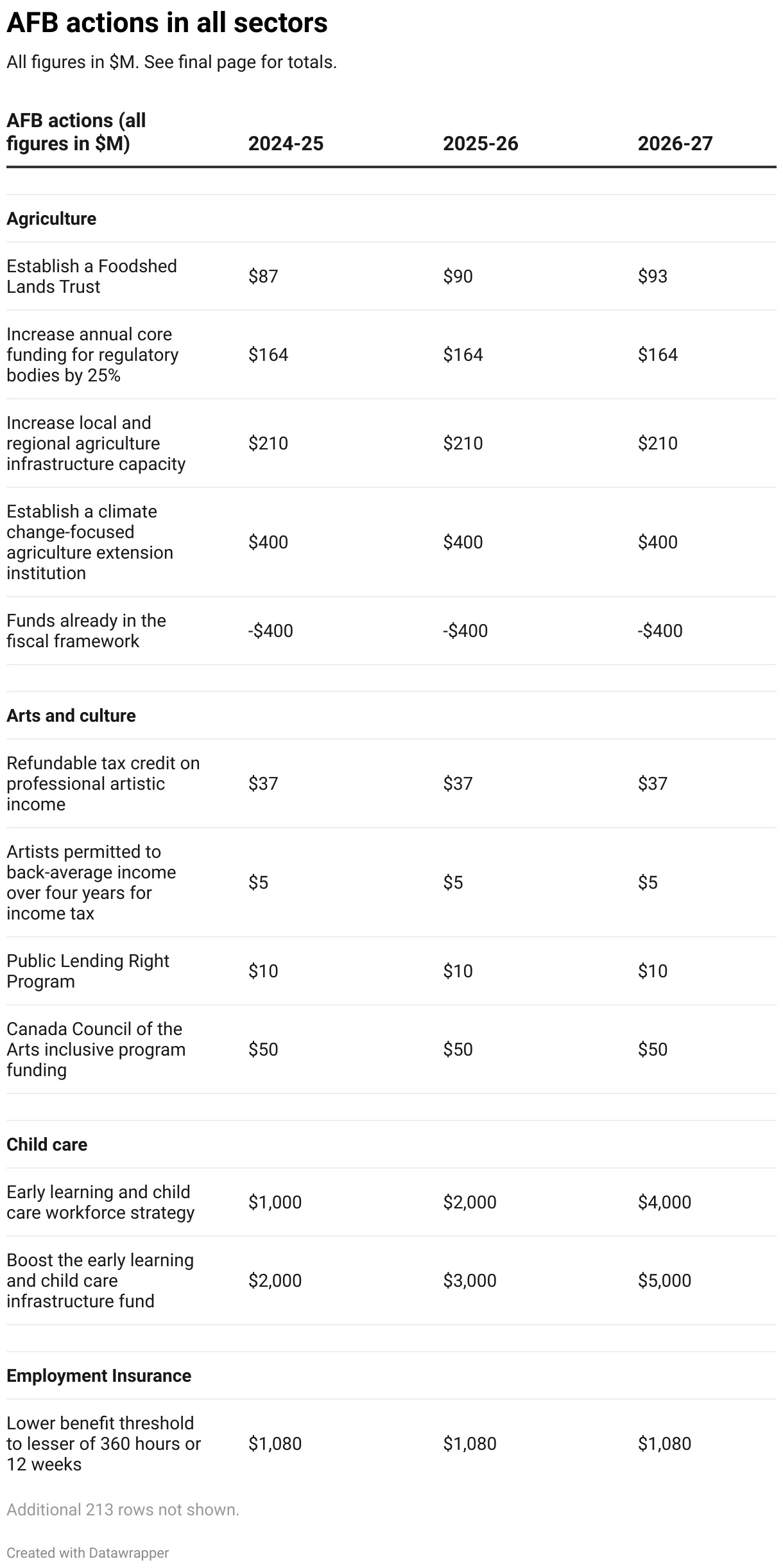

The key AFB poverty fighting tools line up with its four pillars of income support: for families with children, for older Canadians, for those with disabilities and for working age adults without children (see the “Poverty and income security” chapter). The poverty impact of each major AFB measure will be examined, as will the net poverty impacts of the entire AFB. The impacts of the main measures are shown in Table 27.4.

It’s important to point out that in order to obtain any of these supports, federal taxes must be filed. Not everyone files their taxes, leading to missed benefits in populations like recent immigrants, those who are insecurely housed, and Indigenous Peoples. The “Poverty and income security” chapter will do a trial of delivering federal income benefits through trusted third parties to better deliver these important supports to those who are entitled to them but aren’t receiving them.

Let’s start with the Canada Livable Income (CLI), which is the AFB measure to support working-age adults without children, who, essentially, have access to no other federal supports, particularly in the absence of employment income. The CLI is targeted to reduce deep poverty, which is defined as having income 75 per cent or more below the after-tax CF-LIM line. Unfortunately in Canada, there are 637,000 Canadians who are living in deep poverty, almost all of them of working age.

The CLI has almost no impact on poverty rates. Given its focus on deep poverty, it only lifts 24,000 people above the MBM line or 3,000 people above the CF-LIM. But it lifts 391,000 people out of deep poverty, reducing deep poverty in Canada by 69 per cent.

The Canada Child Benefit End Poverty Supplement (CCB-EndPov) is a top up to families that are already receiving the Canada Child Benefit (CCB). It provides up to $8,500 more a child to lower-income families.

Overall, the new supplement reduces the number of Canadians in poverty by 632,000 (MBM) or 566,000 (CF-LIM). It helps more than children, since poverty is evaluated at the family level, with everyone counting as low income if a family is below the income threshold. Since the CCB-EndPov is focused on children, it has a particular impact on child poverty—lifting 369,000 children out of poverty according to the MBM (348,000 CF-LIM). It also has a limited impact on deep poverty, reducing it by 33,000 people.

High poverty rates afflict older adults in their early 60s because they aren’t yet old enough to receive seniors’ benefits but their ability to work, particularly in physical labour jobs, can be limited. As such, the AFB would make the Guaranteed Income Supplement (GIS) available to those aged 60 to 64 in order to better support low-income older workers in that age range. Providing this further support lifts 84,000 older Canadians out of poverty according to the MBM (47,000 CF-LIM). This reduces the poverty rate for those 60 to 64 from 10.5 per cent to eight per cent MBM (15.9 per cent to 14.3 per cent CF-LIM). It also has the effect of reducing deep poverty by 33,000 people—65 per cent, since those 60 to 64 have few other supports outside of social assistance.

The Canada Disability Benefit has been much discussed, but the AFB would put meat on the bones of this plan, with a real strategy for implementation and actual support values. The AFB’s CDB would do a lot of the heavy lifting on poverty reduction since Canadians with disabilities live with much higher poverty rates. The CDB would lift 647,000 Canadians out of poverty.5

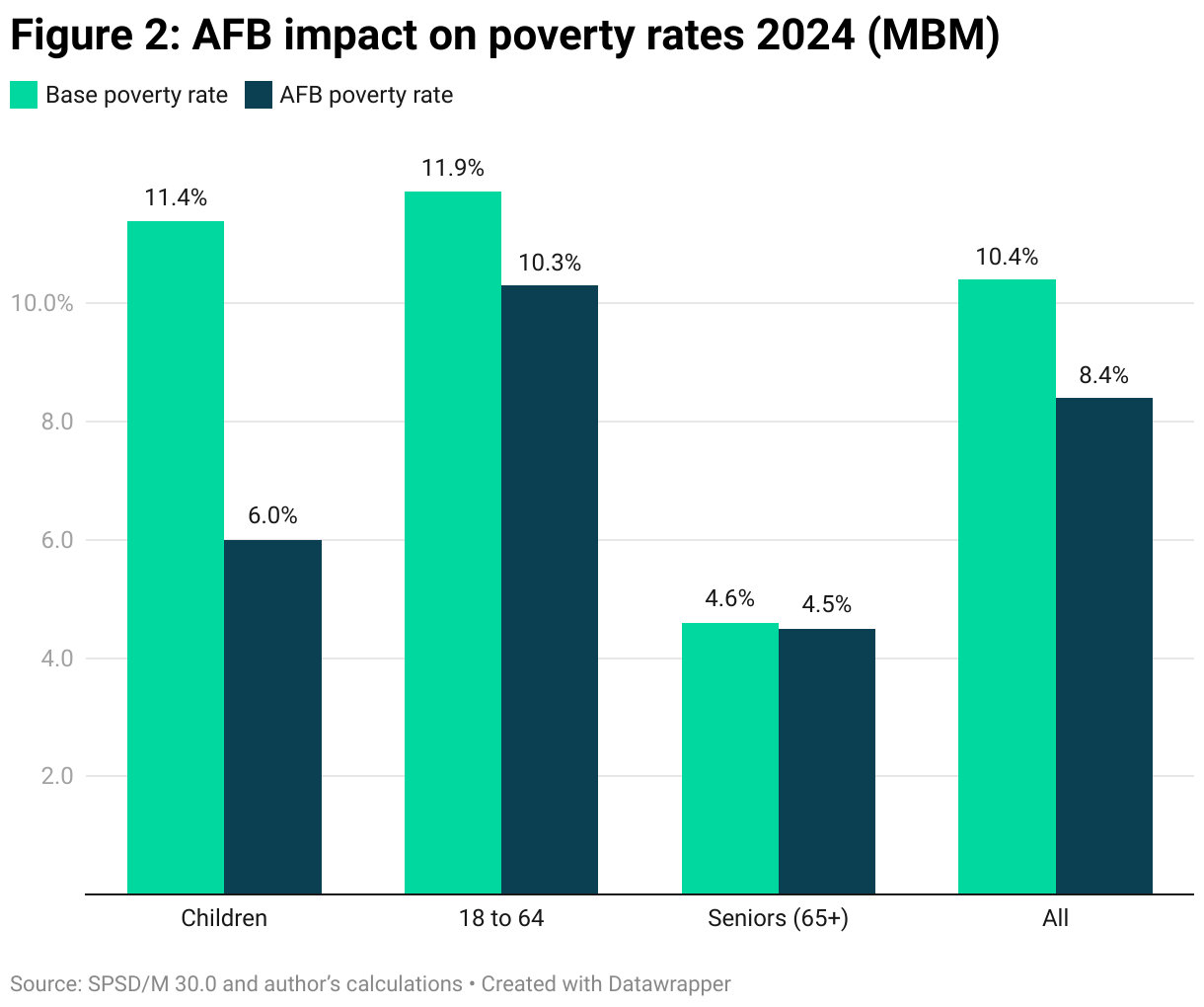

Overall, Figure 27.2 illustrates the net impact of the above changes and of all the tax/transfer changes in the AFB, including those that increase taxes in some areas. The AFB manages to lift 1.4 million people above the MBM line. This includes a million working-age adults and 389,000 children. The count of those in deep poverty is reduced by 400,000 people or 63 per cent. Broadly, the MBM poverty rate declines in 2024 from 10.4 per cent to 6.7 per cent, illustrating the potential impact of key AFB programs on poverty rates and on Canadians living in deep poverty.

As noted above, it’s not currently possible to calculate the poverty impacts on racialized or Indigenous families. These families are more likely to experience poverty, so they are more likely to benefit from the poverty reduction measures in the AFB. Housing affordability measures or measures in sectors that predominantly employ racialized workers (like higher wages in health care or agriculture) will also aid such families in getting closer to the Canadian income average.

Gender analysis

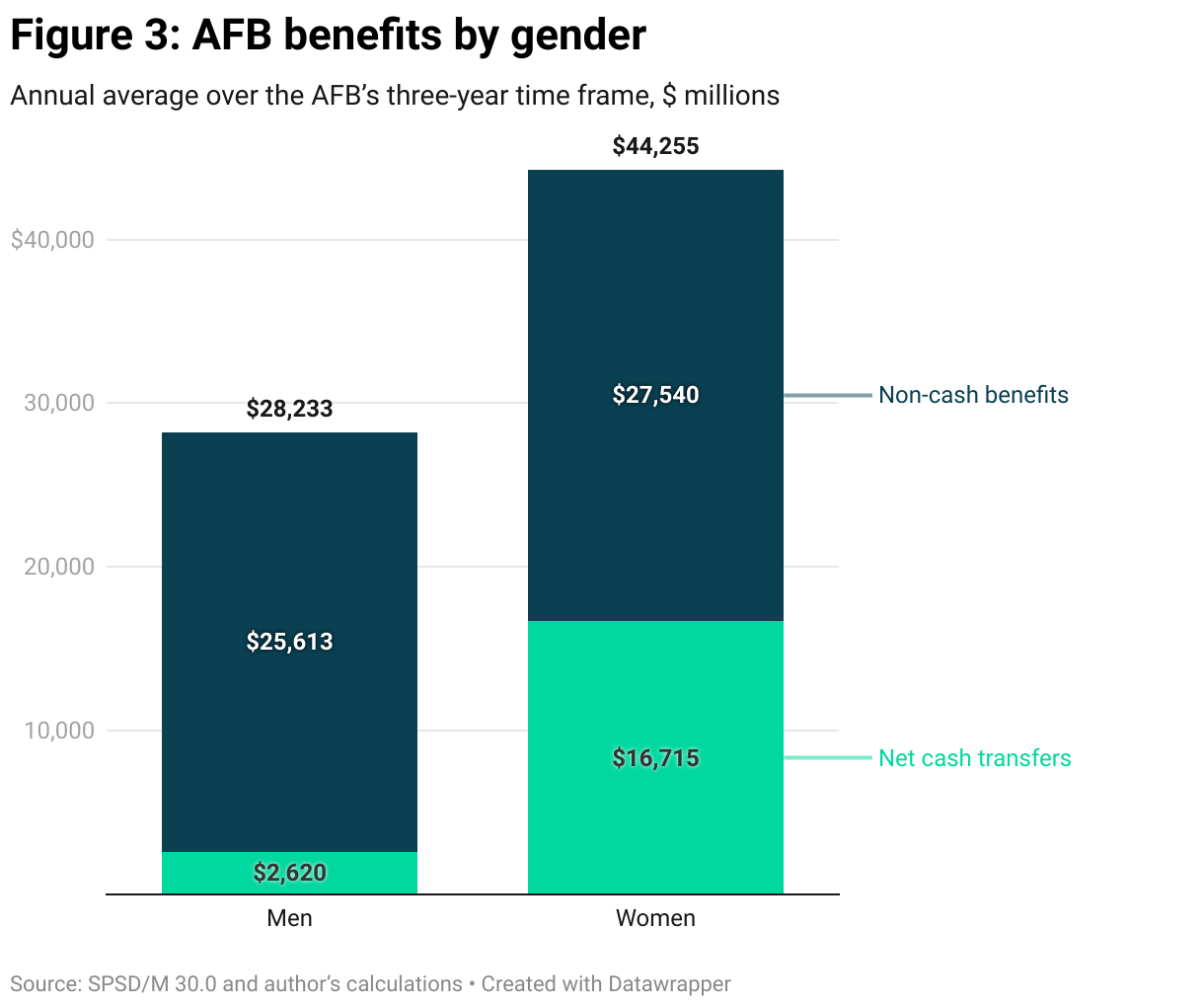

As part of the AFB’s regular reporting, we continue to track aggregate impact of AFB policies by gender. The approach used is to determine how much of a particular program goes to helping men vs. women.

Many AFB measures don’t benefit an identifiable individual. For instance, expanding zero-emissions electricity production or supporting active transportation infrastructure aren’t for the benefit of a particular gender and therefore aren’t included in the calculations behind Figure 27.3. But many programs do have identifiable populations. For example, investments in First Nations communities aid those living there, of which there are more women than men. Alternatively, aid for incarcerated people helps more men than women. Taxes and transfer changes can also be attributed to gender, with men paying more in new taxes, net of transfers, due to AFB changes for things like dividend taxation, because men are more likely to hold financial assets.

If we look at net cash transfers under the AFB plan (i.e. cash transfers net of tax changes) men see a small net benefit of $2.6 billion a year, on average, while women receive an additional $16.7 billion in net new transfers. The AFB’s changes in dividend and capital gains taxation fall more heavily on men. In contrast, the majority of the new CCB end poverty supplement is paid to women, due, in large part, to their capacity as mothers. Both men and women benefit from a decline in post- secondary tuition.

Now we turn to non-cash benefits, which is spending on programs that don’t result in individual cash changes but are programs with an intended target population. Many non-cash benefits will be of benefit to a particular population for which there is a gender breakdown. In this category, the distribution between genders is more even, with $25.6 billion in net new benefits flowing to men and $27.5 billion of net new benefits flowing to women, on average, a year from AFB non-cash measures. For example, higher wages in health care benefits women while support for agriculture would benefit more men, given the gender employment breakdowns in those industries. Therefore, for new non-cash benefits in the AFB, 52 per cent of flows to women and 48 per cent flows to men.

Combining both cash and non-cash benefits in all AFB programs where gender attribution is possible, we find that 39 per cent of net new benefits flow to men and 61 per cent of them flow to women. Broadly speaking, the AFB is what a gender-sensitive budget should look like.

Analyzing the aggregate impact of a budget in terms of poverty or on certain populations, like men vs. women, should be an important part of every government’s budget process. Recent federal budgets have come a long way in estimating their gender impact, although they provide less analysis of the impact on poverty or on other vulnerable subgroups. The AFB illustrates what’s possible in terms of these types of analysis as a template for governments to follow in their own budget processes.

This analysis also illustrates the substantial strides that a federal government could make on poverty reduction and the elimination of deep poverty. The AFB shows that the federal government can aggressively tackle the defining issues of our day and that the higher growth that that generates will keep our relative debt in check.

Notes

- See chart 19, Bank of Canada, April 2023, Monetary Policy Report.

- See table 1, Tony Chernis and Corinne Luu, 2018, DisaggregatingnHousehold Sensitivitynto Monetary Policy by Expenditure Category, 2018-32, Bank of Canada.

- Statistics Canada. Table 36-10-0594-01 Input-output multipliers, detail level

- Estimates in this section of poverty rates, poverty rate changes, deep poverty are the result of glass box calculations in 2024 based on Statistics Canada’s Social Policy Simulation Database and Model

- 30.0. The assumptions and calculations underlying the simulation were prepared by David Macdonald and the responsibility for the use and interpretation of these data is entirely that of the authors.

- Unfortunately, due to methodological complications, an estimate of the impact on CF-LIM poverty and deep poverty aren’t available.

Alternative Federal Budget Project/AFB Working Group. Every year, the Canadian Centre for Policy Alternatives works with a diverse array of experts and organizers from progressive organizations across Canada to produce an Alternative Federal Budget—a document which details what an ambitious federal budget could achieve. The AFB authors work together under the CCPA to produce this guiding document.