Summary

The following text is a submission by Canadian Centre for Policy Alternatives researchers to Employment and Social Development Canada covering the Canada Disability Benefit—a new benefit aimed at reducing poverty for Canadians with disabilities.1

As the text below outlines, the benefit falls significantly short of its poverty reduction goals. Its very design ensures that it will have a negligible impact on those most in need.

There are two key reasons for this negligible impact: unnecessarily restrictive eligibility criteria, and the wildly insufficient size of the benefit.

In order to qualify for the benefit, potential recipients must be between the ages of 18 and 64 years and have a Disability Tax Credit (DTC) certificate, a notoriously difficult to access program which requires extensive and costly paperwork. If this remains unchanged, the CDB would only reach 205,000 people.

Our content is fiercely open source and we never paywall our website. The support of our community makes this possible.

Make a donation of $60 or more and receive The Monitor magazine for one full year and a donation receipt for the full amount of your gift.

However, other federal and provincial programs have their own separate processes for determining disability that many people have already completed. If those other programs were included instead of relying on DTC certificates alone, it would substantially increase eligibility on day one. For example, if Canadians receiving income support through a disability stream of provincial social assistance or those receiving the CPP disability benefit could also qualify as “disabled” for the purposes of the CDB, the benefit would reach four times as many people (798,000).

As it stands, if someone qualifies for the CDB, they will receive a total annual benefit of $2,400—which will only lift 10,000 people out of poverty, out a total of 911,000 Canadians with disabilities aged 15 to 64 who live in poverty.

Expanding the eligibility as proposed would lift 46,000 people out of poverty on day one. Higher benefit levels would predictably be better at reducing poverty. For instance, to lift 200,000 people out of poverty would require a benefit level of $7,000 a year at an annual cost of $5.9 billion. Several other benefit levels with corresponding costs are simulated.

The authors recommend that the Government of Canada:

- Expand the pool of potential beneficiaries by expanding the eligibility requirements. Including Canada Pension Plan-Disability (CPP-D) and social assistance disability steam recipients as additional routes to accessing the CDB would be an obvious first step. The government should also investigate other disability programs such as workers compensation as potential vehicles for assessing disability status.

- Increase the benefit level until it begins to have an actual impact on poverty rates. $2,400 per year simply isn’t enough to meaningfully address the high levels of poverty that people with disabilities experience and the high cost of living associated with having a disability.

- Redefine the Canada Disability Benefit within the tax system as it will presently reduce eligibility for other federal and provincial supports including social housing (e.g., exempting the CDB from the calculation of Adjusted Family Net Income).

Canada Disability Benefit: a long time coming

The Canada Disability Benefit has been a long time coming. First announced in 2020, framework legislation establishing the benefit received royal assent in June 2023—and the benefit design was released in Budget 2024 and the June 29 Canada Gazette. Public consultations on the proposed regulations are underway. The new program is set to start in July 2025.

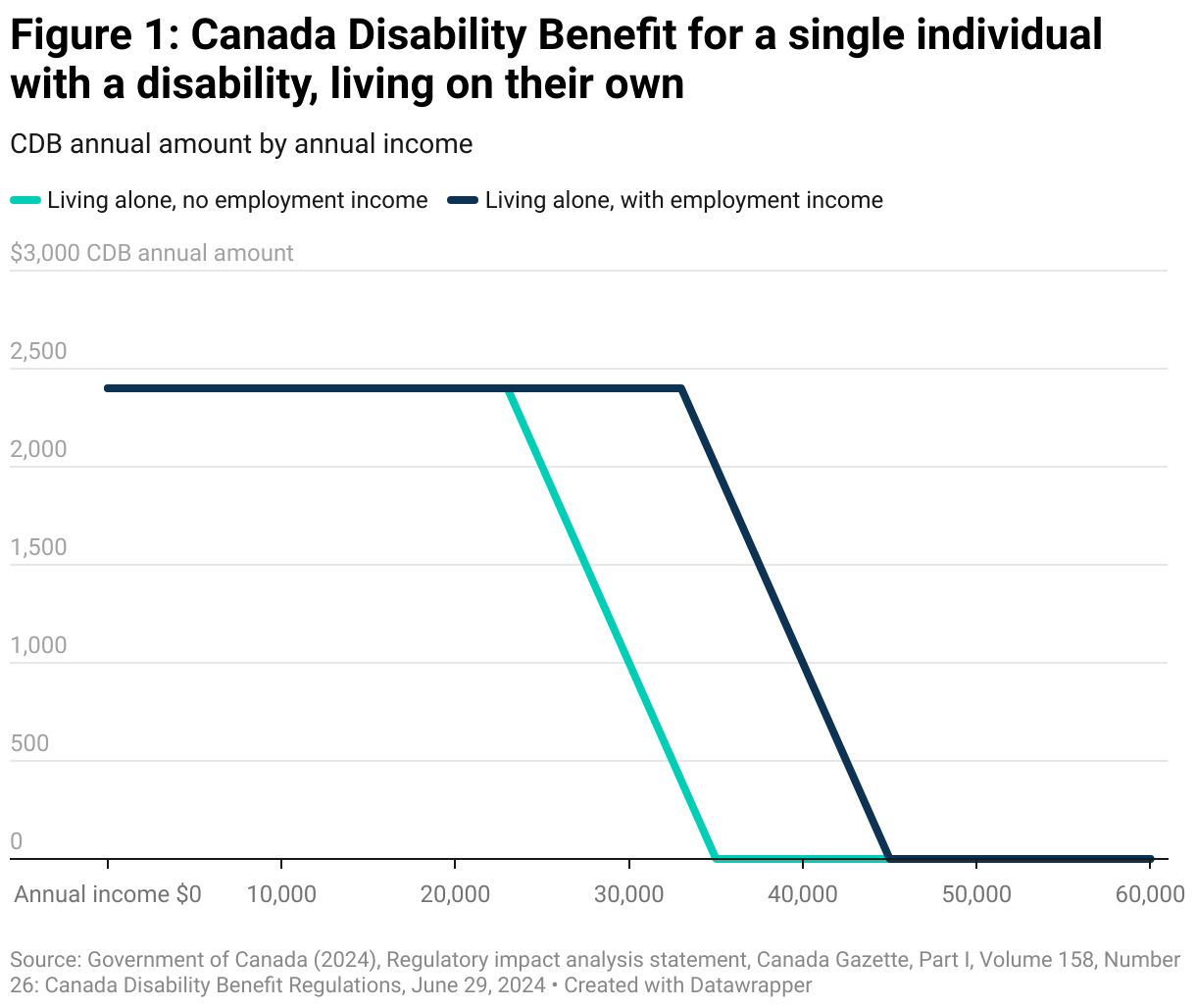

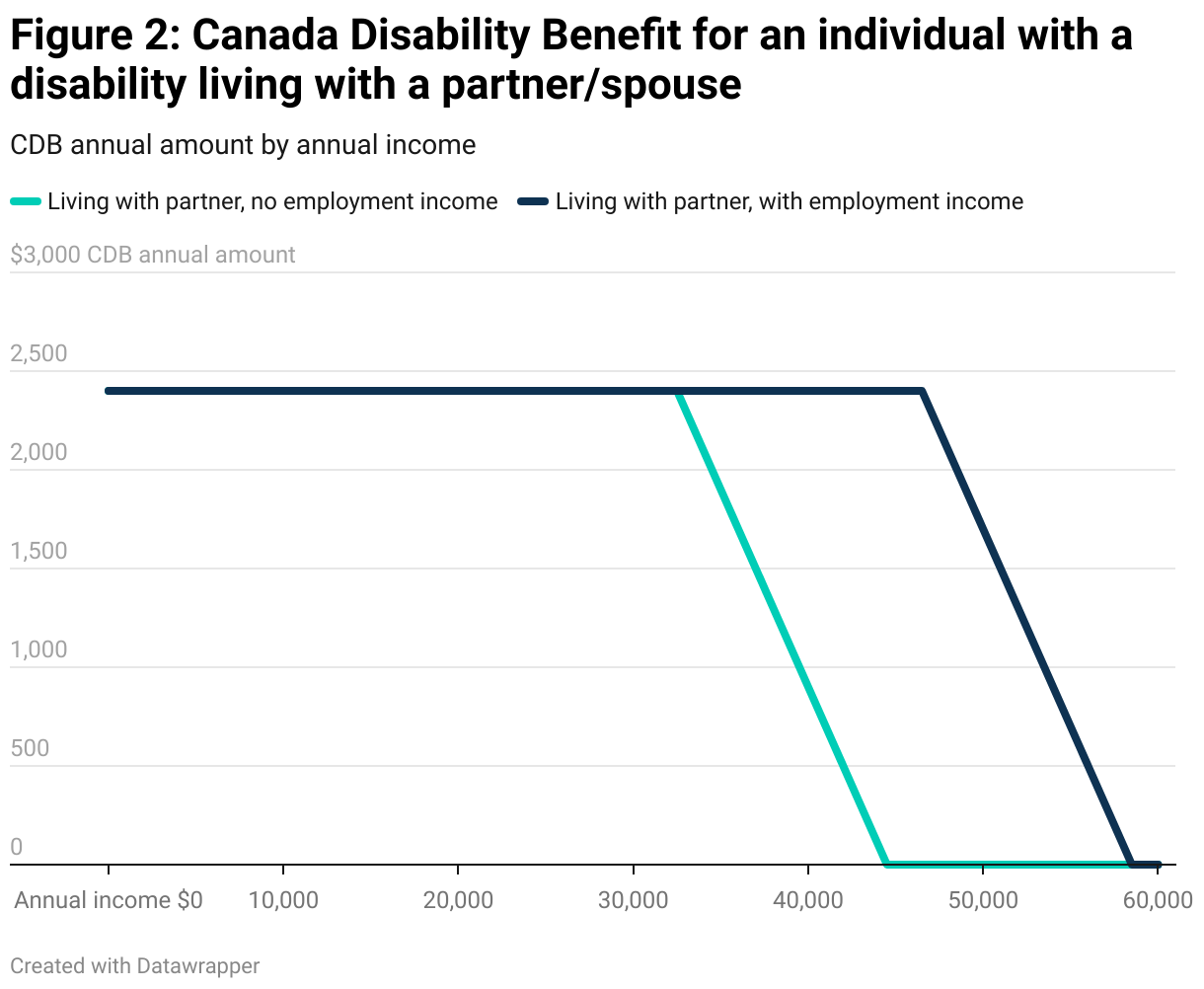

The benefit has been set at $2,400 per year or $200 a month (and to be adjusted annually for inflation thereafter) and is available to people with disabilities aged 18 to 64 years. Single individuals with total incomes below $23,000 are eligible for the full benefit. For people with disabilities living with a partner, the family income threshold for receipt of the maximum benefit is $32,500.

There is an earning exemption of $10,000 per year for individuals and $14,000 per year in combined income for those in a couple. In these instances, beneficiaries are eligible for the full benefit with total incomes of up to $33,000 and $46,500.

The value of the benefit is phased out above these cut-off points at a rate of 20 per cent, that is, a reduction of 20 cents for every dollar of income above the threshold. For example, for an individual without additional earnings, the benefit phases out completely at $35,000, and $44,500 for individuals in couple families.

In order to qualify, applicants must be residents in Canada for the purposes of the Income Tax Act—here including Canadian citizens, permanent residents, temporary residents who have lived in Canada for the previous 18 months or more, and refugees.

Applicants must also have a Disability Tax Credit (DTC) certificate. The DTC is a non-refundable tax credit that was introduced to provide tax relief to individuals with “severe and prolonged impairments” that impact their daily lives. To qualify for the DTC, individuals must obtain formal certification from a designated health provider with regard to the type, extent and expected duration of their disability.

A DTC certificate is currently required to establish eligibility for a range of disability-related programs such as the Child Disability Benefit, Canada Disability Savings Program and Home Buyer’s Plan. It is now being proposed as the tool to establishing disability status for the purposes of the Canada Disability Benefit.

Government proposal falls short of community needs and expectations

The stated goal of the Canada Disability Benefit Act is to reduce poverty and support the financial security of working-age persons with disabilities. Yet, its very design ensures that it will have a negligible impact on those most in need. The decision to require a Disability Tax Credit certificate as a means “to certify an impairment” as well as the very low benefit level on offer guarantees that only a small number of people with disabilities will receive any support. Fewer still will be lifted out of poverty.

This brief looks at these two critical issues and proposes alternative strategies to more effectively deliver on the promise of the Canada Disability Benefits both by making it much easier to access immediately and showing how a higher benefit level could yield larger reductions in poverty.

1. Disability Tax Credit: Not fit for purpose

The Disability Tax Credit is notoriously difficult to access and its receipt is highly skewed toward older taxfilers and upper income households—a point that the disability community forcefully stressed in early consultations regarding CDB design and is well documented in numerous reports. For example, a recent study from the Department of Finance found that only 13.5 per cent of people with disabilities (roughly 778,000 people of an estimated population of 5.8 million adults) had claimed the DTC on their tax form in 2017. And only 8.1 per cent–or 467,000 claimants—had realized any personal federal tax savings as a result of the claim.2

These figures include all adults aged 18 years and older across all income groups. The number of working-age claimants is predictably much smaller, and the group living in low income, even smaller still.

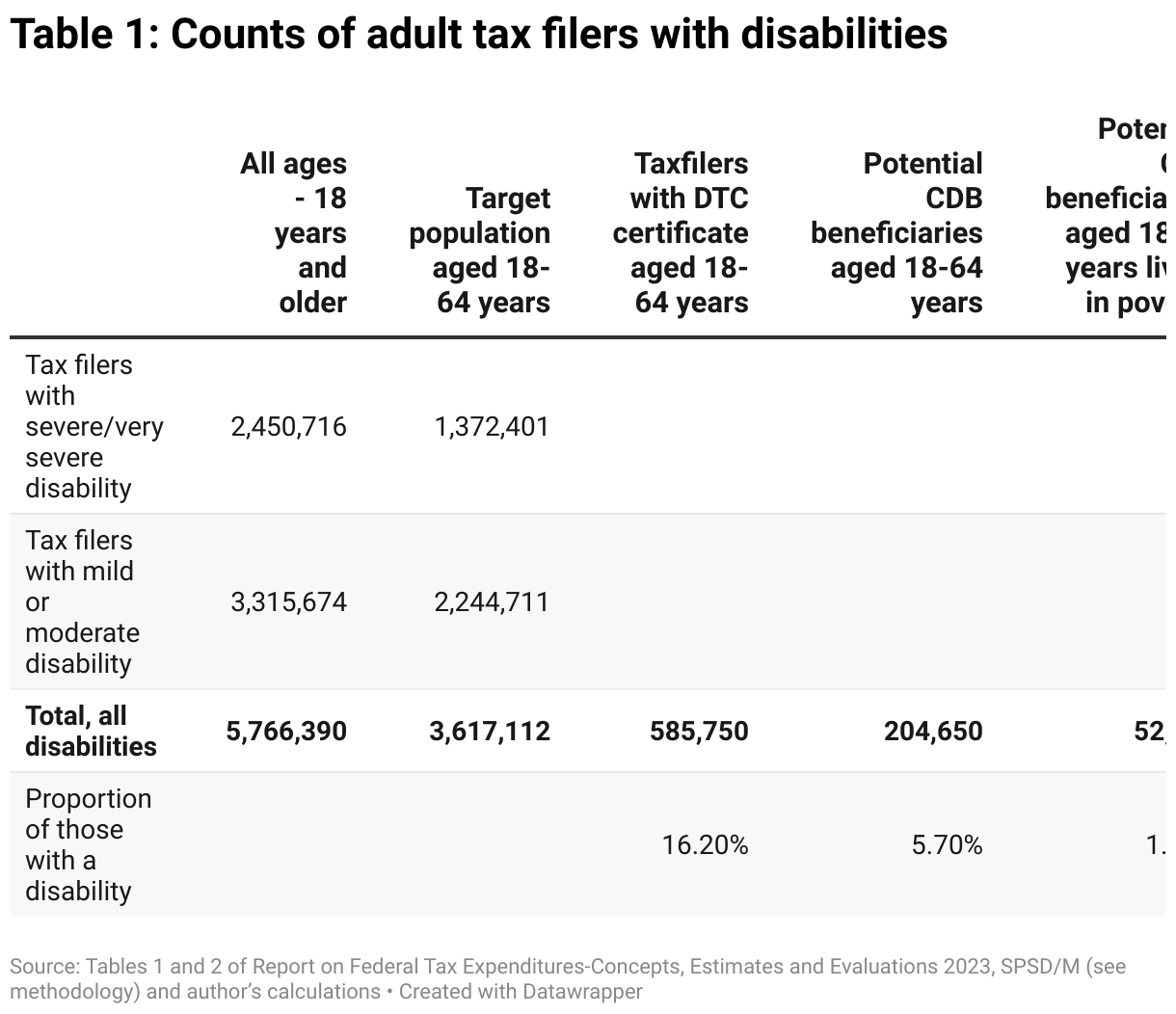

We know from the Canada Revenue Agency that there were 585,750 DTC certificate holders aged 19 to 643 in 2022, 40 per cent of all individuals with “accepted” certificates. Given that there are 3.6 million tax filers aged 18 to 64 with a disability—1.4 million of whom have a severe or very severe disability—starting with the DTC certificate as the sole entry criteria places the majority of people with disabilities at a severe disadvantage. Only 16.2 per cent of those with a disability aged 18 to 64 will have the requisite paperwork to apply for the Canada Disability Benefit.

Using Statistics Canada’s Social Policy Simulation Database and Model (SPSDM—see the methodology section), we are also able to estimate how many people with disabilities aged 18 to 64 years also have incomes below the CDB income thresholds. Our calculations suggest that only 204,650 (or 5.7 per cent) of people with disabilities in this age group will potentially benefit from the CDB.

And of this group, only 52,800 had incomes below Canada’s official poverty line (Market Basket Measure). This represents 1.5 per cent of all people with disabilities aged 18 to 64 and a fraction (5.8 per cent) of the 911,000 working-age adults with disabilities living in poverty as reported in the 2022 Canadian Income Survey. Clearly using the DTC certificate is a grossly inadequate starting point for determining eligibility for the CDB.

These findings aren’t a surprise. The Disability Tax Credit is designed to target those with “severe and prolonged impairment in specific areas of daily living” but it has two key drawbacks. First, the complexity and the expense of the process of applying for a DTC certificate, including securing a note from a medical professional certifying impairment, deters millions from applying. Second, it’s a non-refundable tax credit—meaning that if someone already has enough tax credits to reduce their taxes owing to zero, there is no point in going through the application process for a DTC. Many don’t apply at all because their incomes are so low that a potential tax deduction is of no value to them.

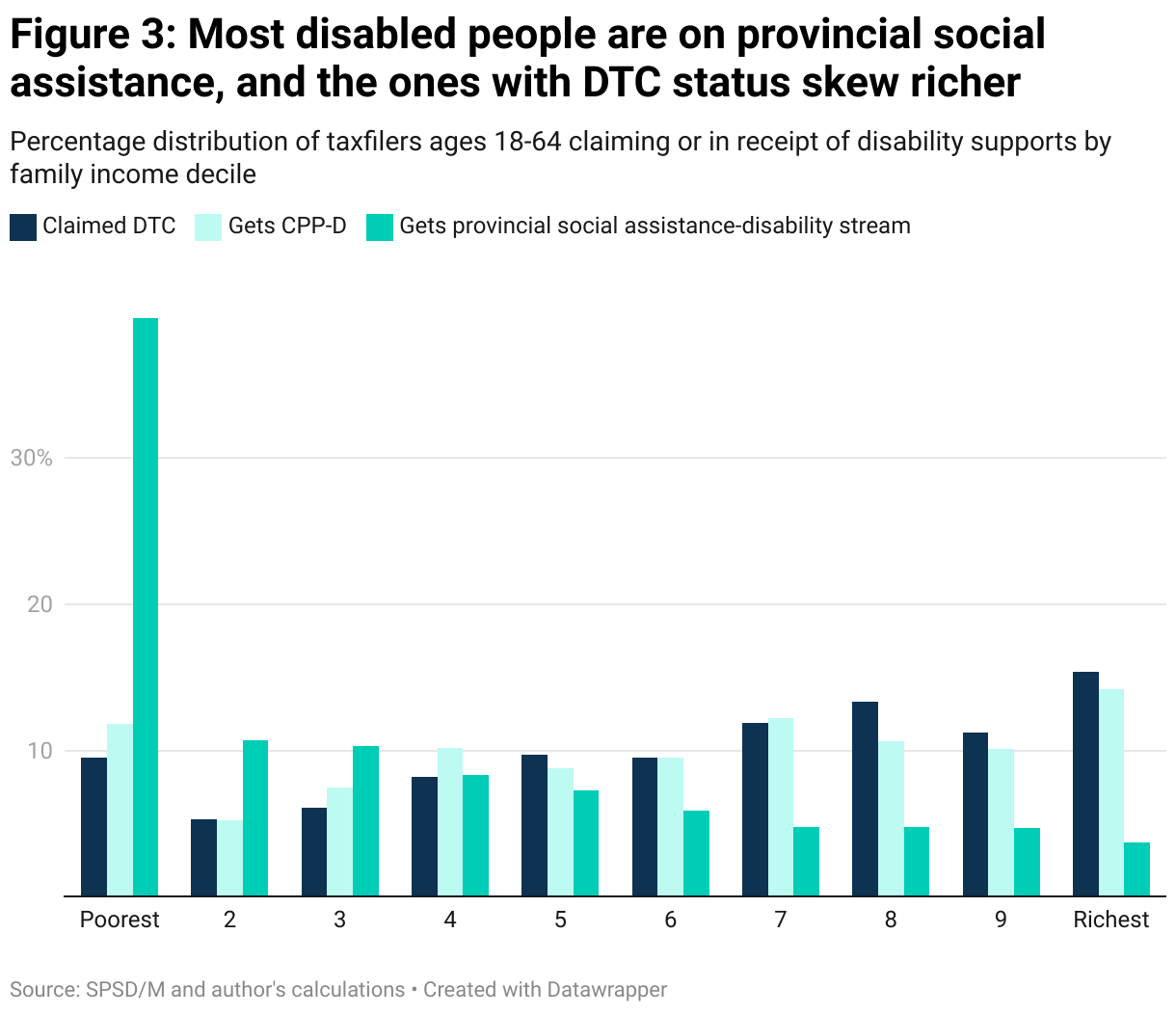

Compared to other programs that support those with disabilities such as social assistance and the Canada Pension Plan Disability Benefit (CPP-D), the DTC is very regressive. Only 10 per cent of DTC claimants aged 18 to 64 years have family incomes below $26,000—the cutoff for the poorest 10 per cent of the Canadian households. On the other hand, 40 per cent of people with disabilities on social assistance are in the lowest income deciles (See Figure 3).

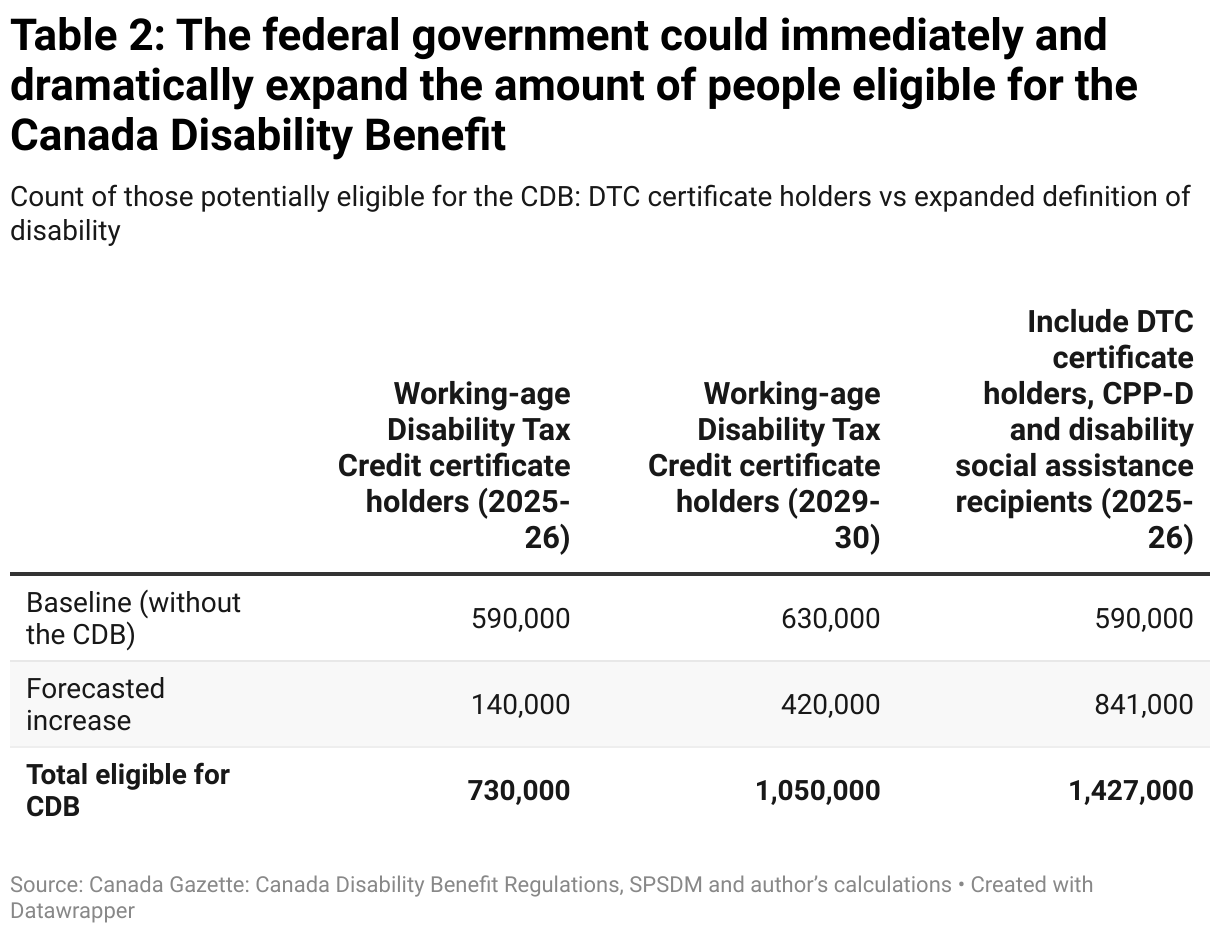

The federal government is aware of the problem and has allocated $22.4 million over five years starting in 2025-26 to support community navigation services and another $243 million over six years to help cover the fees charged by medical practitioners to complete required DTC medical forms. The program analysis and costing included in the proposed regulations suggest that the government hopes to boost the number of DTC certificate holders aged 18 to 64 from 590,000 to 730,000 by next July, and potentially to 1.1 million by the end of the decade.

These are optimistic projections. It remains to be seen whether the government will be able to meet these targets. If they do, all to the good. But at the end of six years—and much time and stress for people with disabilities—millions of Canadians aged 18 to 64 with disabilities will still not have the necessary approvals to potentially qualify for the Canada Disability Benefit.

The government argues that it is choosing to use the DTC to establish eligibility for the CDB because this decision will allow it to get the program up and running as quickly as possible. The DTC offers a “consistent and equal approach to determining disability eligibility…across all jurisdictions.” Relying on other provincial or territorial programs with their own disability criteria would “potentially create disparities” where an individual might qualify for the CDB in one jurisdiction but not in another.

Building on existing program architecture is a good approach for launching a program quickly. But given the scale of the need and the clear flaws and biases in the existing DTC program, leveraging other programs such as the Canada Pension Plan-Disability (CPP-D) benefit would immediately capture many more low-income people in need. There will be administrative challenges involved in program harmonization to resolve over time, including settling on a single definition of disability for assessing eligibility.4 That said, expanding the pool of applicants in this first phase of development by relying on other well-established programs is a more effective strategy for meeting the CDB’s poverty reduction goal and providing immediate relief to people with disabilities living in poverty. Forcing hundreds of thousands of people through another disability certification process for equity’s sake is an odd way to apply the concept.

If we expand eligibility for the CDB to not only DTC certificate holders, but also to people in receipt of the CPP-D program and those receiving social assistance through a disability stream, the number eligible for the CDB triples immediately from 590,000 people eligible to 1.4 million on day one. This wouldn’t cost $243 million dollars or take six years.

Other existing sources for rapid admission to the CDB should also be considered including long-term workers compensation, veterans’ disability benefits and private insurance disability benefits. Unfortunately, we aren’t able to model these changes as these programs are not included in SPSDM. But changing the eligibility criteria for the CDB could rapidly expand the pool of potential beneficiaries without forcing people with disabilities to undertake screening over and over again.

As currently proposed, only 204,650 people with disabilities aged 18 to 64 years will actually benefit from the new Canada Disability Benefit. By expanding the eligibility to include those receiving CPP-D or disability-based social assistance, a total of 798,000 people with disabilities would receive some benefit from the CDB. In total, 1.8 million beneficiaries and family members would benefit from the receipt of the CDB. The number of potential beneficiaries will be larger still if the government moves forward with its plans to enhance the rolls of DTC certificate holders.

2. Benefit level: Inadequate to the task of reducing poverty

Economic stress and hardship define the lives of millions of people with disabilities. In 2022, the median after-tax income of all persons with disabilities was $31,100, exactly three-quarters of the income of people without disabilities ($41,300). Among adults aged 25 to 64 years, 14.6 per cent or 911,000 lived in poverty (using the Market Basket Measure definition). Over one-third (35.9 per cent) lived on less than $30,000 per year and two-thirds (64.5 per cent) lived on less than $50,000 per year. For people with severe or very severe disabilities, the proportion living on very low incomes was even higher.

People with disabilities living on social assistance are, by definition, poor. In 2023, welfare incomes for single individuals with disabilities ranged from a high of $23,473 in Alberta to a low of $11,648 in New Brunswick. According to the Maytree Foundation, the welfare incomes of all single individuals with disabilities were below Canada’s Official Poverty Line (Market Basket Measure)—indeed the majority were living in deep poverty defined as below 75 per cent of the poverty line.

As a result of low incomes, people with disabilities are forced to make daily decisions as to whether to fill prescriptions, buy nutritious food, or use precious energy to take public transit to local food banks—all while fearful that they may jeopardize their eligibility for benefits or access to subsidized housing. In 2022, for example, more than half of people with disabilities—nearly 4.5 million people—reported having at least one unmet need when it came to either aids, devices, medication or healthcare services. Of this group, almost three-quarters (3.2 million) cited cost as a reason for those needs going unmet.

People with disabilities are also more likely to live in food insecure households compared to those without a disability. A 2023 survey of Canadians found that 28 per cent of people with a physical disability and 39 per cent with a mental disability reported going hungry in the previous 12 months because of lack of money for food.

The federal government has said that it ‘aspires’ to see the combined amount of federal and provincial/territorial disability supports grow to the level of Old Age Security (OAS) and the Guaranteed Income Supplement (GIS)—about $20,000 per year. However, at its current level of $2,400 per year, the proposed Canada Disability Benefit barely makes a dent in this objective. (For reference, the poverty line for a single individual is on average $25,778 a year5).

There is also significant concern about the proposed structure of the CDB itself as a “tax reportable but untaxed” benefit—and not as a refundable tax credit like the Canada Workers Benefit. Such a structure will make it easier to claw back the CDB from social assistance as is the case with other similar supports and potentially impact calculations for subsidised housing and related federal and provincial credits as well. Some beneficiaries could well end up being net losers and experience increased financial insecurity as a result of receiving the new CDB. Making the CDB a refundable credit would ensure that its value is automatically exempt from other key disability support programs.

The key point is that the proposed value of the benefit is too small to move any but a few above the poverty line and its current structure may result in further losses. Our modelling shows that if the CDB were implemented, based on current DTC counts, only 10,000 people would be lifted above the MBM poverty line here including beneficiaries and family members.

Even if the value of the CDB was substantially increased to $8,000 a year, for example, still only 36,000 people would be lifted out of poverty, assuming no change in the count of DTC certificate holders (see Figure 4). This finding demonstrates again the serious limitations and damaging consequences of using DTC certification as the sole eligibility criteria.

As Trevor Manson, co-chair of the ODSP Action Coalition, said in response to Canada Disability Benefit announcement in Budget 2024: “Aspirations are not plans. Aspirations are not going to lift people out of poverty.”

This doesn’t have to be the case. If we expand the eligibility criteria as described above to include not just DTC certificate holders but also those receiving CPP-D and disability social assistance, the benefit’s poverty impact is substantially improved with an immediate boost in the number of CDB beneficiaries.

Figure 4 compares the poverty impact of the original program without DTC expansion to a program that also includes those receiving CPP-D and disability-based social assistance. As the value of the CDB increases from $2,400 up to $9,000 a year, the number of CDB beneficiaries and its poverty impact grows. A Canada Disability Benefit worth $9,000 per year would potentially reach over one million beneficiaries and lift 278,000 people with disabilities and their family members out of poverty (See Table 3). Alternatively, a benefit of $7,000 a year would lift 212,000 people out of poverty.

Expanding the numbers supported by the Canada Disability Benefit will require a larger budget. We estimate that the proposed bare-bones version of CDB using the DTC as the primary eligibility criterion, assuming no change in the number of DTC certificate holders, would cost $413 million in the program’s first year (2025-26) as shown in Figure 5.

Adopting a broader definition of disability, as discussed above, would increase program costs to $1.7 billion. As the benefit level rises above $2,400 per year, program costs increase again, reaching just over $8 billion for a CDB with a benefit of $9,000 per year or $5.9 billion for a benefit of $7,000 annually. For comparison, elderly benefits including Old Age Security and the Guaranteed Income Supplement are forecast to cost $85.3 billion in 2025-26 and currently support over 6.8 million Canadians.

Conclusion

The introduction of the Canada Disability Benefit is a milestone for people with disabilities, but this barebones version doesn’t begin to address the devastating poverty and economic struggle that define people’s lives. The disability community is rightly disappointed about the sizable gaps in this program and the level of assistance on offer.

This brief proposes alternative strategies to more effectively deliver on the promise of the Canada Disability Benefits both by making it much easier to access immediately and showing how a higher benefit level could yield larger reductions in poverty. We recommend that the Government of Canada:

- Expand the pool of potential beneficiaries by including the Canada Pension Plan-Disability (CPP-D) and social assistance programs as additional routes to accessing the CDB.

- Investigate other disability programs such as workers compensation and those from private insurance as potential vehicles for establishing disability status.

- Increase the maximum benefit of $2,400 per year to meaningfully address the high levels of poverty that people with disabilities experience and the high cost of living associated with having a disability.

- Take action to ensure that the Canada Disability Benefit is exempt from calculations determining eligibility for other federal and provincial supports including social housing (e.g., exempting the CDB from the calculation of Adjusted Family Net Income).

Methodology

The analysis above relies heavily on “glass box” changes to Statistics Canada’s tax modelling software Social Policy Simulation Database and Model version 30.1 (SPSDM). The assumptions and calculations underlying the simulation were prepared by David Macdonald and the responsibility for the use and interpretation of these data is entirely that of the author.

Identifying DTC certificate holders

The Canada Revenue Agency estimated that in 2022 there were 585,750 people aged 19 to 64 with a Disability Tax Credit Certificate. Of those 585,750 people, the custom SPSDM changes were able to identify 519,790 of them. Therefore, this analysis is an undercount of the current DTC certificate holders by 11 per cent.

For this analysis, if a person aged 18 to 64 claimed the DTC credit for themselves then they were included as DTC certificate holders. If others claimed the credit on a person with disabilities’ behalf, the process was more involved.

If there was a dependent disability claim and there was a senior or a child under age 18 in the economic family, then that person was assumed to be the DTC holder and was generally excluded from this analysis.

Where a child or senior wasn’t found, their economic family was searched to find out whether there was anyone aged 18 to 64 living in the household who was receiving social assistance, the Canada Pension Plan Disability benefit, workers’ compensation benefits or if they were flagged as an adult dependent. These are all good indicators that that person has a disability. If a match was found, and that person wasn’t the claimant’s spouse, then that person was flagged as the DTC certificate holder.

If this process didn’t produce a match, the economic family was again searched to see if there was a person aged 18 to 64 with under $2,000 in federal and provincial taxes owing and who wasn’t the claimant’s spouse. If so, that person was flagged as a DTC certificate holder.

There were 45,000 instances where a suitable DTC certificate holder couldn’t be identified, likely because they lived at a different address and/or weren’t in the same economic family. These instances were all excluded.

Identifying social assistance recipients with disabilities

SPSDM models the social assistance received by an individual but doesn’t have data on the type of benefit received, that is, whether the person is a recipient of a disability stream of social assistance or not. However, we know that half of all social assistance recipients are receiving benefits through a disability stream and that the proportion rises to 68 per cent when looking at singles living alone. Using the Maytree Social Assistance Summaries, a matrix was created to show the probability by province and by family type of a social assistance recipient being part of a disability stream. As each social assistance recipient’s province of residence and family type is known, they were randomly assigned to a disability stream using the probabilities from the matrix. This is the process that was used to simulate the expansion of the CDB to those receiving social assistance.

Identifying CPP-D beneficiaries

Receipt of the Canada Pension Plan-Disability benefit for those aged 18 to 64 years is a variable in SPSDM. It was used in the expanded definition of disability proposed and modelled in this paper.

Full comparison of results

Table 3 provides a full comparison of various scenarios and their impacts as discussed earlier in the analysis.

Notes

- The Canadian Centre for Policy Alternatives is a charitable research institute and Canada’s leading source of progressive policy ideas, whose work is rooted in the values of social justice and environmental sustainability.

- A significant proportion of the tax savings from the DTC (42 per cent) directly benefits people without disabilities, typically other family members providing support or care. Of the remaining 58 per cent, people with mild or moderate disabilities account for 19 per cent of total benefits received and those with severe or very severe disabilities account for the final 39 per cent.

- The CRA figures are presented for those aged 19 to 64 in 2022 (and not the CDB target group of those aged 18 to 64 years). The Regulatory Impact Analysis Statement published in the Canada Gazette starts with a value of 590,000, presumably a rounding from the CRA figures.

- The government should bring the definition of disability used for the purposes of the Disability Tax Credit into alignment with the definition of disability chosen for the Canada Disability Benefit Act and Canada Accessibility Act. This is also an important step to ensuring that those in need will have access to the new benefit.

- This threshold is an average for all community sizes across all provinces.