Fast Facts

Governments of all stripes are scrambling to address the housing supply shortage in municipalities across the country, especially in major cities. From the federal Housing Accelerator Fund to Ontario’s now-aborted plans to open up the green belt for sprawling suburban development, governments are working to set the private sector loose to build, build, build.

As this has been happening, the Bank of Canada has been on a multi-year campaign of raising interest rates to bring down inflation. The explicit goal of interest rate raises is to “cool” the economy. How has that program been affecting housing prices?

A quick look at the numbers shows a dire situation for new builds in the private sector.

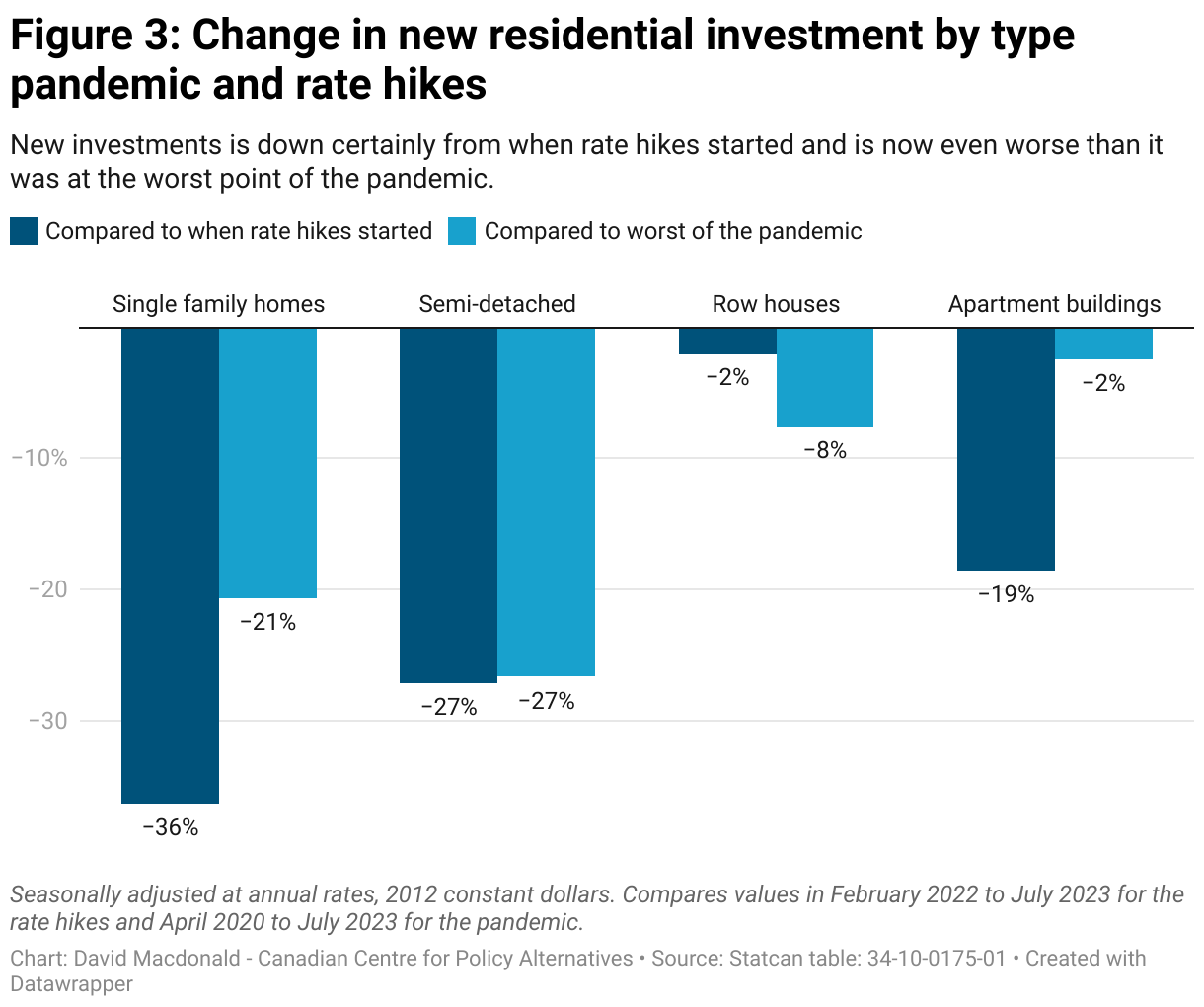

- Developers are investing less in new residential housing construction than they were in April 2020—the height of pandemic economy shutdown. Compared to the worst of the pandemic, investment in new single-family homes is down 21 per cent. New row homes are down eight per cent, and new apartment construction is down two per cent.

- Compared to February 2022 when rate hikes started, the numbers are even more dire. Investment in single-family homes is down 36 per cent, semi-detached houses declined by 27 per cent, new row home construction saw a mild decline of two per cent, and apartment buildings cratered by 19 per cent.

- The Bank of Canada estimates that the worst impacts of rate increases take two years to hit the housing sector and the housing sector is the main vehicle for rate hikes to hit the economy. Right now, it has been 18 months since the first rate increases, but most of the bigger rate increases have occurred in the past 12 months—so the worst is yet to come.

Our content is fiercely open source and we never paywall our website. The support of our community makes this possible.

Make a donation of $35 or more and receive The Monitor magazine for one full year and a donation receipt for the full amount of your gift.

What’s happening in housing?

Housing prices—for new purchases, mortgage carrying, and rent—are at or near all-time highs. Desperate governments, at all levels, are encouraging the private sector to build anything in the hopes this will have an impact on prices and rents. Policymakers are going for new supply at any cost—justifying everything from the now-cancelled sprawl development plan of the greenbelt around Toronto, to the elimination of GST on the sale of new apartment buildings. The goal is supply, any supply in the hopes that more will cut house prices.

These private sector incentives may have been effective in 2019, but their relevance is rapidly receding. In 2022, the Bank of Canada implemented historic interest rate hikes, deeply suppressing private housing investment—which sunk to levels worse than during the early days of COVID-19, when parts of the industry were shuttered.

Whatever minor help private sector incentives might be in building out more housing, they are totally overwhelmed by high interest rates.

Today, new housing construction in the private sector is at a lower level than it was at the worst point in the pandemic economy shutdown—when a significant share of the construction industry was completely shut down. If governments are serious about increasing housing supply, these numbers should make them hit the panic button.

By their own admission, the Bank of Canada’s rate hikes won’t fully hit the housing sector for two years after they begin. Right now, it’s been 18 months since the very beginning of the rate hikes—and most of them have taken place in the last year. That means that we’re still only in the beginning of what could be a precipitous decline in private sector housing investment.

The private sector is locked in to a period of declining investment in home construction because of rate hikes, and all levels of government are ignoring this fundamental reality. Federal and provincial policies continue trying to incentivize private sector construction, but those policies cannot make up for the lost ground to rate hikes.

If governments are serious about building new housing supply, they need to get back in the housing game themselves. We’ll get to that later, but first, let’s break down what’s happening in the housing sector right now.

We’re building less now than during the early pandemic economy shutdown

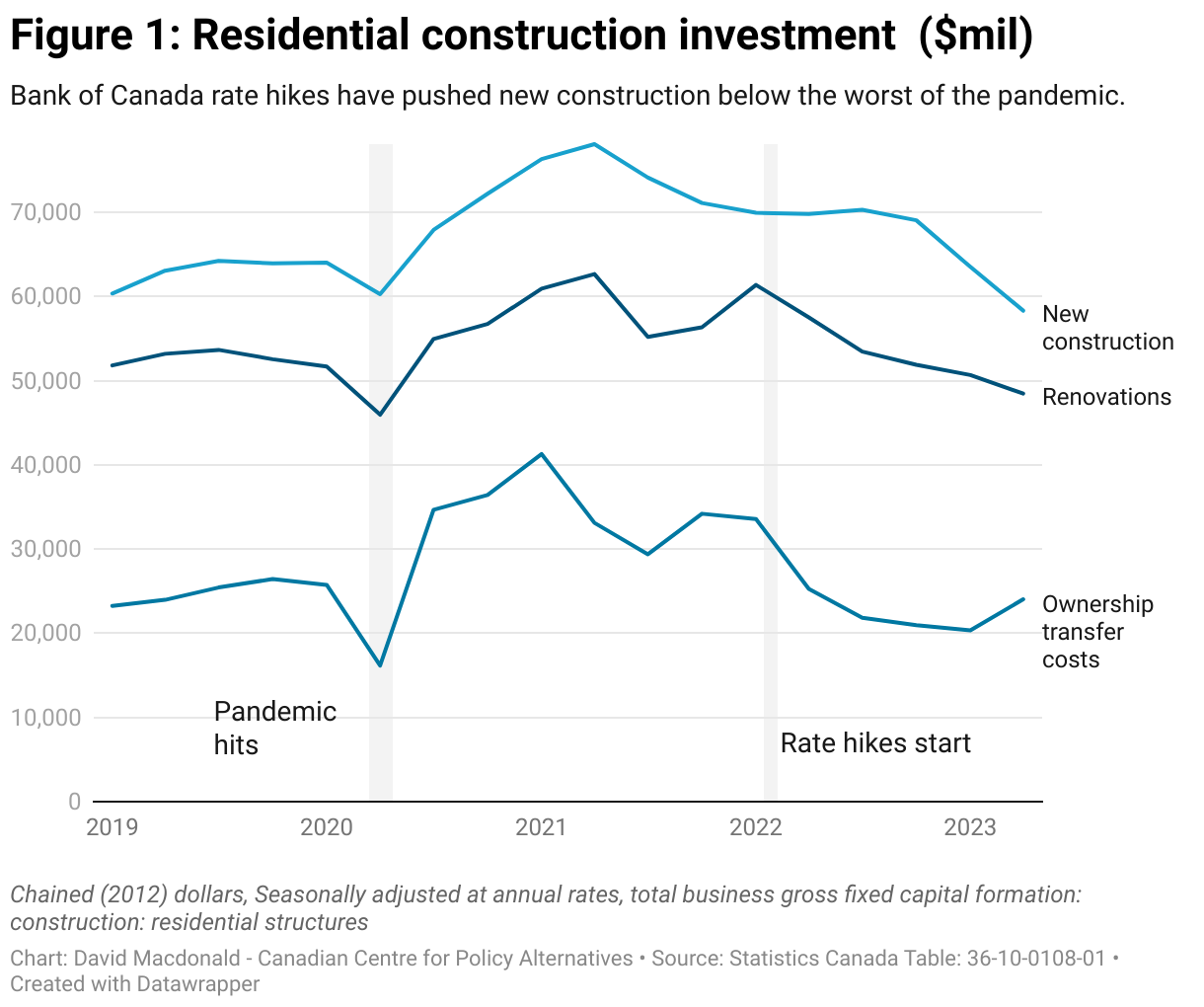

Interest rates are having a devastating effect on residential construction whether in new builds, renovations or ownership transfer costs (like real estate commissions).

Investments in new home builds is down 17 per cent compared to Q1 2022, before the hikes started. Renovations are down 21 per cent and ownership transfer costs (like real estate commissions) are down 28 per cent. Real GDP hasn’t grown at all between January and July 2023 and cratering residential investment is a key driver of that stagnation.

In Q2 of 2020, when COVID-19 hit, we saw new housing construction significantly depressed. In several provinces, COVID-19 lockdowns straight up stopped new home construction. In summer 2021, there was a surge in new residential construction to catch up for lost time.

The latest data shows new residential construction is actually below the worst of the pandemic economy shutdown, when big parts of the construction industry was shut down—and it’s still falling. The full impact of rate hikes on new builds is nowhere near fully realized yet. These huge drops will completely overwhelm the measures taken so far by governments to incentivize private construction.

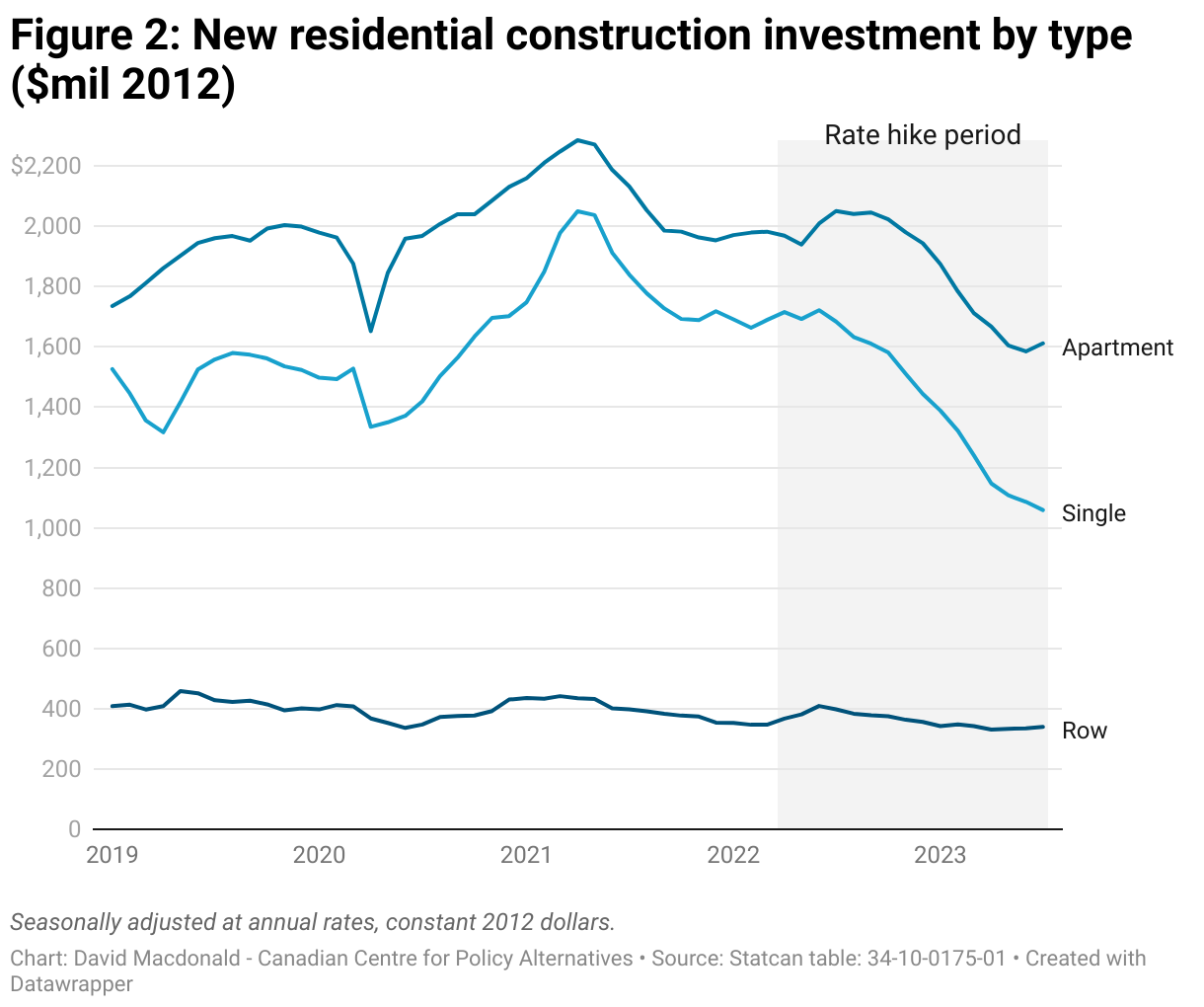

It’s also possible to look at the rates of construction by unit type, dividing between single family homes, apartment buildings, and row houses. These figures are presented in seasonally adjusted, constant dollars to remove the impact of inflation on building materials and the strong seasonality of the construction industry. By doing so, we see the big drop in investment during the COVID-19 lockdowns, but we can also see the substantial recovery the following summer.

Rate hikes started slowly with the Bank of Canada overnight rate moving from 0.25 per cent to 0.5 per cent in March 2022 to then to one per cent in April. Rates rose quickly over the summer of 2022 hitting 3.25 per cent in September 2022. We saw some increases in new construction, particularly in row houses and apartments, in summer 2022—but by summer’s end there were declines in all major unit types.

Since last summer, rates have only continued to rise and new residential construction investment continued to decline.

The most recent data is from July 2023, where new construction investment is decisively below the worst of the pandemic economy shutdown for single family homes, semi-detached and apartments. Investment in new row houses is around the same level as it was during the worst of the pandemic economy shutdown, when portions of the construction industry were completely shut down.

The impact of Bank of Canada rate hikes have been breathtaking. Investment in new single family homes is down 36 per cent between February 2022 and July 2023. Investment is down 27 per cent for new semi-detached houses and new apartment construction is down 19 per cent. Row houses are the only bright spot—down only two per cent since before the rate hikes started, although new row house construction saw a lull at the start of 2022, creating a favourable comparison point.

If we compare the July 2023 numbers to April 2020—the height of COVID-19 lockdowns, when whole industries were shut down—the numbers are still down. New single family homes were down 21 per cent compared to April 2020, row homes down eight per cent, and apartments down two per cent. It’s worth repeating—the private sector is currently investing less in new home construction that it was during the COVID-19 lockdowns.

Collapsing housing investment is how rate hikes are supposed to work

Cratering housing investment seems like a pretty serious political issue—but it’s exactly how the Bank of Canada expected rate hikes to hit the economy. Interest rate hikes don’t affect all parts of the economy equally. They take a serious bite out of some sectors, while leaving others relatively unscathed.

If you have to take out a loan to engage in a type of economic activity, higher interest rates matter. If you don’t need a loan, interest rates don’t have much of an impact on your economic activity. This means that higher interest rates increase carrying costs for businesses looking to build things like residential housing or consumers looking to buy those houses or cars.

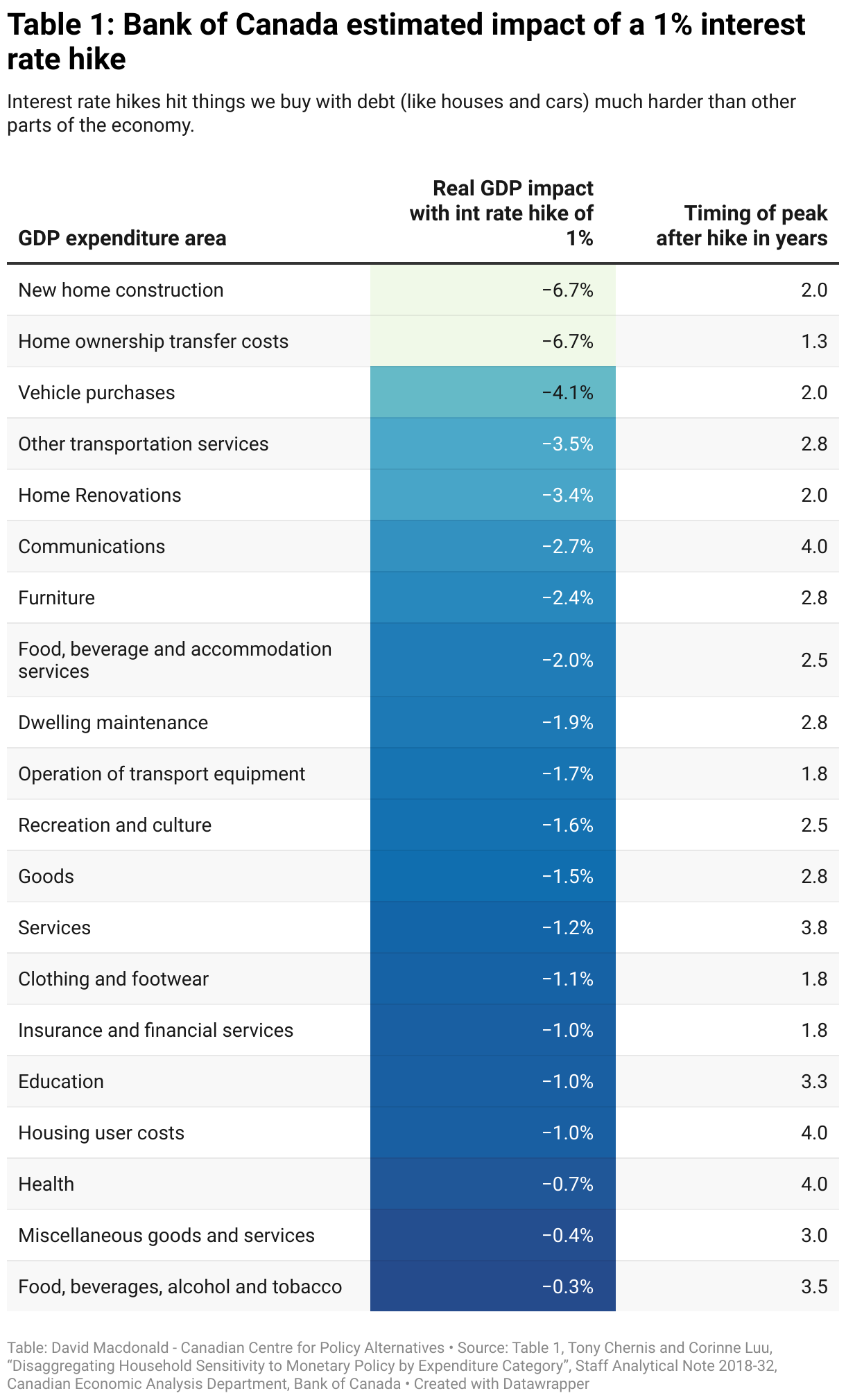

Table 1 was made from data the Bank of Canada produced before it began hiking interest rates in 2022. The central bank estimates how an interest rate hike of one per cent would impact the economy, and how long it takes to feel the full impact of the hike.

Interest rate hikes have the biggest economic impact on sectors related to housing—construction, renovations and homeownership transfers— well as vehicles. These are, of course, items most people buy with large debt loads, either mortgages or car loans. Businesses in the housing construction industry also take on large debts while completing a project and prior to its sale.

The economic activity in the food and beverages area, on the other hand, doesn’t change at all with an interest rate hike and sits at the bottom of the list.

The lag times that the Bank of Canada predicts are substantial for homes and cars. It takes two years before the full GDP impact is felt for home construction and vehicle purchases. This round of rate hikes only started in March 2022, 18 months from the date of this analysis. However, most of the hikes happened within the last 12 months.

By their own numbers, the Bank of Canada was fully aware that their rate hikes would hit the housing sector hardest. That was not an unfortunate side-effect—it was the central bank’s core plan. We can see that in its own research documents that they produced prior to this rate increase cycle—even if the Bank of Canada didn’t exactly make it clear when they were talking to politicians or the public.

Now, blindsided governments are scrambling to make up for the ground they’re rapidly losing on private sector construction—but they’re reaching for tools that will no longer work in this new high-rate context.

A path forward

SInce the Canada Mortgage and Housing Corporation withdrew from building apartments in the 1990s, the private sector has been the main force to finance, build and run housing either for rent or for sale. Despite government approaches that assume this will continue to be the case, the numbers show that it isn’t going to fly anymore..

The 2021 federal budget’s “housing accelerator fund” was meant to speed up municipal approvals of new builds. The feds recently removed the GST on the initial sale of purpose built rentals. Across the policy spectrum, the federal government is relying heavily on the private sector to take up the torch and build new housing supply. That’s already happening much less—and it’s going to get worse.

While these government housing initiatives may have limited positive impact, they are being made increasingly irrelevant by the impact of rate hikes. It’s as if governments are bringing a nail to the construction site but the Bank of Canada is bringing a wrecking ball.

The economics of private development in new residential construction has fundamentally changed. Builders aren’t sure they can move new units, and their own carrying costs during construction erase margins and scrub potential profits.

There is a way out—don’t rely on the private sector to build.

With higher interest rates, governments need to shift focus to filling in for the missing private sector themselves. This isn’t a time for more private incentives—it’s time to get your hands dirty. The federal government can and should be directly building non-market housing, or buying and converting units to non-market rent. They could build them directly or provide 0% mortgages to non-profit providers to do it. These are longer term solutions and unfortunately, building takes time. It can easily take ten years from land acquisition to people moving in, five years if the stars align.

In the shorter term, non-profit housing providers and universities/colleges could buy existing for-profit apartments and convert them into non-market buildings with lower rent. Governments could outlaw Airbnb and other short term rental platforms from big cities for five years to provide some breathing room for new builds. Municipalities could implement rapid city-wide upzoning to allow for new builds—we can save the green belt by opening up the single-family home belt.

All levels of government should work to strengthen and enforce rent controls. Governments could also implement large transfer taxes on investment properties and heavy restrictions on mortgages for investors.

Governments at all levels have been shouting about the housing crisis, and the need to build new housing supply, but their solutions are stuck in an era when the private sector was actually building homes. With private sector investments collapsing in housing construction, governments need to fill that gap.

It’s time for governments to take direct and ambitious action in the housing sector—to get back into the housing game, and stop relying on the private sector.

Acknowledgements: The author would like to thank Sheila Block, Alex Hemingway, Marc Lee, and Ricardo Tranjan for their helpful comments on an earlier draft of this paper.