Summary

This study looks at tax changes between 2004 and 2022, examining changes by the Paul Martin Liberal government, Stephen Harper Conservative government and Justin Trudeau Liberal government. It considers almost all sources of income, including corporate profits and other sources of income not normally counted in Statistics Canada’s tallies, and all taxes paid.

It finds that, overall, Canada’s tax system is only moderately progressive through the bottom half of the income distribution, and is regressive at the top of the distribution due to several sources of untaxed or lightly taxed income (such as capital gains, inheritances/bequests and employer-provided benefits) that predominantly go to top earners.

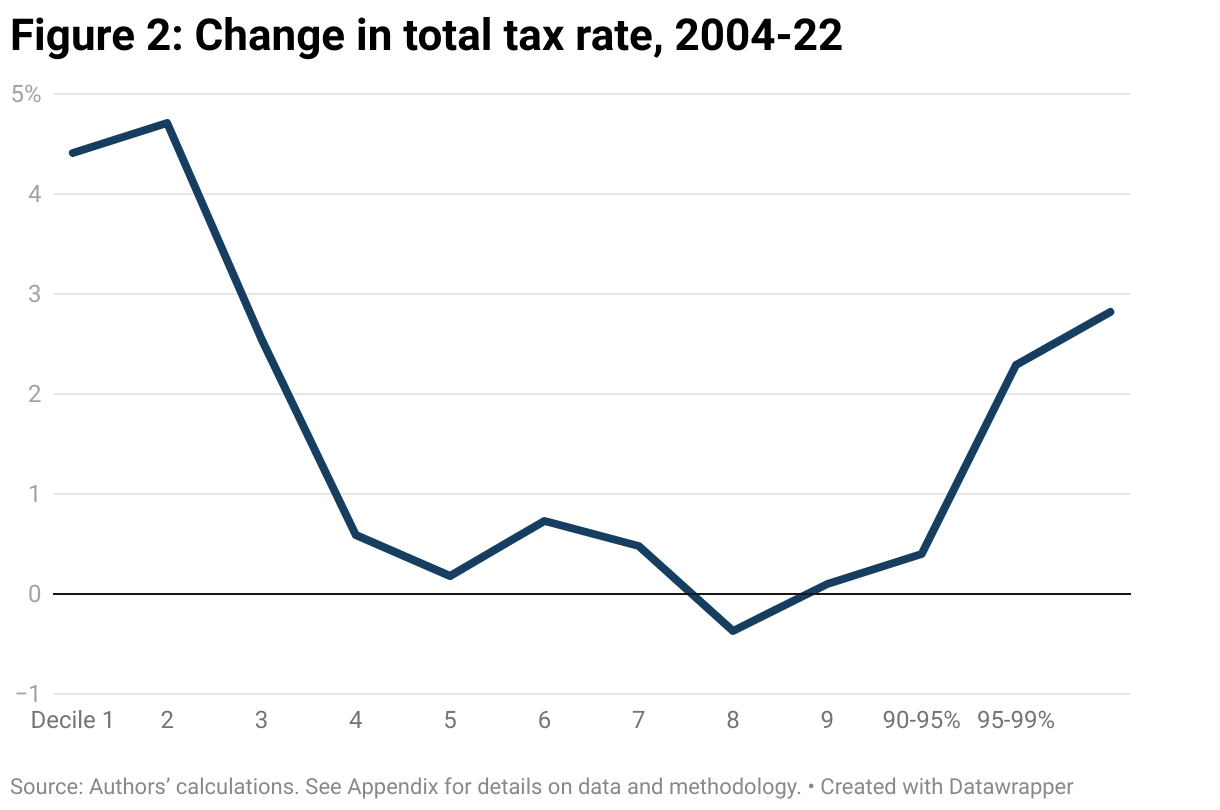

Since 2004, Canada’s tax system has become less progressive, with rates at the bottom of the distribution in 2022 as much as 4.7 percentage points of income higher for the bottom two deciles.

Excluding the top and bottom 10%, the tax system is relatively proportional (a flat tax structure). The average tax rate was little changed in 2022 (36.7%) compared to 2004 (36%), with the peak tax rates in the middle, at 43.8% and 43.5% respectively.

One positive development is that rates for the top 5% of households are somewhat higher in 2022 than 2004. Rates for the top 1% were also up by 2.8 percentage points in 2022 relative to 2004.

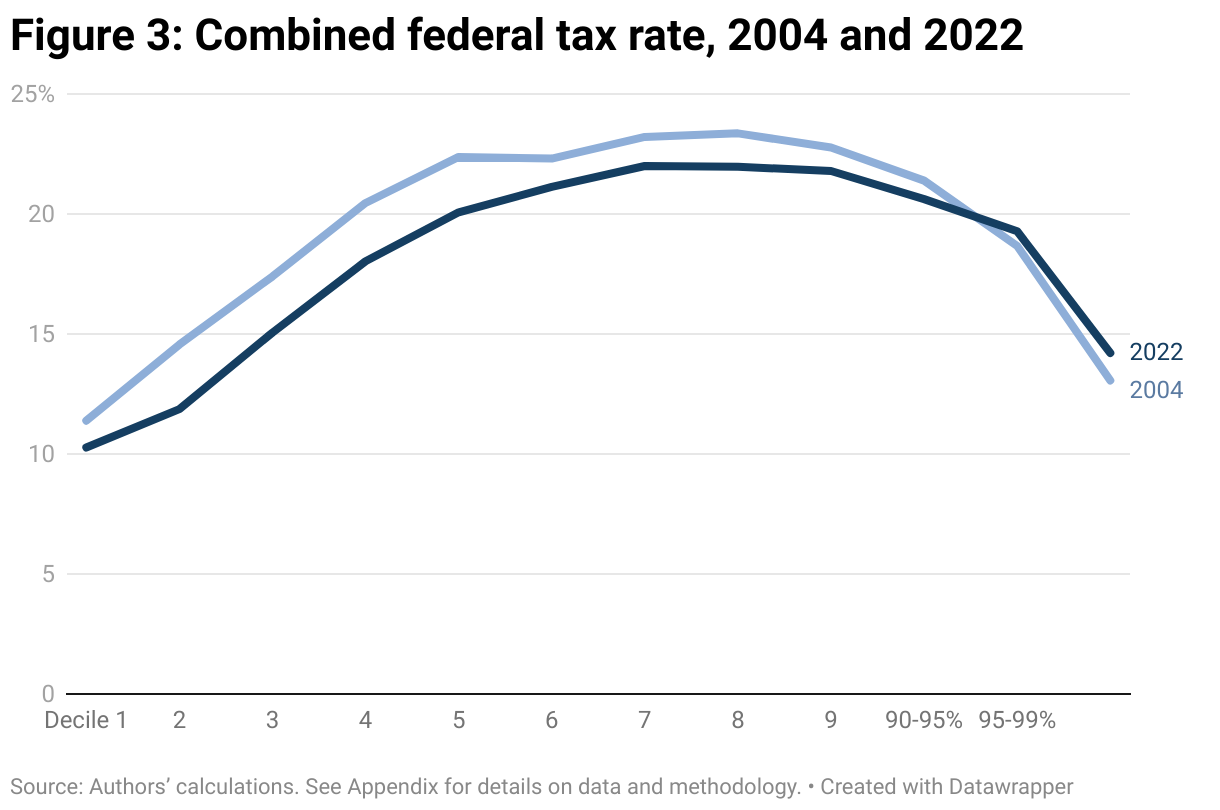

There was an overall reduction in federal taxes between 2004 and 2022, reflecting reductions in the GST and federal income tax between 2005 and 2008. An exception is the very top of the distribution, reflecting the 2016 addition of a new top income tax bracket. The mix of federal taxes is progressive up to the households in decile 7, then it flattens out and becomes regressive at the top.

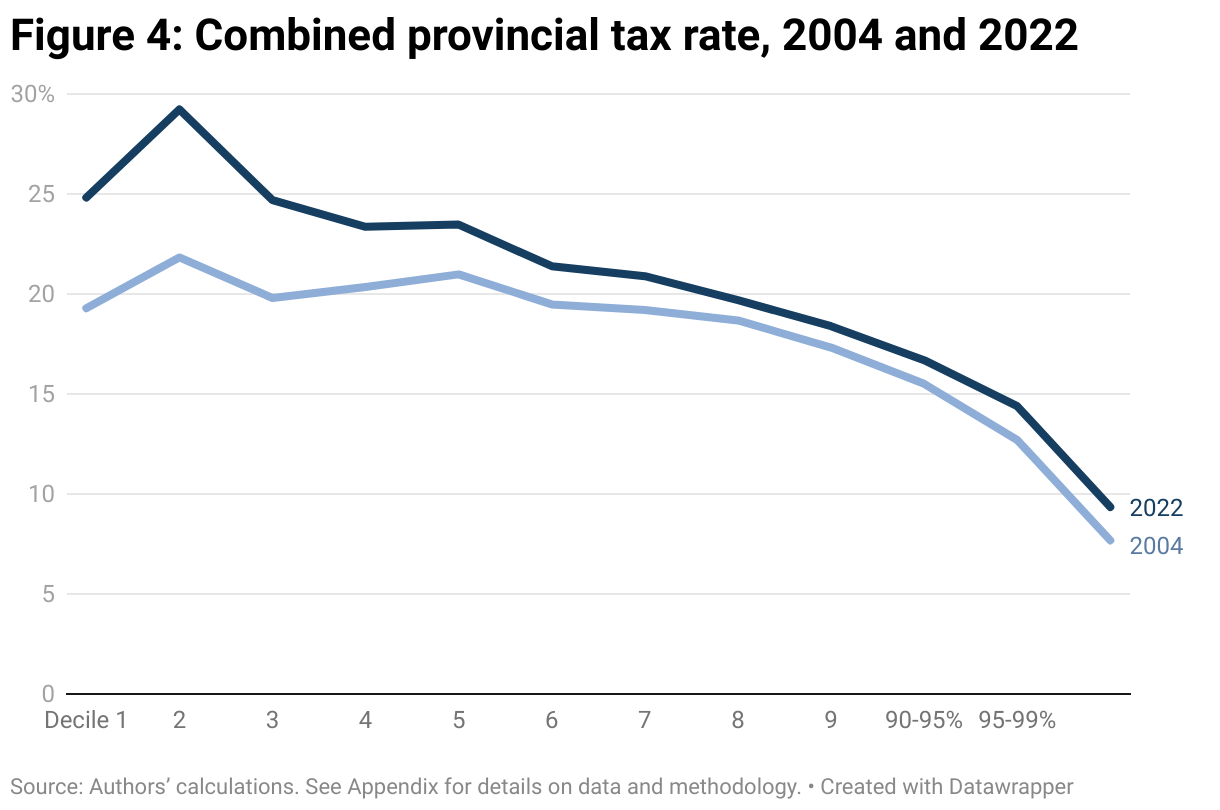

Reductions in federal taxes have been offset or more-than-offset by increased provincial taxes for all groups in 2022 relative to 2004. The distribution of provincial taxes is more clearly regressive across the whole distribution, and has also become more regressive at the bottom. In 2004, provincial tax rate was fairly flat up to decile 5 then regressive, but by 2022, it was completely regressive.

The 2004 to 2022 timeframe can be divided in two eras: the tax-cutting budgets of the Martin and Harper governments and a gradual improvement in progressive taxation on some fronts under the Trudeau Liberal government—some of which was undermined by provincial tax increases.

Corporate tax cuts figured prominently during the first half of our timeframe. The Conservative government of the day reduced the general corporate income tax (CIT) rate in a series of steps, from 21% in 2007 to 15% in 2012.

Under the Harper government, the GST was lowered from 7% in 2005 to 5% in 2008. The rate for the lowest income tax bracket was reduced from 16% to 15% in 2005, and the basic personal amount (exempt from income taxation) was increased above the rate of indexation between 2005 and 2009.

The Trudeau government in 2016 introduced a new top personal income tax bracket of 33%, while the rate on the second lowest bracket was reduced from 22% to 20.5%. In that same budget, the Canada Child Benefit combined and bolstered previous child and child care benefits.

Taxation of the wealthiest is a central means to reduce inequality, provide adequate shared public infrastructure and services that benefit all, and create opportunities for all to live a decent life. A return to more progressive taxation would improve fairness, while also providing a lever to directly reduce income and wealth inequality. Despite the progressive personal income tax system, when we look at all taxes and income, the tax system is only moderately progressive at the bottom, flat through the middle and regressive at the top.

Among our tax reform recommendations:

Increase the progressivity of the income tax system: While there have been some modest increases in the top marginal income tax rate federally and provincially, the income tax system could do a much better job at mitigating market-driven increases in inequality and the concentration of income and wealth at the very top. Top marginal tax rates in Canada exceeded 70% for a quarter-century after the Second World War and only fell to about 50% since 1982. A new top rate for capital gains inclusion in the 2024 federal budget is a small step in this direction.

Tax inheritances and wealth: To ensure that all Canadians contribute their fair share in taxes, large inheritances and gifts should be included in the recipient’s taxable income. Alex Hemingway calculates that a Canadian wealth tax applying to net wealth above a $10 million threshold with three brackets and rates (one per cent for net wealth above $10 million, 2% above $50 million and 3% above $100 million) would raise an estimated $32 billion in the first year alone, rising to an estimated $51 billion by the tenth year.

Raise corporate income taxes and bring in a windfall profits tax: Recent governments have delivered windfalls to certain corporations and sectors due to commodity prices determined outside of Canada (mega-profits going to oil and gas companies in 2021 and 2022, for example) or due to use of market power to increase prices (supermarket chains, most notably). A one-time windfall profits tax was brought in federally for the banking and life insurance sectors for the 2021 tax year. Ongoing windfall taxes can guard against excessive profiteering and make the CIT more progressive overall.

Introduction

The public sector represents a large share of all modern economies. Federal, provincial and local governments provide a wide range of public infrastructure and services and are, in turn, major employers. Governments also provide various income support payments to individuals and families. Thus, how tax revenue is generated and how the cost of taxes is allocated are central questions of social justice.

Because of the tax brackets applied to personal income, we often assume that the tax system is progressive, which means that as their income rises people contribute a progressively larger share of their income to taxes. However, personal income taxes are only one kind of tax. There are many other taxes that are regressive, which means people with higher income pay a lower share of their income to the tax, and many sources of their income are not taxed, or only lightly so.

What matters is how the mix of taxes is distributed across income groups, known as tax incidence. This paper presents the first update of tax incidence in Canada since Marc Lee’s 2007 paper, Eroding Tax Fairness: Tax Incidence in Canada, 1990 to 2005.1 This paper follows the methodological approach taken in that paper to look at changes between 2004 and 2022. This time period captures shifts in the tax system made by the Martin Liberal government, Harper Conservative government and Trudeau Liberal government.

We include additional income and taxes in our analysis that are not included in standard research looking at household taxation. We estimate a measure called broad income, which is a more comprehensive income concept than the conventional total income (market income plus income transfers) produced by Statistics Canada.2 Broad income includes Statistics Canada’s total income and adds corporate pre-tax profits, employer-provided benefits, realized capital gains, inheritances and bequests. All of these sources represent command over resources and thus should be included as broad income.

On the tax side, we include all federal and provincial personal and corporate taxes as detailed in the Department of Finance’s Fiscal Reference Tables.3 These include federal and provincial income, sales/commodity and payroll taxes, as well as local and provincial property taxes. More detailed background and discussion of data sources and methodology are provided in the Appendix, including some differences in the current paper compared to Lee’s 2007 paper.

In the next section, we review the key changes in federal and provincial tax systems over the 2004 to 2022 period. We then review our results, with breakdowns of total taxes, federal and provincial taxes, as a share of broad income. Finally, we discuss implications for tax reform in light of these findings.

Major federal and provincial tax changes

A number of changes to the federal tax system occurred between 2005 and 2008, with tax-cutting budgets delivered by both the Martin Liberal and Harper Conservative minority parliaments. The GST was lowered from 7% to 6% in 2006 and to 5% in 2008, while the GST credit4 was maintained at previous levels. In addition, the rate for the lowest income tax bracket was reduced from 16% to 15% in 2005, and the basic personal amount (exempt from income taxation) was increased above the rate of indexation between 2005 and 2009.

Federal income tax reforms are also notable in the 2016 budget, the first from the Trudeau Liberals. A new top personal income tax bracket of 33% was created, while the rate on the second lowest bracket was reduced from 22% to 20.5%. The overall fiscal impact was modestly revenue positive.

Beyond changes to rates and brackets, other tax credits and deductions were brought in that reduce income taxes payable. This includes ongoing increases in Registered Pension Plan (RPP) and Registered Retirement Savings Plan (RRSP) contribution limits, and the introduction of the Tax Free Savings Account (TFSA) in 2008. Additionally, a number of boutique personal income tax credits were introduced between 2006 and 2015, most of which were eliminated in the 2016 budget. One particularly notable positive change to personal income taxation was the Trudeau government’s cap on the use of stock options as a form of corporate remuneration.

Some notable changes also occurred in the income transfer system, in particular improvements in child benefits. These changes culminated in the Canada Child Benefit, introduced in the 2016 budget. The benefit combined and bolstered previous child and child care benefits. A Working Income Tax Benefit was introduced in 2008, which boosts income for low-income workers (renamed the Canada Workers Benefit, this benefit has been modified several times since its inception). The Guaranteed Income Supplement (GIS) for seniors was enhanced in 2015.

A number of temporary measures during the COVID-19 pandemic boosted transfer income. These included federal programs, like the Canada Emergency Response Benefit (CERB), and provincial changes, such as an enhanced Climate Action Tax Credit in B.C. We chose our dates of analysis specifically to avoid these years (we looked at 2019 and 2022). We note that a key lesson from COVID-19 is that federal capacity to underpin incomes can be much stronger than we currently see.

Corporate tax cuts figure prominently during the first half of our timeframe, with the Conservative government of the day emphasizing international tax competitiveness. This included a reduction of the general corporate income tax (CIT) rate in a series of steps, from 21% in 2007 to 15% in 2012, as well as limitation of the capital tax in 2006 and elimination of the corporate surtax in 2008. Similarly, there have been ongoing reductions over many budgets in the small business tax rate, as well as favourable accelerated capital cost allowances and expansion of flow-through share tax credits.

At the provincial level, there have also been changes although their impact on tax incidence will be less noticeable in our national analysis. Ontario lowered the personal income tax rate for the bottom bracket in 2009 and increased taxes on high incomes between 2012 and 2014. The province also harmonized sales taxes with the GST in 2010. B.C. added a new top personal income tax bracket in 2018, with a marginal rate of 16.8%, and eliminated its regressive Medical Service Plan premiums in 2019 in favour of a payroll tax, the Employer Health Tax. Alberta had a flat income tax of 10% between 2001 and 2015, which was replaced by a progressive rate structure, with a top marginal tax rate of 15%.

On corporate taxes, Ontario reduced its CIT between 2009 and 2012, and also eliminated its capital tax. In B.C., the CIT rate was reduced in 2009 and 2011, then was raised in 2013 and 2018; as a result, the general CIT rate was one percentage point higher in 2022 than 2004. In Alberta the shift was in the opposite direction, with an increase in CIT rate in 2015 that was then lowered back to the previous rate by 2020. Similar to the federal government, small business tax rates were also reduced in several provinces.

Tax incidence results

Results in this section are presented for household income deciles, or groupings of 10% ranked from lowest income (D1) to highest (D10), with further break down of D10 into the top 1% (P99-100), next 4% (P95-99) and next 5% (P90-95). Rates below are stated as a share of broad income for each group.

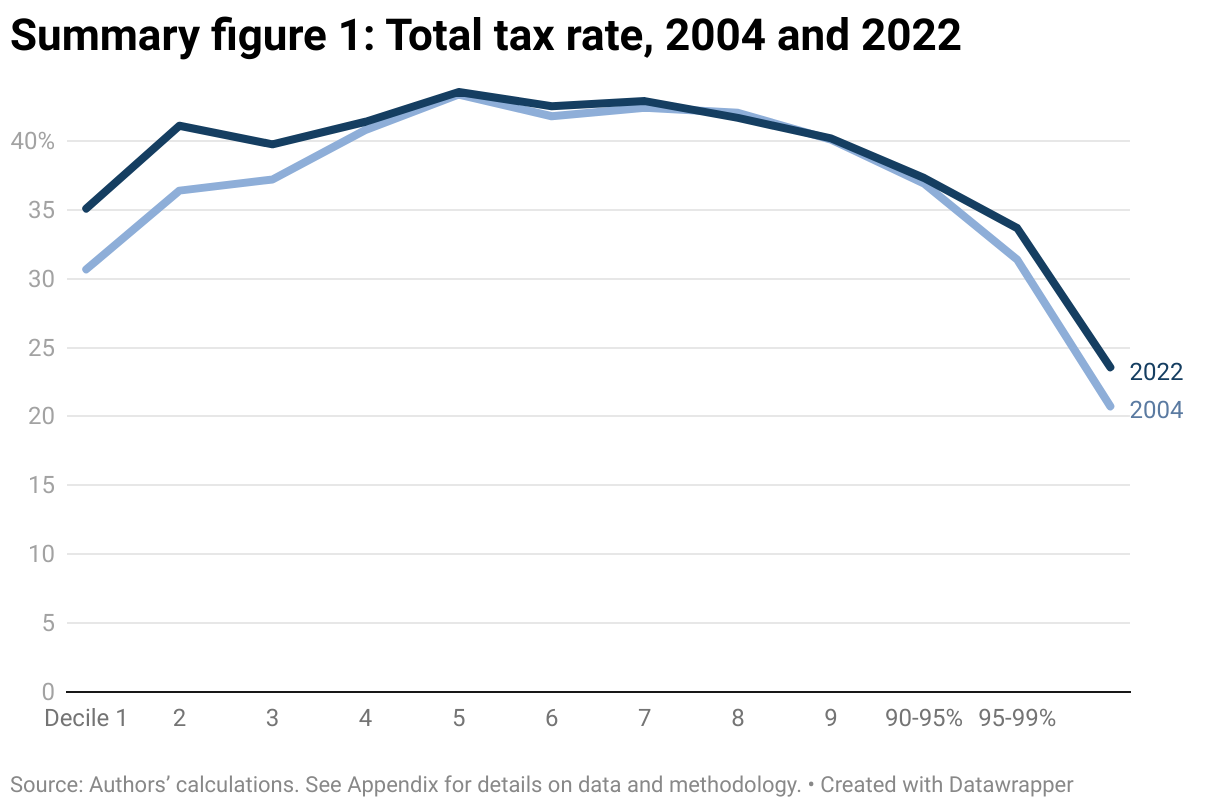

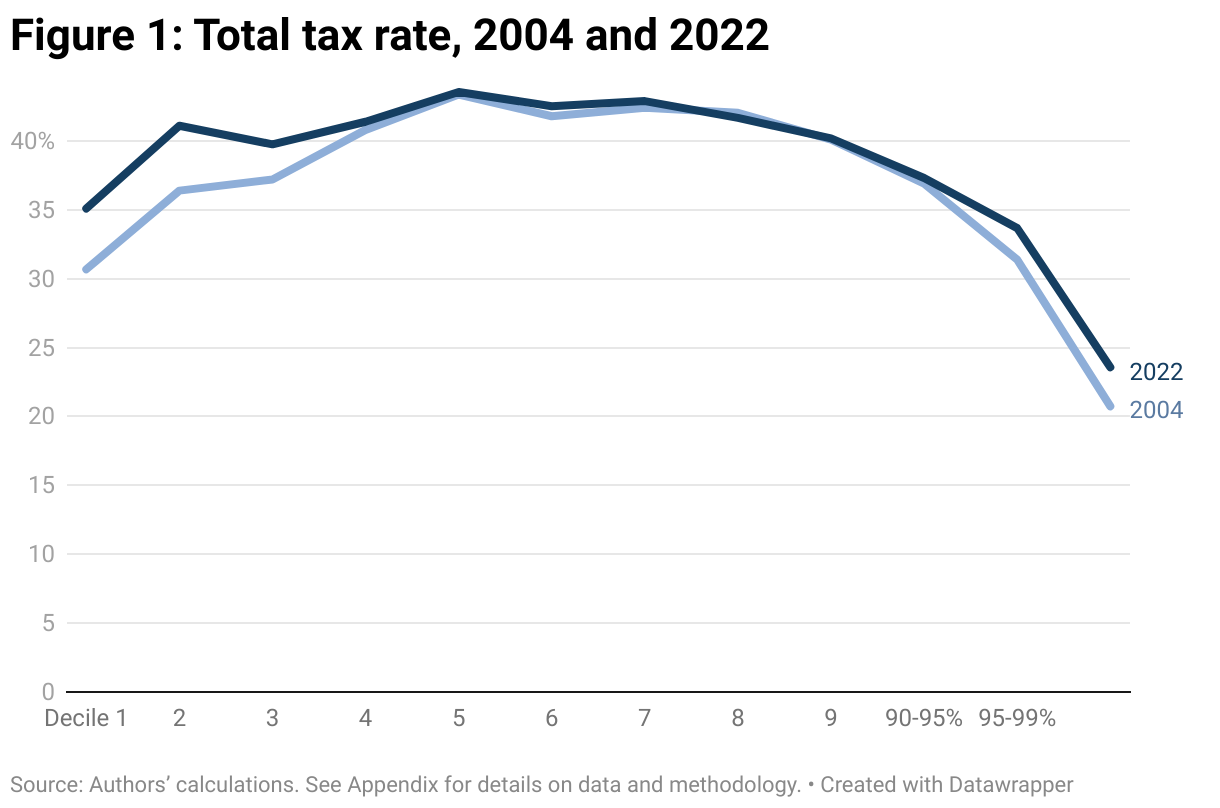

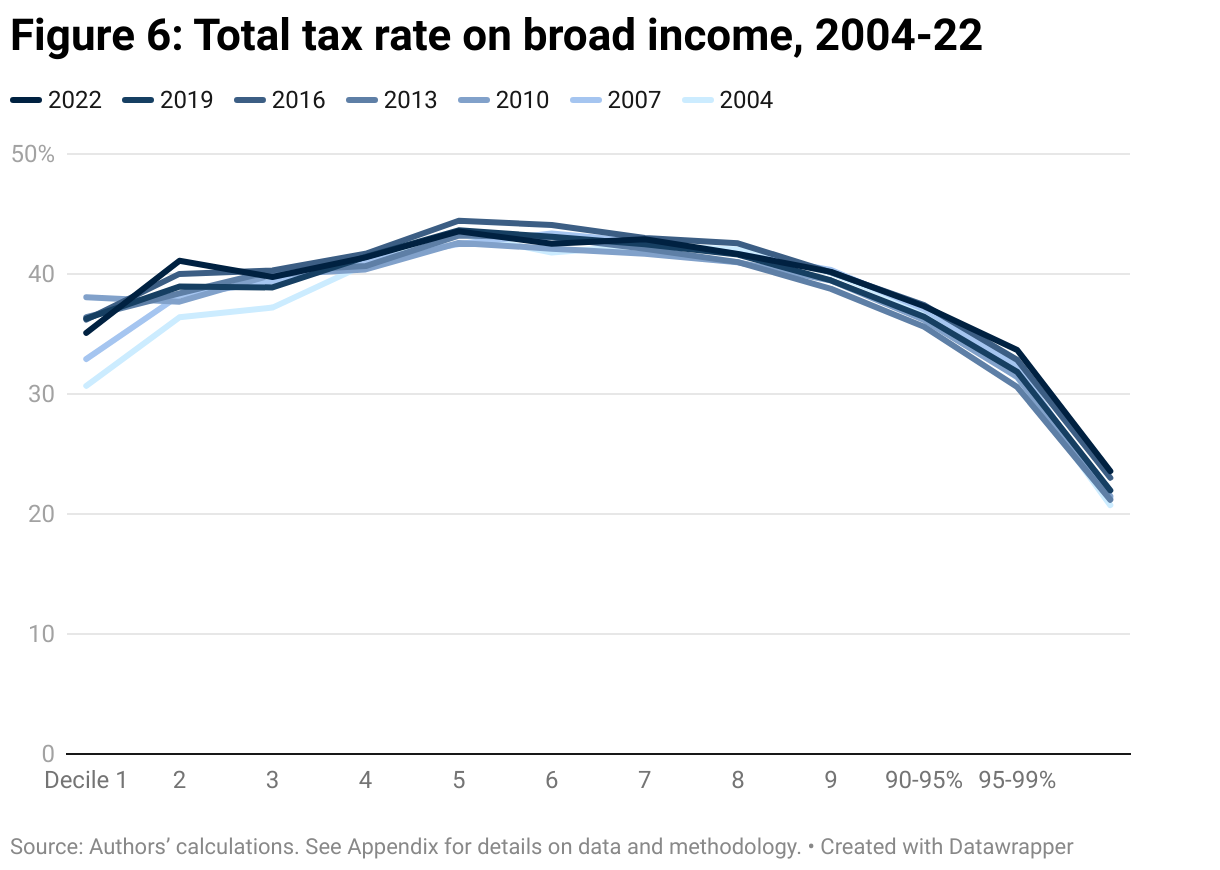

Figure 1 shows that the total tax rate is progressive up to the middle of the income distribution, then regressive thereafter. The average tax rate is little changed in 2022 (36.7%) compared to 2004 (36.0%), with the peak tax rates in the middle (D5) at 43.8% and 43.5% respectively. Additional figures, including all three-year increments between 2004 and 2022, are included in the Appendix but we leave them out of these figures to more clearly illustrate the change over time. Data are also presented in Table 1 at the end of this section.

Figure 2 shows the change in tax rate between 2004 and 2022. Relative to 2004, the 2022 distribution was much less progressive over the bottom deciles, with average tax rates in 2022 as much as 4.7 percentage points of income higher for the bottom two deciles. Rates for the top 1% were also up by 2.8 percentage points in 2022 relative to 2004. A closer look (see Appendix) shows that this appears to be a recent outcome of federal efforts to close some loopholes available to wealthy Canadians. Tax rates through the middle of the distribution were very similar in 2022 as in 2004.

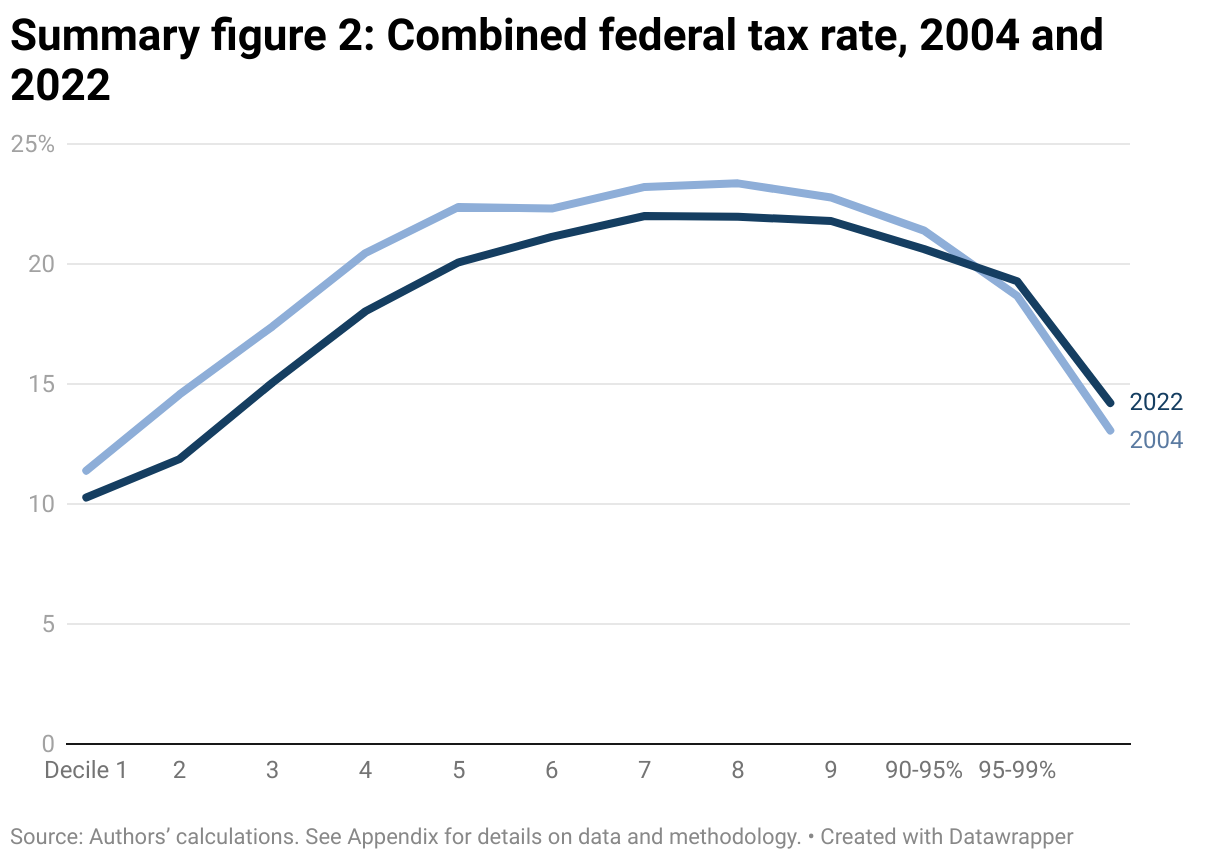

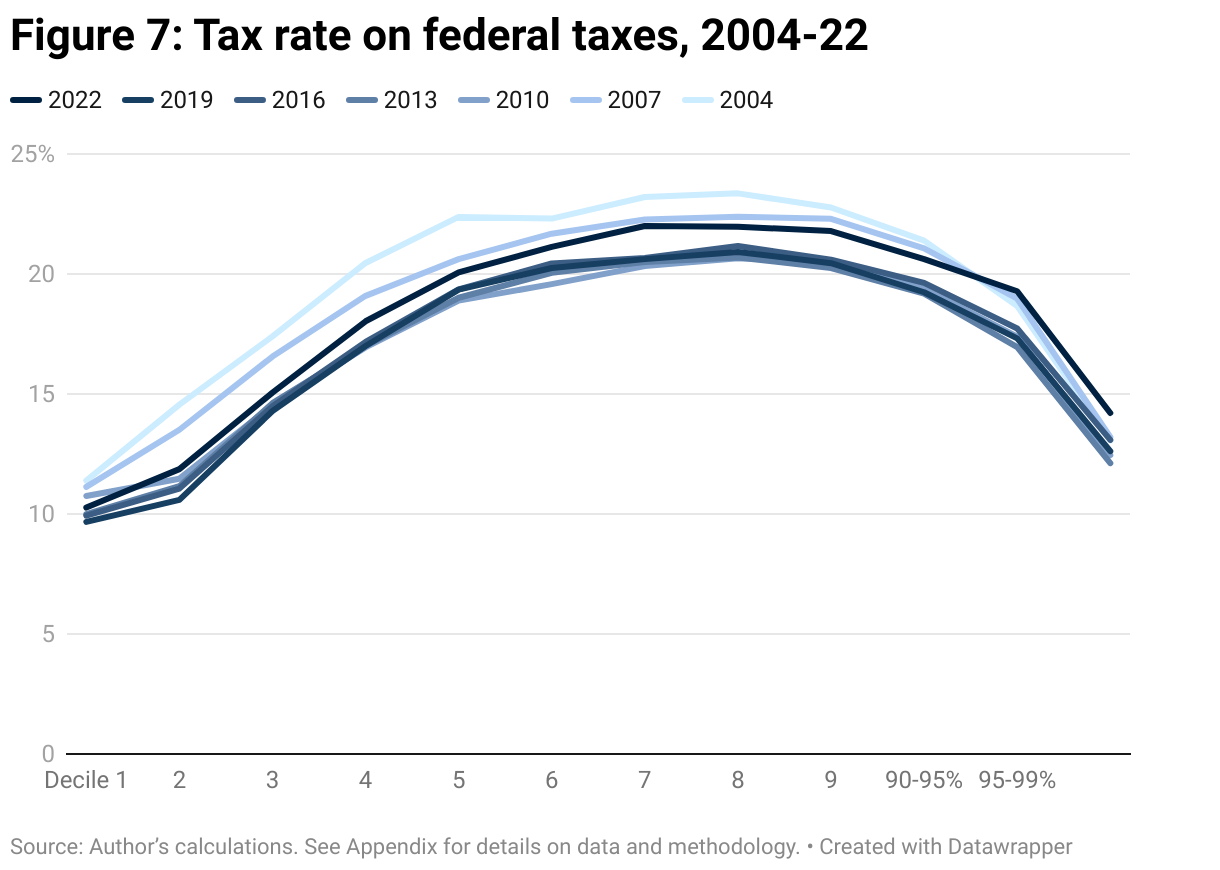

Figures 3 and 4 show all federal and all provincial taxes, respectively. There was an overall reduction in federal taxes between 2004 and 2022, reflecting reductions in the GST and federal income tax between 2005 and 2008. An exception is the very top of the distribution, reflecting the 2016 addition of a new top income tax bracket. The mix of federal taxes is progressive up to the D7, then it flattens out and becomes regressive at the top. This is largely due to the progressive nature of personal income taxes, combined with payroll taxes that are progressive up to a ceiling on contributions and regressive for the upper part of the distribution. Corporate income tax is also progressive, even with a flat rate structure, due to the fact that ownership is so highly concentrated in the upper part of the distribution.

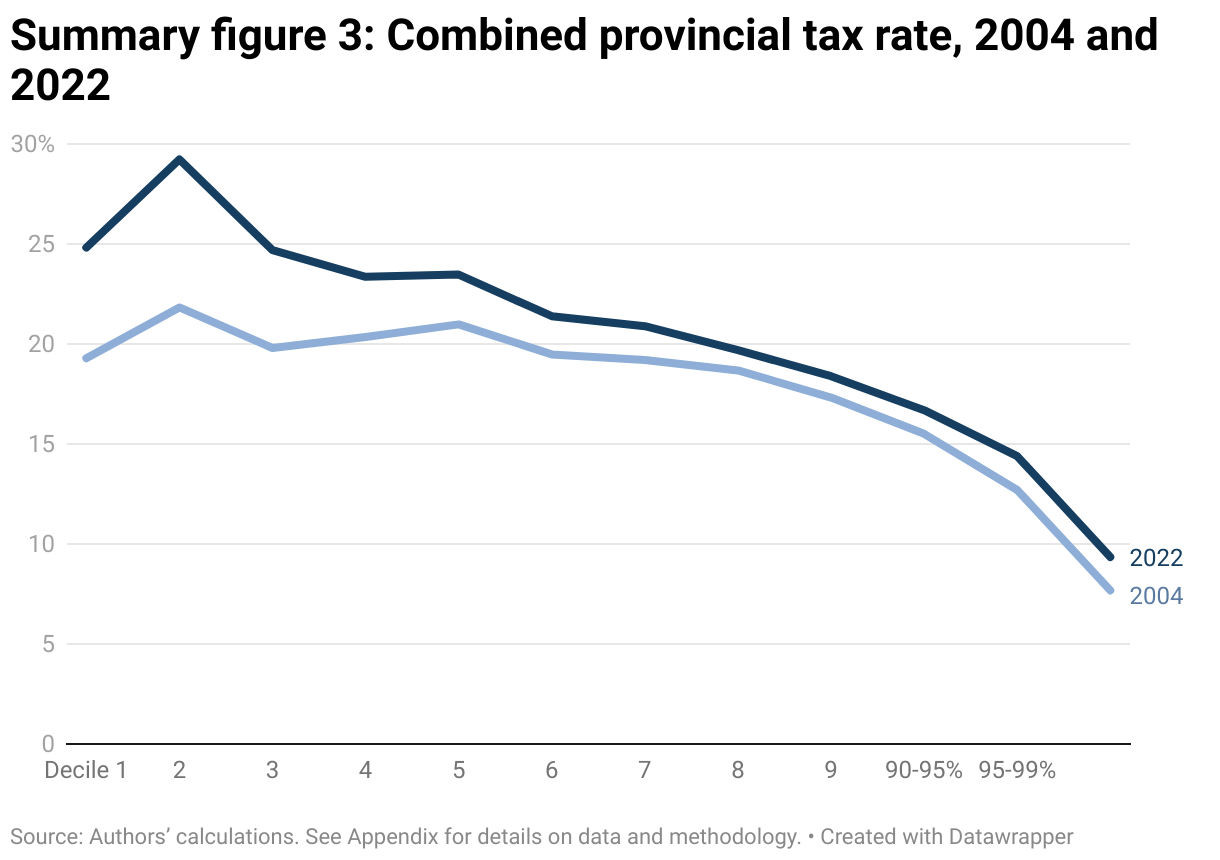

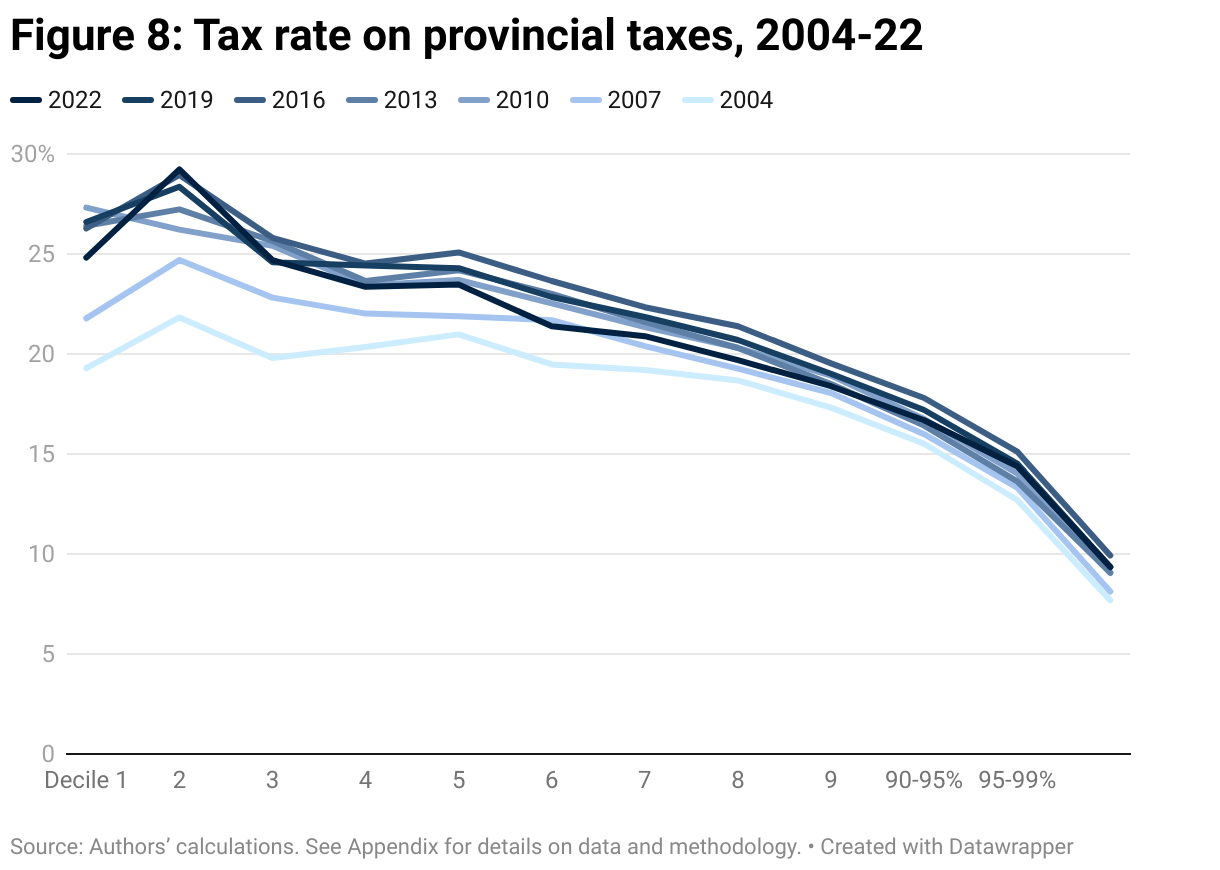

Reductions in federal taxes have been offset or more-than-offset by increased provincial taxes for all groups in 2022 relative to 2004. The distribution of provincial taxes is more clearly regressive across the whole distribution, with the exception of the jump from D1 to D2, which is likely due to the greater prevalence of income transfers vs. market income at the bottom of the distribution. The provincial distribution has also become more regressive at the bottom. In 2004, provincial tax rate was fairly flat up to D5 then regressive, but by 2022, it was clearly regressive. Thus, the increase in tax rates in the bottom of the distribution noted above is entirely the consequence of provincial tax changes and, if anything, the regressive shift is moderated somewhat by federal tax changes over that timeframe. Looking more closely, we find that provincial PIT rates increased for all groups from D3 upwards, likely reflecting the growth of incomes beyond inflation-adjusted increases to income tax brackets, as well as a large increase in the commodity tax rates at the bottom of the distribution. These changes merit further research at the provincial level.

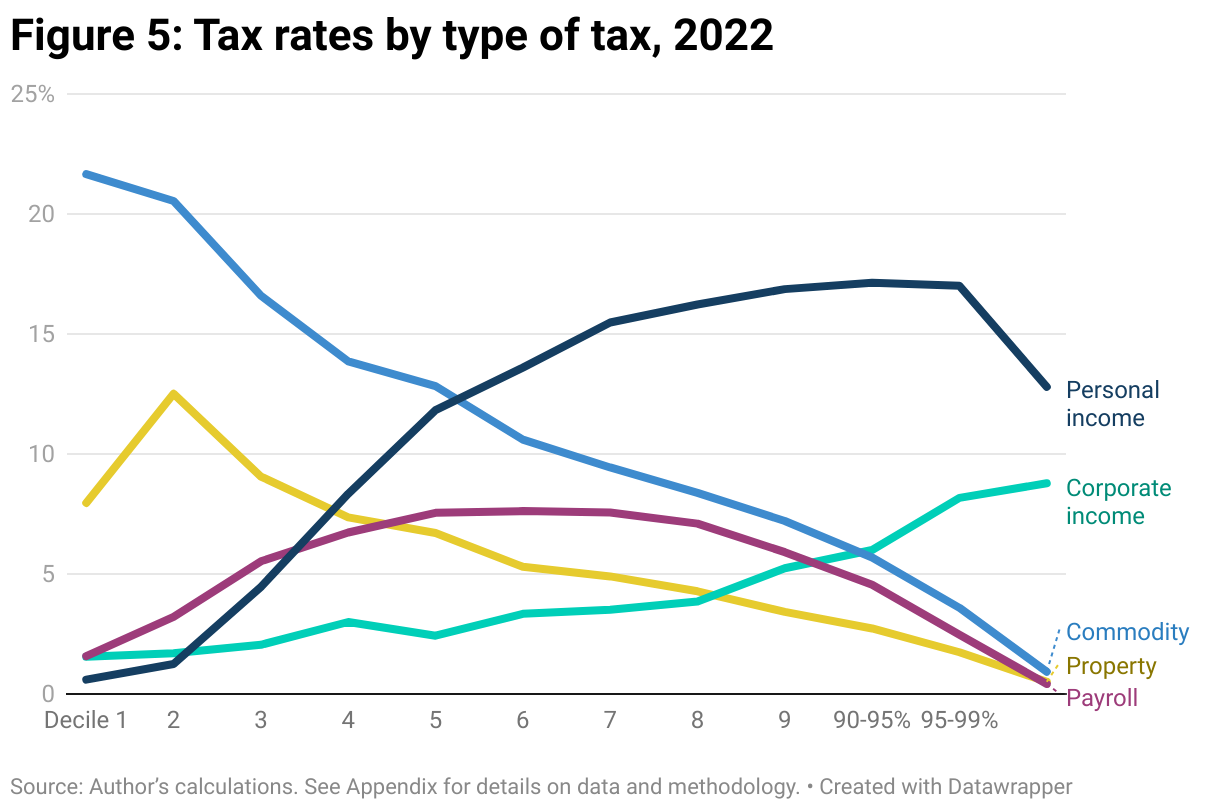

Figure 5 shows the incidence of different types of taxes: combined federal and provincial personal income taxes, corporate income taxes, commodity, payroll and property taxes. Personal income tax remains the most progressive part of the tax system due to brackets that increase marginal rates as income rises. However, untaxed income predominates at the very top of the distribution, with no taxes payable on inheritances and gifts, employer-provided benefits, only half of taxes payable on realized capital gains, and no capital gains tax whatsoever on sales of principal residences.

Corporate taxes are also progressive since they are paid by equity owners (in this case, allocated by the incidence of dividends). Commodity taxes are regressive, but credits/benefits, such as the GST credit at the federal level or B.C.’s Climate Action Tax Credit at the provincial level, are important to reduce the actual regressive impact of commodity taxes, including carbon taxes. In between are payroll taxes, which are progressive up to the ceiling on contributions, then regressive as income rises above the ceiling.

Implications for tax reform

Canada is a land of both abject poverty and spectacular wealth. Our broken social contract is in need of renegotiation. A fair and decent society should have neither extreme of obscenely rich nor desperately poor. Taxation of the wealthiest is a central means by which we can reduce inequality, provide adequate shared public infrastructure and services that benefit all, and create opportunities for all to live a decent life. More progressive taxation will also support our efforts to cut emissions since the wealthiest Canadians not only have much larger carbon footprints, their emissions have increased while those for the majority have fallen.5

A fair tax system should be based on a broad or comprehensive income concept that reflects the individual’s actual command over resources. This is also known as “horizontal equity”: the principle that two people with the same amount of income in a given year pay the same rate of tax regardless of the source of that income. Bay Street accountant Kenneth Carter, who headed a royal commission on taxation in the late 1960s, captured this notion with his comment that “a buck is a buck.” In addition, “vertical equity” is the principle that those with greater ability to pay should pay a greater share of their income in tax. In the words of the Carter Commission (the Royal Commission on Taxation), taxes should be allocated according to “economic power.” A fair tax system should thus be progressive and broad in its consideration of taxable income.

Our study highlights the role of non-taxed and lightly taxed sources of income, capital gains in particular, for regressivity at the top of the income distribution. Realized capital gains represent real dollars in sellers’ pockets and should be fully included in the income tax base. Whether for real estate or financial assets, lightly taxing gains on these (often speculative) holdings is not good policy. The federal government moved modestly to change direction with a 2023 change to fully tax capital gains on housing sold in a period of less than one year, and B.C. is planning a new flipping tax on gains made under one year (phasing out by end of year two after a purchase).

Reform tax expenditures

Canada’s income tax system contains a large number of deductions and tax credits (both refundable and non-refundable), known collectively as “tax expenditures.” Rather than actual expenditures funded by taxes, these represent forgone tax revenue and lower effective tax rates. Some tax expenditures seek to achieve a public policy objective, such as increased saving for retirement, investment in research and development, investment in economic activities (such as exploration and mining), support for charitable activities, and specific personal circumstances. Whether or not these measures are desirable and effective in achieving their objectives, they have distributional impacts by affecting the taxes paid by different groups, and reduce tax revenues that could be used for public services and income supports. A large number of current deductions and credits disproportionately benefit high earners.

A report by David Macdonald found that the five most regressive or inequitable tax expenditures were: pension income splitting, employee stock options deduction, the dividend gross-up and tax credit, the foreign tax credit, and, partial inclusion of capital gains. In contrast, Macdonald also cited five progressive tax expenditures: the working income tax benefit, non-taxation of Guaranteed Income Supplement and spousal allowance benefits, the refundable medical expenses supplement, non-taxation of social assistance benefits, and the disability tax credit. In other words, not all tax expenditures are the same in terms of distributional impact.6

Finance Canada provides estimates of the value of tax expenditures in the federal income tax system in their annual Tax Expenditures reports.7 Key deductions, exemptions and tax credits that primarily benefit the wealthiest should be phased out. A more comprehensive review of these tax expenditures is needed. Even the tax expenditure for charitable donations, at more than $3 billion per year, ultimately allows wealthy individuals to determine what type of charitable endeavors will be undertaken by society.

Increase the progressivity of the income tax system

In Canada, the top income tax brackets greatly improve tax fairness while also tackling income inequality. While there have been some modest increases in the top marginal income tax rate federally and provincially, the income tax system could do a much better job at mitigating market-driven increases in inequality and the concentration of income and wealth at the very top.

Top marginal tax rates in Canada exceeded 70% for a quarter-century after the Second World War and only fell to about 50% since 1982. While many arguments were made in favour of lowering top rates to boost economic performance, it is notable that Canada’s growth of productivity and GDP per capita were substantially higher during the post-war period than after 1982. A number of scholars have estimated revenue-maximizing top marginal rates ranging from 65% to 90%.8

In addition, brackets below the top marginal rate could also be raised, as this would also increase the progressivity of the tax system and the total amounts paid by top earners. This is not even necessarily about raising revenues—which is an important consideration—but ameliorating toxic inequality that is having adverse impacts for the bottom 80% of households.

The 2024 federal budget also introduced a new top rate for capital gains inclusion of 66% for gains above $250,000 per year. This is a modest but important step towards a more progressive tax system at the top of the distribution.

Tax inheritances and wealth

To ensure that all Canadians contribute their fair share in taxes, large inheritances and gifts should be included in the recipient’s taxable income. Tax law professor Neil Brooks proposed a cut-off of $3 million for inclusion of inheritances and gifts in taxable income, as well as an annual wealth tax of 1%.9 There is room for debate on where to draw the threshold, but the key point is that taxing bequests is essential for fairness and equality of opportunity. Alex Hemingway calculates that a Canadian wealth tax applying to net wealth above a $10 million threshold with three brackets and rates (one per cent for net wealth above $10 million, 2% above $50 million and 3% above $100 million) would raise an estimated $32 billion in the first year alone, rising to an estimated $51 billion by the tenth year.10

Taxing holdings of wealth at an annual rate would improve tax fairness because wealth is much more unequally distributed than income. Provincial property taxes are, in essence, a wealth tax on real estate, the principal form of asset ownership for a large share of the population (B.C. has both a property tax and a property transfer tax). A federal tax on wealth would simply broaden the base to include financial market assets, ownership of which is highly concentrated at the top of the income ladder. Indeed, a private version of a wealth tax already exists in the form of annual fees for many whose financial wealth is held in mutual funds.

Raise corporate income taxes and bring in a windfall profits tax

Corporations are legal vehicles through which individuals pool their capital to accumulate wealth. Corporations benefit from limited liability laws, from public infrastructure investments and public spending on education, health care and so forth, so it is appropriate that corporations also pay income taxes.

Corporate income taxes ensure that all income gets taxed and reduces the incentive for individuals to shelter income from tax by keeping it within a corporation. At some point, however, income and capital gains must revert back to an individual (during one’s lifetime or upon death), at which point they would be subject to the personal income tax system.

In addition, recent years have delivered windfalls to certain corporations and sectors due to commodity prices determined outside of Canada (mega-profits going to oil and gas companies in 2021 and 2022, for example) or due to use of market power to increase prices (supermarket chains, most notably).11 A one-time windfall profits tax was brought in federally for the banking and life insurance sectors for the 2021 tax year. Ongoing windfall taxes can guard against excessive profiteering and make the CIT more progressive overall.

Conclusion

In its current state, the Canadian tax system has become more regressive since 2004. A return to more progressive taxation would improve fairness, while also providing a lever to directly reduce income and wealth inequality. Despite the progressive personal income tax system, when we look at all taxes and income, the tax system is only moderately progressive at the bottom, flat through the middle and regressive at the top.

A comprehensive tax review in the United Kingdom concluded that a good tax system must be both progressive and neutral. This is to say that it “can raise the revenue that government needs to achieve its spending and distributional ambitions whilst minimizing economic and administrative inefficiency, keeping the system as simple and transparent as possible, and avoiding arbitrary tax differentiation across people and forms of economic activity.”12 These principles of a good tax system are not new nor controversial; they have been articulated by other major tax reviews in the past, though there is still an active debate in the economics and law literature over how to best operationalize them through public policy.

A good tax system must be progressive for reasons of fairness and justice, but also on economic grounds.13 The marginal utility of money declines as income rises—that is, the perceived and actual benefit derived from an extra dollar of income is much higher for low-income households than higher-income households. It follows that social welfare is improved when resources are more equally distributed—at least up to the point where incentives to work and invest in productive activities get severely distorted.

To the extent that money can buy opportunities, particularly for young children, progressive taxation serves to redistribute opportunities and improve social mobility. Thomas Piketty recommends, for example, wealth and inheritance taxation to fund capital grants that would go to each young person in society in order to break down wealth inequalities and to keep wealth and capital circulating for a dynamic economy.14

Progressive taxation is particularly important in the presence of high levels of market income inequality and concentration of wealth at the very top of the income distribution, as we are increasingly seeing in Canada. There is good reason to believe that in reducing inequality at the top and bottom of the distribution through more progressive taxation, we can have a stronger economy that is efficient, sustainable and fair.

Appendix

Data and methods

This paper follows the method of Marc Lee’s 2007 Eroding Tax Fairness (ETF) paper, which itself followed the approach taken in an influential 1994 article in the Canadian Tax Journal, “Tax Incidence in Canada,” by Vermaeten, Gillespie and Vermaeten (VGV).15

We include all sources of income and all taxes, then distribute these across deciles (groupings equally comprised of 10% of households, ranked from lowest to highest income). The top decile often conceals the extreme inequality at the top of the distribution, so we break the top 10% into the top 1%, the next 4%, and the next 5%.16 Some anomalies can emerge in the bottom decile because this can include ostensibly wealthier households reporting large capital losses and closing the year with low income. We adjust for this, to some extent, by only including households with reported income greater than zero.

Estimates are made for each of the following years: 2004, 2007, 2010, 2013, 2016, 2019 and 2022. By using these three-year intervals, we can clearly see the trends. Since comparisons over time can be affected by choice of start and end years, we believe our choice allows the analysis to avert false patterns emerging from the 2008-10 financial crisis and recession, as well as the 2020-21 COVID-19 pandemic shutdowns.

To derive our distributions by income group of taxes and income sources, we start with aggregates from the Canadian System of Macroeconomic Accounts (CSMA), Canadian Income Survey (CIS), Survey of Financial Security (SFS), and Fiscal Reference Tables. These are then allocated to deciles and centiles as determined by Statistics Canada’s Social Planning Simulation Database and Model (SPSD/M), which is widely used for distributional analysis of government policy changes. Statistics Canada summarizes the SPSD/M as such:

The SPSD is a non-confidential, statistically representative database of individuals in their family context, with enough information on each individual to compute taxes paid to and cash transfers received from government. The SPSM is a static accounting model which processes each individual and family on the SPSD, calculates taxes and transfers using legislated or proposed programs and algorithms, and reports on the results.

On the income side, we begin with CSMA data, which includes: wages, salaries and commissions, investment income, self-employment income, corporate pre-tax profits (net operating surplus), and other income.17 We then add: employer-provided benefits (mostly supplemental health and dental plans but also vehicles and other perks), realized capital gains, and inheritances and bequests.

We also add estimates for commodity and property taxes shifted to workers. The latter category is estimated based on the idea that companies do not pay the full amount of taxes levied on them because they can pass some of the tax along to consumers as higher prices and to workers as lower wages. In the absence of those taxes, workers’ wages would be higher, and thus we add back amounts, following assumptions made in VGV.

These additions and adjustments to net domestic income yield what is known as pre-fisc income. To form broad income, we add government income transfers, including: federal transfers for old age and children’s benefits, plus Employment Insurance benefits and Canada/Quebec Pension Plan benefits, and provincial transfers for social assistance.

One source of income in the CSMA that we do not count, and that has received more attention in recent years, is imputed rental income, which is the non-cash income of homeowners living in their own home, estimated as its equivalent rental value. Because this is non-cash income and its estimated value is a function of activity in real estate and rental housing markets, we do not include it, although it clearly represents in-kind command over resources.

Our aggregate for realized capital gains comes from SPSD/M. For inheritances and bequests, we assume, following VGV and ETF, that 1.2 per cent of net worth turns over each year in the form of inheritances and bequests. Net worth data are from the SFS.

In most cases, we allocate the CIS or CSMA aggregate based on the same concept in the SPSD/M. In cases where there was no corresponding variable available in the SPSD/M, we use proxies in the SPSD/M to allocate the aggregate amounts. For example, corporate pre-tax profits and corporate taxes are allocated based on the distributional series of dividend income. Self-employment income and inheritances and bequests are both allocated based on the distribution of capital gains. Employer-provided benefits and shifted commodity and property taxes are allocated back to households based on the distribution of EI premiums.

The allocation of corporate pre-tax profits and corporate income tax is in line with dividends in SPSD/M and implicitly assumes that corporate taxes are borne by the owners of capital. A standard theoretical proposition in the literature is that corporate owners pay corporate taxes only up to the “world rate” then shift the remainder to consumers or employees. In the VGV analysis of the 1988 tax system, they consider the U.S. rate to be the effective world rate and note that since Canadian and U.S. rates are very similar, the full incidence is borne by corporate owners. The same assumption was made in ETF and in this paper. As noted in ETF: “it is questionable whether the ‘world rate’ hypothesis actually holds in the real world. Furthermore, the hypothesis is based on highly mobile international capital, whereas in many sectors capital is less than fully mobile (non-tradables, resources) and the international mobile capital may represent a small share of Canadian industry.”

Our allocations from the SPSD/M are adjusted for family size to compensate for economies of scale when spending the income received; two can live more cheaply per person than one and four can live more cheaply per person than two. We use the standard division by the square root of family size approach, which makes equivalent, for example, a single individual making $100,000 with a family of four making $200,000.

Differences between ETF and current modeling

The current paper follows the methodology of ETF and VGV. Due to discrepancies in the aggregates produced by SPSD/M and officially published statistics, ETF used the latter and then allocated values back to deciles and centiles based on SPSD/M distributions.

However, there are some differences that emerge from updates to the SPSD/M model, changes to the CSMA and CIS, and a shift to using households in the current study, whereas ETF was based on economic families. Using households allowed us to derive allocations for local property tax in SPSD/M.

As defined by Statistics Canada: “Economic family refers to a group of two or more persons who live in the same dwelling and are related to each other by blood, marriage, common-law union, adoption or a foster relationship.”18 Whereas, “Household refers to a person or group of persons who occupy the same dwelling…either a collective dwelling or a private dwelling. The household may consist of a family group such as a census family, of two or more families sharing a dwelling, of a group of unrelated persons or of a person living alone.”19 In some cases, one household could comprise more than one economic family, although these are a fairly small share of the total number of households.

Comparing the allocations in ETF for 2005 and the current paper for 2004, there are some important differences in investment income, dividend income and capital gains arising from better modelling in the SPSD/M. These show lower shares of these income sources in the middle of the distribution and higher shares in the top two deciles. In the opposite direction is property tax, which shows in the current modelling much less tax paid in the top decile alongside higher average rates through the remainder of the distribution. The SPSD/M in 2023 is much upgraded and has greater functionality than the version used for ETF.

A key difference is that income aggregates changed, leading to some differences in estimations in the current paper: $688 billion for wages, salaries and supplementary labour income in ETF for 2005 vs. $554 billion for wages, salaries and commissions in 2004 for the current paper. Some of the gap is annual growth, but the former is also higher due to the inclusion of employers’ social contributions (based on the current CSMA series). The different sources:

- ETF was based on data now archived as Gross domestic product (GDP), income-based, provincial economic accounts, annual, 1981-2010 (×1,000,000), Table: 36-10-0311-01 (formerly CANSIM 384-0001).

- This paper primarily draws from the Canadian Income Survey (CIS), Income statistics by economic family type and income source (×1,000,000), Table: 11-10-0191-01 (formerly CANSIM 206-0021). These data go to 2021 and are in 2021 dollars. We convert them to current dollars using the CPI for Canada, all items, Consumer Price Index, annual average, not seasonally adjusted, Table: 18-10-0005-01 (formerly CANSIM 326-0021).

- These are supplemented by data from System of National Accounts, Gross Domestic Product, income-based, provincial and territorial, annual (×1,000,000), Table: 36-10-0221-01 (formerly CANSIM 384-0037). This series includes corporate profits (we use the SNA’s net operating surplus here). The CIS data only go to 2021, so 2022 SNA quarterly data are used to estimate growth for the CIS income categories for 2022.

Tax data for both papers are drawn from the same source, the Fiscal Reference Tables, published by the federal Department of Finance. The federal carbon price is counted as revenue in the Fiscal Reference Tables but the Climate Action Incentive (aka carbon price refund) is not counted as an income transfer, so CAI has been added to our figure for income transfers (vetted against the federal government Annual Financial Reports).

The 2004 distribution estimated in this paper lines up well with the ETF 2005 numbers but tax rates top out at a higher percentage through the middle. The main difference is driven by a much higher aggregate for wages, salaries and commissions in the ETF dataset. The use of households rather than economic families may also be a factor. Differences in data sources and methods limit the comparability but we have confidence in the updated data in the CSMA and SPSD/M. The main point is that the same assumptions have been made from 2004 to 2022, to be able to see the direction of changes over time.

This publication was produced in cooperation with Canadians for Tax Fairness.

Notes

- https://policyalternatives.ca/publications/reports/eroding-tax-fairness

- See https://www12.statcan.gc.ca/census-recensement/2021/ref/dict/app/index-eng.cfm?ID=a2_4

- 2023 edition, https://www.canada.ca/en/department-finance/services/publications/fiscal-reference-tables/2023.html

- Terminology can be confusing here. The GST credit is not a credit against income tax owing or GST paid. It is an example of a tax benefit, an income transfer to low- to modest-income households based on the previous year’s taxable income.

- DT. Cochrane and K. Miller, October 16, 2023, “Taxes and the Path to a Green Economy”, Canadians for Tax Fairness, https://www.taxfairness.ca/en/taxes-and-climate

- D. Macdonald, November 2016, Out of the Shadows: Shining a light on Canada’s unequal distribution of federal tax expenditures, CCPA, https://policyalternatives.ca/sites/default/files/uploads/publications/National%20Office/2016/11/Out_of_the_Shadows.pdf

- https://www.canada.ca/content/dam/fin/publications/taxexp-depfisc/2023/taxexp-depfisc-23-eng.pdf

- L. Osberg, October 2015, How Much Income Tax Could Canada’s Top 1% Pay?, Canadian Centre for Policy Alternatives, https://policyalternatives.ca/sites/default/files/uploads/publications/National%20Office/2015/10/How_Much_Tax_Could_Canadas_Top_1_Pay.pdf

- N. Brooks, March 3, 2007, “A Democratic Tax Reform for Canada”, Canadian Dimension, https://canadiandimension.com/articles/view/a-democratic-tax-reform-for-canada

- A. Hemingway, May 9, 2023, “Why Canada still needs a wealth tax—and what it could fund,” Policy Note, https://www.policynote.ca/wealth-tax-2/

- DT. Cochrane, April 6, 2022, The Rise of Corporate Profits in the Time of Covid, Canadians for Tax Fairness, https://www.taxfairness.ca/en/resources/reports/report-rise-corporate-profits-time-covid; J. Stanford, February 27, 2024, “Canadian Corporate Profits Remain Elevated Despite Economic Slowdown”, Centre for Future Work, https://centreforfuturework.ca/2024/02/27/canadian-corporate-profits-remain-elevated-despite-economic-slowdown/

- J. Mirrlees, A. Stuart, T. Besley, R. Blundell, S. Bond, R. Chote, M. Gammie, P. Johnson, G. Myles and J. Poterba, 2011, Tax by Design, Oxford: Oxford University Press, pp 471-2, http://www.ifs.org.uk/mirrleesreview/. This finding is consistent with other comprehensive tax reviews by Meade Report on Taxation in the UK (1978) and the Carter Royal Commission in Canada (1969).

- This is the conclusion of the state-of-the-art economic analysis by American economists Peter Diamond and Emmanual Saez in the Journal of Economic Perspectives, and a key recommendation of the Mirrlees review in the UK, which is the most comprehensive tax review undertaken in the developed world in the last decade. P. Diamond and E. Saez, 2011, “The Case for Progressive Tax: From Basic Research to Policy Recommendations,” Journal of Economic Perspectives, vol 25 (4), p. 165-190.

- T. Piketty, 2020, Capital and Ideology, Belknap and Harvard University Press.

- V., Frank, I. Gillespie and A. Vermaeten, 1994, “Tax Incidence in Canada” in Canadian Tax Journal, vol. 42, no. 2, 348-416.

- Also called P99-100, P95-99 and P90-95, respectively.

- Defined as “Regular cash income from market sources that are not included in any of the other market income sources during the reference period. For example, severance pay and retirement allowances, alimony or child support received, periodic support from other persons not in the household, any income from abroad that is not investment income, scholarships, bursaries, fellowships and study grants, and artists’ project grants are included.” https://www12.statcan.gc.ca/census-recensement/2021/ref/dict/app/index-eng.cfm?ID=a2_4

- https://www23.statcan.gc.ca/imdb/p3Var.pl?Function=Unit&Id=33863

- https://www23.statcan.gc.ca/imdb/p3Var.pl?Function=Unit&Id=96113