Summary by the numbers

- New data shows that the federal government only disbursed 34 per cent of the Canada Housing Benefit (CHB) money—and only reached 40 per cent of eligible people

- The housing benefit ended March 31, 2023—with no possibility to boost those low take-up rates

- The Canada Dental Benefit has only disbursed 44 per cent of the money it was supposed to by March 29, 2023 (although the program runs to the end of 2023)

- The one-time GST credit likely had close to a 100 per cent take-up rate, but wasn’t as specific as the other programs

- These one-time cash transfers are the 2.0 version of a benefit distribution model that the federal government pioneered during the pandemic. As they evolve, we need to improve them or atrocious take-up rates will be the norm.

- Solutions include: attempt to automatically transfer cash where possible, targeted email campaigns to those likely eligible, better outreach to community groups who may drive up take-up rates.

Our content is fiercely open source and we never paywall our website. The support of our community makes this possible.

Make a donation of $35 or more and receive The Monitor magazine for one full year and a donation receipt for the full amount of your gift.

Policy Innovation

The pandemic led to substantial policy innovation, using federal cash transfers directly to Canadians.

The CERB, a completely novel attestation-based cash transfer, was one prominent example—but the feds also sent one-time transfers to almost everyone who was already receiving other pre-existing federal cash transfers, like the GST credit.

The government used to send cheques directly to households, then it incorporated those benefits into the tax filing process. Now it is experimenting with using existing administrative tax data to provide direct one-time cash transfers much faster, although leaving the regular cash transfers baked into the tax system untouched.

In the fall of 2022, the federal government reused these novel strategies three times—for the fall GST credit top up, the Canada Housing Benefit top up (CHB), and the Canada Dental Benefit. Statistics are now available for these programs, so we can evaluate how they did.

The GST top up was automatic. The Canada Revenue Agency simply sent everyone receiving the GST credit an additional amount.

The other two—the CHB and the dental benefit—were application-based. Applicants had to go to the Canada Revenue Agency (CRA) website, check some boxes and maybe upload some documents.

The feds used a “trust, but verify” approach. If the CRA approved the applicant, they would immediately receive the benefit in their bank account, similar to the CERB. The CHB was $500 for low-income renters who spend more than 30 per cent of their income on rent. The dental benefit was up to $650 per child under age 12 for families making under $90,000 who have incurred dental costs and don’t have insurance.

The results are in: it was mostly a failure

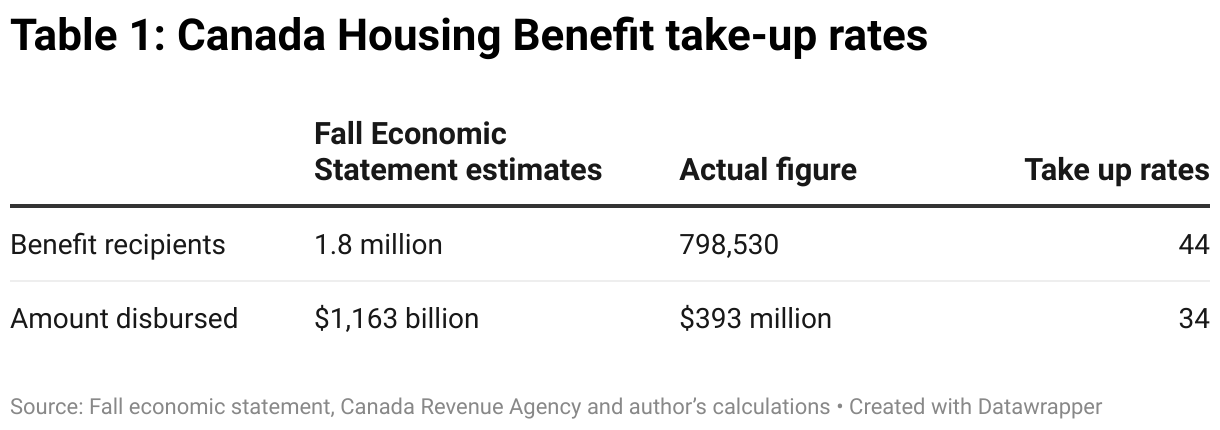

The housing benefit ended on March 31, 2023, so we now have its final details (see Table 1 below).

One key takeaway: the take-up rates were atrocious.

The federal government had only disbursed a third of the projected total when the program closed down. That money only reached 44 per cent of the people who were likely to be eligible for it.

That might be a generous interpretation. When the budget estimates were calculated, they wouldn’t have assumed a 100 per cent take-up rate on an application-based program in the first place. They would have assumed a more limited take-up rate and put that in the fall economic statement as the budget estimate, which is what would be in Tables 1 and 2.

And to add an obvious point: all of these benefits depend on people filing their taxes in the first place. If they don’t file, they can’t receive any of the cash transfers. Up to 12 per cent of Canadians currently don’t file their taxes,so they can’t get any of these transfers. A proper take-up rate would include those Canadians as well, which Tables 1 and 2 don’t.

This was entirely predictable and could have been headed off much sooner. The housing benefit was confusing from the start. The feds imposed onerous requirements, far from pure attestation—as had been the case for the CERB. These conditions are likely as much to blame for low take-up rates as the approach in general.

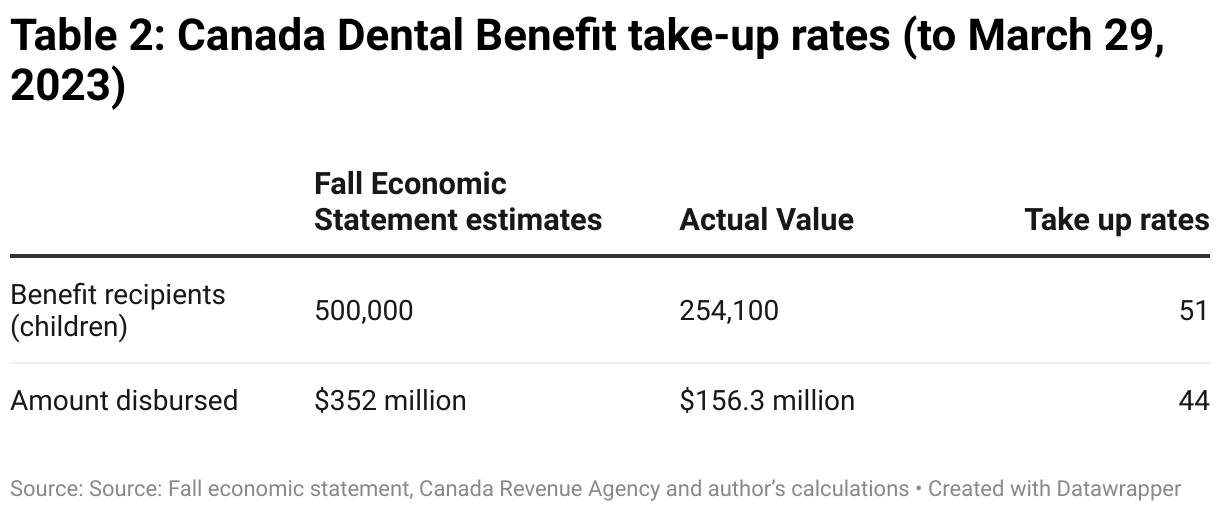

The dental benefit has two application periods. In each period, a family can apply for $650 per child under 12. The first period runs from October 2022 to June 30, 2023 and the second period winds up at the end of 2023.

The federal government has released the data on the program until March 29, 2023 and its fall economic statement estimates cost until March 31, 2023 (the end of the 2022-23 fiscal year). So the end of March 2023 is a logical point at which to evaluate the program, particularly on the amounts disbursed.

The take-up rates for the dental benefit were slightly better than the housing benefit. The CRA only disbursed 44 per cent of what the federal government expected to pay out by the end of March. If more people apply than the CRA expects before the end of 2023, then that number could rise, but this initial checkpoint does not bode well.

Unfortunately, the timeframes don’t properly match for the dental benefit in terms of children helped. The fall economic statement provided an estimate of child beneficiaries for all of 2023, while the stats so far only go to March 29, 2023. The dental benefit has, so far, helped 50.8 per cent of its overall estimate of 500,000 children. There are nine more months to go on the program, but many of the children who will receive it in the second half of 2023 will be the same ones who received it in the first half. This will increase the value they received but won’t drive up the count of beneficiaries.

The federal government is accepting applications for the dental benefit for the rest of 2023. This means that changes in advertising or program design could make a difference in take-up rates—unlike the now-gone housing benefit.

For the GST top-up, anyone who was already receiving the GST tax credit would have also received this fall top-up, which was worth the value of two quarterly payments in a single one-time payment. Other than some low-income Canadians who don’t file income taxes, close to every single person who was eligible to get the credit likely got it.

The GST top-up wasn’t application-based—cash just automatically appeared in eligible Canadians’ bank accounts. With a few possible minor exceptions—people who changed banks or moved at the wrong time, for example—it was as close to full take-up as possible.

Is there a best approach for one-time transfers?

One might conclude that the GST top-up is the best approach, since its take-up rate will always be basically 100 per cent. But there are downsides. For example, governments can’t specify other criteria, such as creating a benefit specifically for low-income Canadians who are tenants rather than homeowners.

If governments want to include these sorts of additional criteria, that’s where the complication comes in—which can easily result in atrocious take-up rates, as was the case for the housing benefit. The feds ran media ad campaigns for both the housing and dental benefits and they advertised them prominently on government websites—particularly on the CRA “my account” website, which Canadians will be visiting often due to tax season.

Clearly, that wasn’t enough.

The CERB—the flagship of the new cash transfer programs—was, of course, widely used by its target demographic. But it wasn’t the only experiment of its kind in the early days of the pandemic. The Canada Recovery Sickness Benefit (CRSB), for example, was barely used at all. The federal government should aim for new one-time benefits to be more like CERB and less like the CRSB.

One hybrid approach—where the benefit mostly arrives automatically in Canadians’ bank accounts—would be one that comes with criteria based on data that the CRA already has. For instance, the CRA knows Canadians’ income from last year and, in some provinces, it also knows how much they paid in rent. One could imagine a modified housing benefit where the CRA could use last year’s data on income and rent, along with bank account numbers that eligible people used for previous tax refunds.

The upside of this approach is that the take-up rate would be much higher—yielding much more money for people who need it. There are downsides as well: bank account numbers aren’t necessarily current, people’s economic circumstances can change from one year to the next, and some provinces don’t collect rental information.

Even if the feds don’t want to automatically send money without more verification, they could still do much more targeted outreach to Canadians. The CRA knows income from last year, they know if families have children (for the dental benefit), in some cases they know rent paid (for the housing benefit). Using this data, the agency could easily email Canadians who are likely to be eligible and encourage them to apply. In many cases, the CRA has emails on file or potentially eligible people have the CRA secure messaging service. The agency should be engaging in this type of targeted outreach in tandem with mass media campaigns like the ones they’ve already conducted..

The federal government could also make stronger connections to community groups, tax filing clinics, anti-poverty groups and so on. These groups routinely help people—particularly lower-income individuals and families—navigate Canada’s tax and benefit system.

The federal government did not engage these groups to get the message out for the housing or dental benefit. With federal support, these groups could create pamphlets, seminars, clinics and more. They could help increase take-up rates for lower-income Canadians and get the benefits to more people who need them. But the feds can’t conjure those relationships out of nowhere—they need to pre-exist so they can be rapidly mobilized for the next one-time cash transfer. And these groups should receive federal funding to ensure the long-term success of these programs

Rapidly sending cash directly to Canadians, outside of filing taxes, is very new for governments, as is relying on citizens to accurately fill out attestations.

These approaches have the potential to make governments much more responsive to emerging issues, like inflation or climate emergencies. However, failing to rapidly communicate a program’s existence, eligibility and onerous application is clearly compromising take-up rates—as it did for the dental and (especially) housing benefits.

As the federal government implements version 2.0 of one-time cash transfers, the housing and dental benefits offer something of a cautionary tale. If the feds want to boost take-up rates, they need to take more proactive measures to make sure that every eligible Canadian actually receives the benefits they need.

Thanks to Ricardo Tranjan and Katherine Scott for their comments on an earlier version of this analysis.