CCPA Senior Economist David Macdonald breaks down the numbers by creating a new methodology, which shows that corporate profits are eating up the vast majority of the extra inflation dollars, far outpacing increased labour costs or other expenses.

Our content is fiercely open source and we never paywall our website. The support of our community makes this possible.

Make a donation of $60 or more and receive The Monitor magazine for one full year and a donation receipt for the full amount of your gift.

Executive summary

This report creates a new dataset to better understand what is driving inflation in Canada—workers’ wages, corporate profits, and specific industries. Right now, we largely rely on the Consumer Price Index (CPI) to track inflation. It’s good at telling us which prices are going up or down but does a poor job of telling us why. This paper adopts a GDP deflation approach, which can separate inflation into three broad categories: profits, wages and other. We can also perform this disaggregation down to the industry level.

What this new approach tells us is different from current inflation headlines. Inflationary price increases aren’t ending up in workers’ pockets, they are ending up in corporate profits—particularly in oil, gas and mining.

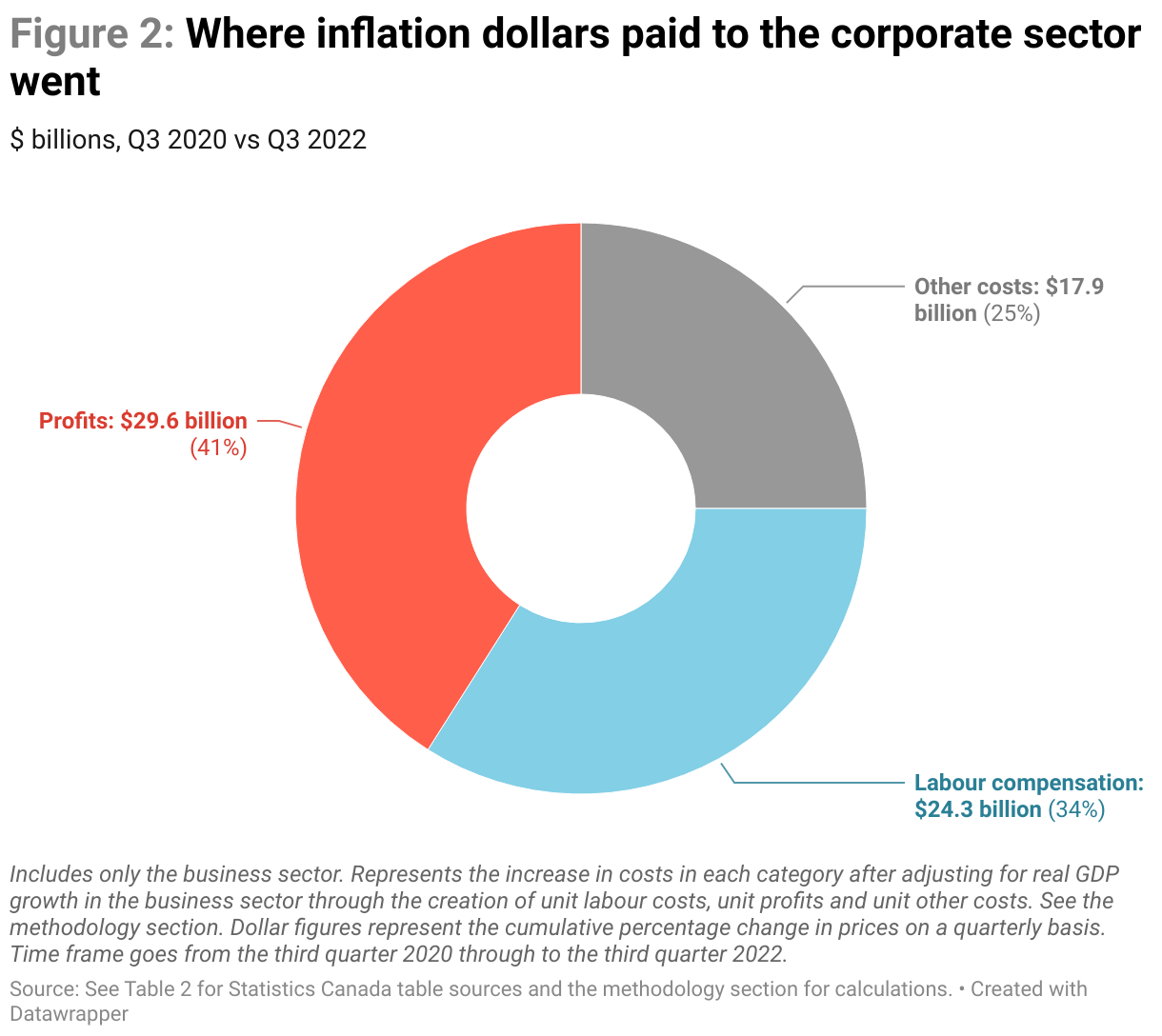

Cumulatively between the third quarter of 2020 and the third quarter of 2022, business prices have risen by 19%. In dollar terms, $72 billion more was sent to the corporate sector in the third quarter of 2022 compared to third quarter of 2020, due to higher prices alone:

- Of that $72 billion, $30 billion ended up as corporate profits.

- Put another way, 41 cents of every dollar spent in higher prices between July and September of 2022 (Q3) was converted into $30 billion in corporate profits.

- A third of that $72 billion—$24 billion—ended up as higher labour compensation without higher output, either through higher wages or more workers required to accomplish the same task.

- The remaining 25% of inflation—$18 billion—ended up as “other costs.”

By far, the largest beneficiary of inflation has been the oil and gas extraction and mining industries:

- Of that $72 billion more in inflation, $18 billion of it ended up in mining and oil and gas extraction. These are inflation dollars only and removes the impact of higher levels of production that can also increase wages and profits.

- Of those $18 billion in inflation dollars flowing to oil, gas and mining, basically all of it ended up on the profits side. Only $656 million ended up in higher worker compensation.

- In a broader sense, 25 cents out of every extra dollar spent on inflation is going straight to higher oil, gas and mining profits.

The second largest industry for receipt of inflation dollars was manufacturing: 13% of every inflation dollar is flowing to this industry, two thirds ($6.6 billion) of which is ending up as profits and one third of which is ending up as higher labour compensation ($3 billion). Manufacturing includes oil refining of crude into gasoline and diesel.

The finance and insurance industries represent the next largest inflation category: Finance and insurance received $7.6 billion of the $72 billion in extra inflationary dollars paid to the business sector in the third quarter of 2022.

Out of the $72 billion in inflation dollars paid in the third quarter of 2022, $29 billion ended up in only three industries: oil/gas/mining, manufacturing and finance/insurance and 40% of all higher prices ended up as profit in just those three industries.

In the 2022 federal budget, a new corporate surtax was applied to the banking and insurance industries, one of the three industries that have been taking over half of every inflationary dollar spent and declaring it as profit. However, this surtax has yet to be applied to the other two industries—oil, gas and mining and manufacturing, including refining—that have been converting inflationary benefits into corporate profits. Companies profiting from inflation are the best candidates for a surtax because these profits are pure rent seeking without productive merit. The proceeds for a corporate surtax can be recycled to help consumers, particularly lower-income households who have to pay those higher prices.

Introduction

There has been plenty of interest in this historic period of inflation in Canada and around the world. The public and the rate-setting Bank of Canada are generally focused on the Consumer Price Index (CPI) as the measure of inflation. There are various versions of the CPI that include or exclude key commodities, like food and energy prices, to get to core inflation or the three versions that the Bank of Canada follows, which attempt to exclude some of the CPI volatility to get to a better underlying inflation figure.1Bank of Canada, Key Inflation Indicators and the Target Range.

The Consumer Price Index and its derivatives can’t tell us where inflation came from, what is driving it and where, ultimately, all of the additional dollars that Canadians are paying in higher prices are going. To understand more about what’s driving inflation, we need a different approach to changing prices rather than just tracking the final price of goods and services sold to consumers. We need a measure of inflationary price changes due to various points along the supply chain by various intermediate industries before higher prices reach consumers.

A different approach to assessing the driving factors behind inflation needs to do so from the perspective of Gross Domestic Product (GDP), which is called the GDP deflator. It follows price changes across the entire economy and not just the change in retail prices for consumers.

There are differences between the CPI and a GDP deflator. The GDP deflator will track the changes in prices if they are sold to consumers (like the CPI does) and if they are sold to other sectors, like other businesses, governments or non-profits. The weighting of price changes is different in the GDP deflator than for the CPI. Whereas the cost of diesel is relatively unimportant in the CPI, since few consumers fuel their cars with diesel, it is much more important and weighted more heavily in the GDP deflator, since this is the primary fuel for long-distance goods transportation for businesses as well as many other industrial uses.

The CPI will track the changing cost of imports, like the changing cost of a TV imported from South Korea, whereas the GDP deflator will only track domestic changes in prices. On the other hand, the GDP deflator includes the changing price of Canadian exports, whereas the CPI does not. The value of exports is relevant in that crude prices, which comprise a big portion of Canada’s exports, are much higher now compared to the start of the pandemic.

Focusing more specifically on the business sector allows us to better isolate where inflation dollars have gone, broken down by profits, labour compensation and other factors, as well as by industry. The business sector is the only sector that generates profits; isolating our focus on that sector allows us to properly separate profit vs. labour factors in inflation. Also, the business sector GDP deflator has risen much faster than the general GDP deflator or CPI (as we’ll see below), further honing in on where inflation dollars have gone. Using a GDP deflator for the business sector is generally the approach of this paper.

The GDP deflator for the business sector will include the price changes of anything sold by the business sector to any other sector. This can include the household sector, which, therefore, will be reflected in the CPI and will also critically include the price of goods and services sold to other businesses, thereby getting at the supply chain issue and clarifying the role that increased input costs play in increasing costs to consumers.

An industry or the economy can create nominal value in two ways: it can increase its output or can increase its prices. Real GDP is a way of measuring changes in output only. It does this by locking prices at a specific level, generally where they stood in 2012. Then if real GDP increases, it can only be because that industry increased its output. The other way that nominal value can be added is if prices rise, i.e. inflation. If nominal GDP is going up at a faster rate than real GDP, then you have inflation and the reason why nominal GDP is rising is because prices are going up, not because production is going up.

Creating the GDP deflator is a simple matter of calculating how much faster nominal GDP is rising compared to real GDP. This can be further extended to profits and wages. If either is growing faster than real GDP (output) then that proportion of the rise is inflationary. These increases in costs in the aggregate are called the GDP deflator but for specific costs they are called the unit cost of labour or the unit profit for changes in nominal total compensation or nominal pre-tax profits.

For example, if you have a gasoline refinery that produces 20% more gasoline because people are out of a lockdown and are buying 20% more gasoline, we might find that both profits and labour compensation rise by 20%. But these increases in profits and payroll aren’t inflationary, they merely reflect higher output. However, if this refinery produces 20% more gasoline but sees profits go up by 30%, then that is inflationary, but only for the final 10%, with the first 20% being due to a change in output (people buying more gasoline). While we may observe profits rising in particular industries, it’s important to adjust those increases for changes in output (or real GDP) to understand which portion of profits are resulting in inflation.

If a gasoline refinery increased its prices by 10% because input prices of buying crude oil went up by 10%, then the refinery can’t be said to have caused inflation since its “value-added” hasn’t changed and neither have labour costs or profit. The GDP deflator of this industry has remained unchanged even though consumer prices have gone up. In this example, it’s not the refining industry that is responsible. This is why we need to track all industries, not just those selling directly to consumers.

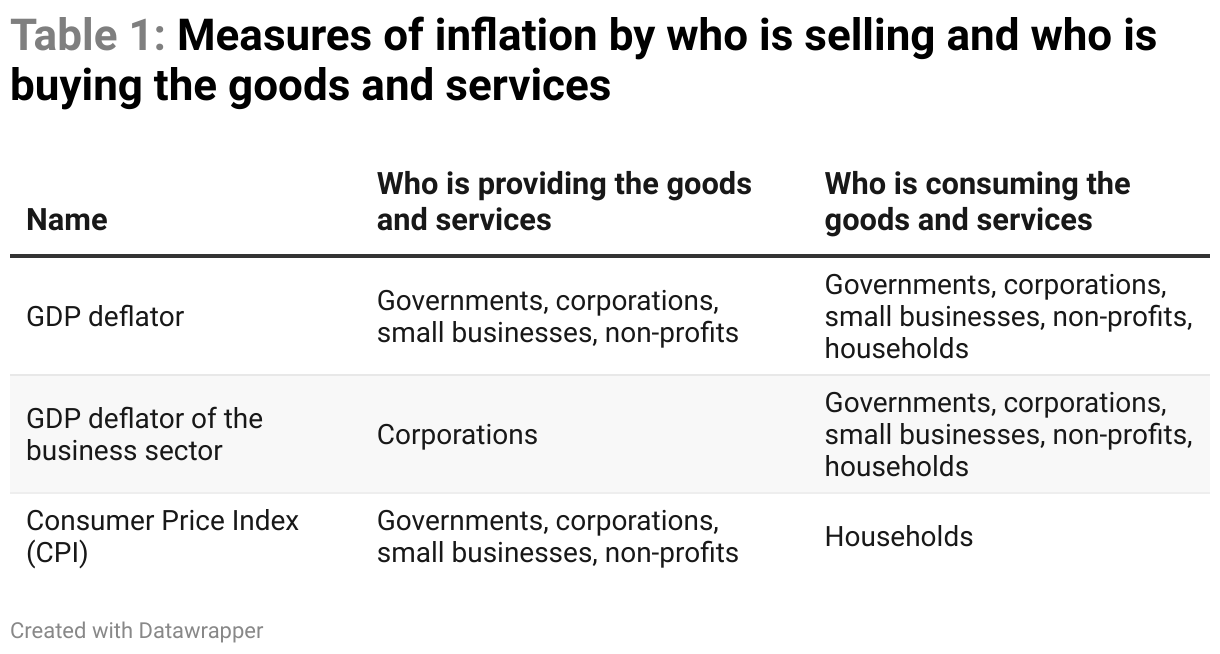

Table 1 examines three types of inflation: the CPI, the GDP deflator, or price changes across the entire economy, and the GDP deflator for the business sector, or price changes occurring from goods and services sold by the corporate sector.

There are tradeoffs in switching to the GDP deflator from the CPI. For instance, the CPI tracks changes in individual retail prices, like comparing the relative price change between potato chips and mortgage interest costs. The GDP deflator doesn’t track individual retail prices but it can apportion inflation by industry and by cost driver categories like wages and profits.

For example, potato chip prices have increased by 14.9% between the third quarter of 2020 and the second quarter of 2022.2Statistics Canada, Table 18-10-0004-01 Consumer Price Index, monthly, not seasonally adjusted. The potato chips and other snack products CPI went from an average of 104.8 in the third quarter of 2020 to 120.4 in the second quarter of 2022. But it is unclear where that extra 15% is ending up. Plenty of attention has been focused on grocery store profits, but maybe grocery stores are just passing on higher prices from potato chip manufacturers. Perhaps potato chip manufacturers are just passing on higher prices from potato farmers. Or maybe all three are passing on their higher prices for diesel to fuel tractors as well as trucks that transport potatoes and chips around the country.

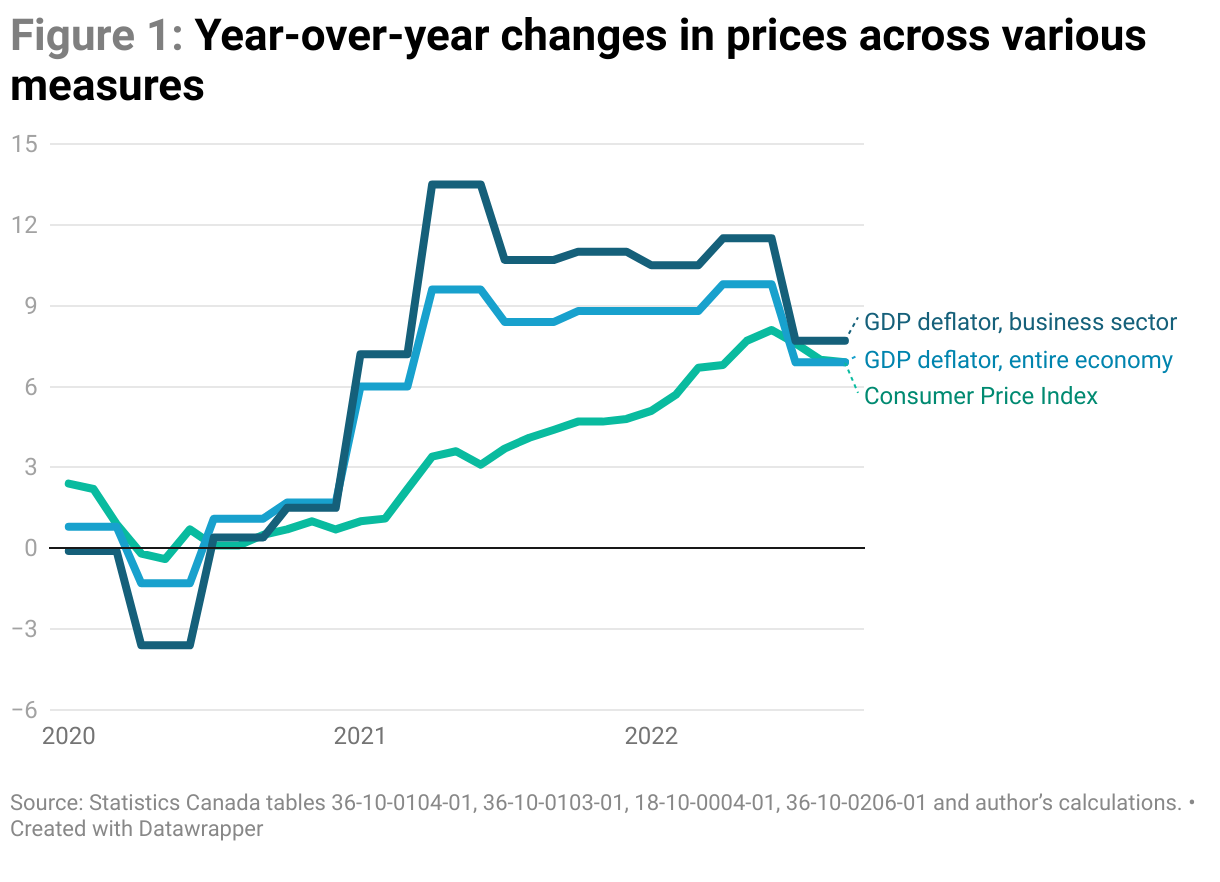

Figure 1 shows all three of these inflation measures on the same year-over-year basis. The GDP figures are only updated quarterly, whereas the CPI data is available monthly. What is immediately apparent is that the GDP deflator approach has shown inflation rising much faster than the final prices that consumers pay in the CPI. While they appear to be converging more recently, it has taken longer for consumers to pay higher prices. The initial rise in the GDP deflator inflation in early 2021 was well before they started showing up in the CPI in 2022. It may be that it takes time for price increases further down the supply chain to reach the final consumers and CPI.

Of the three measures of inflation, inflation in prices from the business sector is the largest. Inflation in the business sector hit 13.5% at the end of the second quarter of 2021, well above the broader GDP deflator, which was only 9.6%. This is also well above the peak so far in CPI inflation of 8.1%, which was reached in June 2022.

Government and non-profit goods and services likely haven’t increased in price as quickly as those in the business sector. This would have the effect of moderating both the CPI and the entire economy’s inflation compared to business sector price inflation. The weighting of price increases likely matters too.

As noted above, the benefit of the GDP deflation approach is that the value-added approach can separate inflation into three broad categories: profits, wages and other. We can also perform this disaggregation down to the industry level.

The GDP deflation approach tracks the nominal “value-added” by each industry instead of a final price. If an industry only passes on its higher input costs as higher prices but doesn’t change the amount of product sold, then there is no change in its contribution to GDP and it isn’t the industry responsible for those higher prices. Its value added has remained unchanged.

Businesses often complain about higher input costs causing them to increase their prices, but this skates around the fact that one business’ input costs is another business’ prices (which sold them their inputs). Energy plays a key role as one of those driving input costs, but Canada is a net exporter of crude oil and generally exports as much as it imports in refined petroleum (like gasoline and diesel).3Statistics Canada, Table 12-10-0121-01 International merchandise trade by commodity, monthly (x 1,000,000). So any hike in gas prices is a hike in money going to Canadian companies across the entire economy.

In terms of the actual data, unit labour costs (inflation due to labour, meaning larger payroll without larger output) are well captured in Canada by industry, by quarter and are updated rapidly, but the unit profits and the broader “other” category contain poor data that is updated less frequently. The exclusive focus on labour costs completely ignores the productivity of corporate profits and whether profits are going up because companies are getting more productive or if they are going up because companies are jacking up prices. If a company is seeing higher profits because it has learned how to produce more with a new technique, this isn’t inflationary, since output has increased potentially as much as profits. On the other hand, if a company is seeing higher profits with the same output, the per unit amount going to profits has increased and this is inflationary. Without better data on profits and other costs, it’s not possible to properly answer the question of where responsibility lies for the present bout of inflation by industry and by category. This paper attempts to build such a series by synthesizing two existing Statistics Canada datasets and examines the preliminary results. See the methodology section for more details.

The “other costs” category can play an important role in some industries and over some quarters in driving or restraining inflation. It is made up of net interest, depreciation and amortization and non-income corporate taxes (indirect taxes) net of business subsidies. The financial parts of interest and depreciation are relatively consistent over time—although in the early days of the pandemic business subsidies swung significantly with the roll out of the Canada Emergency Wage Subsidy. Ideally, these categories would be broken apart to better understand their role in inflation. Unfortunately, the data is insufficient for that purpose and forces their group into an “other costs” category. See the methodology section for more details.

Where are your inflation dollars going: profits or wages?

The third quarter of 2020 marks the rough starting point for the rapid upswing in business GDP inflation and it is the general starting point for this analysis. The most recent data is for the third quarter of 2022. Cumulatively over that period, business prices have risen by 19%. Excluding any re-opening in the economy that caused output to tick upwards, prices alone are 19% higher.

In dollar terms, that means that $72 billion more was sent to the corporate sector in the third quarter of 2022 compared to third quarter of 2020, due to higher prices alone. Of that $72 billion, $30 billion ended up as corporate profits. Put another way, 41 cents of every dollar spent in higher prices between July and September of 2022 was converted into $30 billion in higher corporate profits. A third of that $72 billion—$24 billion—ended up as higher labour compensation without higher output, either through higher wages or more workers required to accomplish the same task. The remaining 25% of inflation—$18 billion—ended up as “other costs.”

It’s worth noting how different this accounting is from common messaging that inflation is somehow workers’ fault and further real wage cuts are required to get us out of inflation. This accounting can cut through that fog and show that over half of every dollar spent in higher prices is ending up as higher corporate profits.

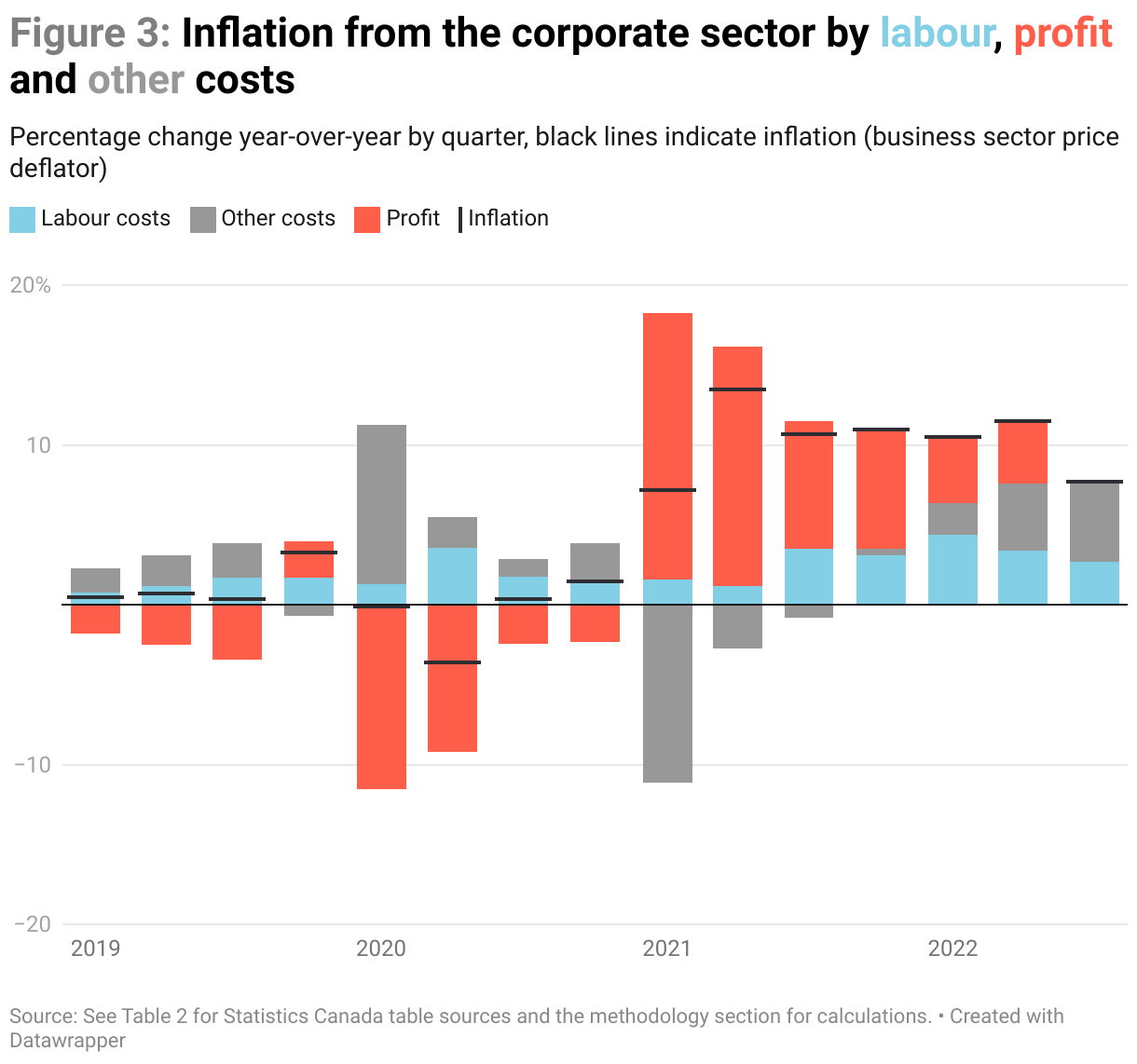

Figure 3 performs the same calculation as Figure 2, but does so on a quarterly, year-over-year basis, which is the approach generally taken with CPI figures. As the pandemic hit in the first two quarters of 2020, business sector inflation dipped into deflation. The profit contribution to inflation dropped below zero. In other words, corporate profits fell faster than output (as measured by real GDP). The initial deflation of 12% in corporate profits was followed by a 17% increase in inflationary pressure by the first quarter of 2021.

In the early stages of the inflation ramp up, “other costs” plays an important role in pushing down business sector inflation. This is likely due to the fact that the financial components of “other costs” don’t fall much even if profits and labour fall during a recession. Net interest costs, depreciation and amortization are relatively constant despite drops in sales. As real GDP fell in the first quarter 2020, these financial components didn’t and they looked to expand relative to real GDP.

Where are your inflation dollars going by industry?

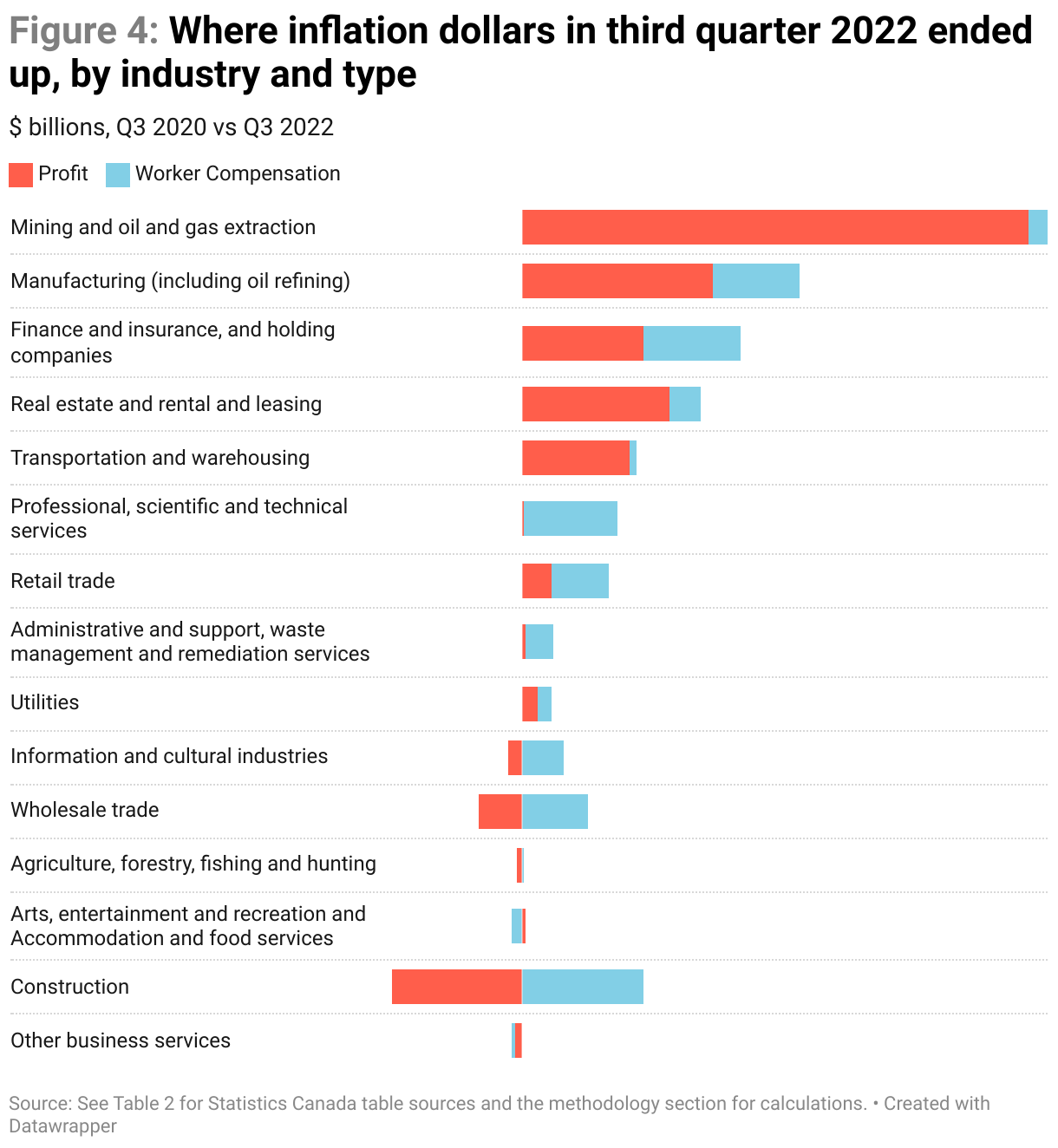

With some limitations, inflation dollars can be further tracked down to the industry level and broken down into the two main cost categories of profits and worker compensation. Unfortunately, at the industry level the impact of other costs can’t be determined due to data limitations. So while the other costs can be determined in the aggregate, they can’t be properly broken down by industry. See the methodology section for more details.

Of the $72 billion additional dollars paid in straight inflation to the business sector by the third quarter of 2022 (compared to the third quarter of 2020), $55 billion can be properly allocated to specific industries. By far, the largest beneficiary of inflation has been the oil and gas extraction and mining industries. Of that $72 billion more in inflation, $18 billion of it ended up here. These are inflation dollars only and removes the impact of higher levels of production that can also increase wages and profits. Of those $18 billion in inflation dollars flowing to oil, gas and mining, basically all of it ended up on the profits side. Only $656 million ended up in higher worker compensation. In a broader sense, 25 cents out of every extra dollar spent on inflation is going straight to higher oil, gas and mining profits.

Clearly, it would be informative to know if those profits are in oil and gas extraction or in the mining sector, as they are aggregated together in this dataset, but the data doesn’t provide details that far down. We can see profit changes in those industries over this period, but there is no way to say whether those profit changes are due to higher output or to higher prices (inflation).

The increase in quarterly profits in the oil and gas extraction and support services between the third quarter of 2020 and the third quarter of 2022 was $20 billion (the industry lost $5.8 billion in the third quarter of 2020 and made $14.2 billion in the third quarter of 2022, a difference of $19.9 billion).4Statistics Canada, Table 33-10-0225-01 Quarterly balance sheet, income statement and selected financial ratios, by non-financial industries, non seasonally adjusted (x 1,000,000). Comparatively, the increase for mining and quarrying sector quarterly profits over that period was much lower, at $362 million.

The second largest industry for receipt of inflation dollars was manufacturing: 13% of every inflation dollar is flowing to this industry, two thirds ($6.6 billion) of which is ending up as profits and one third of which is ending up as higher labour compensation ($3.1 billion). As with the first industry, it would be nice to know which sub-industries of manufacturing are getting all of these inflation dollars and declaring them as profits. The dataset does not provide any detail below the broad manufacturing grouping. Raw profits are available in more detail but we cannot know which part of profits was due to higher production (non-inflationary) and which was due to higher prices (inflationary).

The largest increase in raw quarterly profits within the manufacturing sector was in petroleum and coal product manufacturing, which includes oil refining. Here, quarterly profits rose by $3.6 billion5Statistics Canada, Table 33-10-0225-01 Quarterly balance sheet, income statement and selected financial ratios, by non-financial industries, non seasonally adjusted (x 1,000,000) between the third quarter of 2020 and the third quarter 2022. The next largest manufacturing industry for quarterly profit increases was pharmaceutical/ medicine/ soap/agricultural chemical/paint manufacturing ($2.5 billion), followed by wood product and paper manufacturing ($1.7 billion). The oil refining industry illustrates the importance of parsing increased profits by their source: production or price increases (inflation). Certainly, there was more gasoline produced in the third quarter of 2022, as many more people were driving. However, the price of gas was also higher. A portion of the $3.6 billion higher profits in this industry is due to production (non-inflation) and a portion is due to price increases (inflationary). The Statistics Canada data isn’t detailed enough to break these apart.

The finance and insurance industries represent the next largest inflation category: finance and insurance received $7.6 billion of the $72 billion in extra inflationary dollars paid to the business sector in the third quarter of 2022. This includes the entirety of the financial and insurance industries. While it would be interesting to see which sub-sectors are causing this—for instance, big banks or insurance companies—this is as much detail as the data allows.

It’s worth pausing here and pointing out that of the $72 billion in inflation dollars paid in the third quarter of 2022, $29 billion ended up as profits in only three industries: oil and gas, mining, manufacturing and finance/insurance. Earlier, it was pointed out that 41% of all higher prices ended up as profits, but it’s much more concentrated than that: 40% of all higher prices ended up as profit in just those three industries.

There has been plenty of attention paid to the role that grocery stores might be playing in driving food inflation. Unfortunately, they are aggregated into a much larger “retail trade” category, preventing this analysis from weighing in on whether the doubling of profits is caused by higher outputs (people buying more groceries and eating out less) or by jacked-up prices.6David Macdonald, “Pressure’s on Canada’s grocery giants”, the Monitor, October 27, 2022. This sort of data is available in the United States, but not in Canada—though it could be.

The industries in which higher worker compensation drove inflation are also worth examining. These are industries in which workers’ wages rose and/or more workers were required to accomplish the same output for some reason.

The construction industry was in an odd situation: profits were decreasing while output was increasing, meaning profits helped to pull down inflation while worker compensation pushed the other way. That means the industry, on the whole, made almost no contribution to inflation, with lower inflationary profits offsetting inflationary worker compensation. This may have been due to the starting point of the third quarter of 2020, which saw a large upswing in home price speculation. Nonetheless, it’s worth examining the potential sources for inflationary changes in worker compensation by examining payroll changes, with the proviso that we can’t separate payroll increases into productive vs. inflationary. Building equipment contractors constituted the largest sub-industry for payroll changes, followed by residential building construction.7Using average weekly earnings including overtime x employment for all employees. Statistics Canada, Table 14-10-0220-01 Employment and average weekly earnings (including overtime) for all employees by industry, monthly, seasonally adjusted, Canada. In terms of occupations, by far the largest increase in payroll was in middle-management occupations in trades, transportation, production and utilities—more so than in the industrial, electrical and construction trades category, which is the largest employer in this industry.8Custom tabulations, Statistics Canada, Labour Force Survey, public use microdata file, average third quarter 2020 vs. average third quarter 2022. Payroll calculated as usual hourly wage x actual hours worked at all jobs. It is possible that management costs increased substantially without adding to output and is, therefore, inflationary. Had those management costs not materialized, prices may have been lower or more money could have gone to corporate profits.

Finance, insurance and holding companies saw the second highest inflationary increase in labour compensation, amounting to $3.4 billion by the third quarter of 2022. Professional, scientific and technical services were third, with an inflationary increase in labour compensation of $3.3 billion compared to two years earlier.

As with analysis of profits above, it would be interesting to drill further down to determine which sub-components of various industries are seeing higher growth in worker compensation compared to output. But, like the profit figures, we can only get hints of what might be driving it without knowing how much is due to higher production and how much is inflationary.

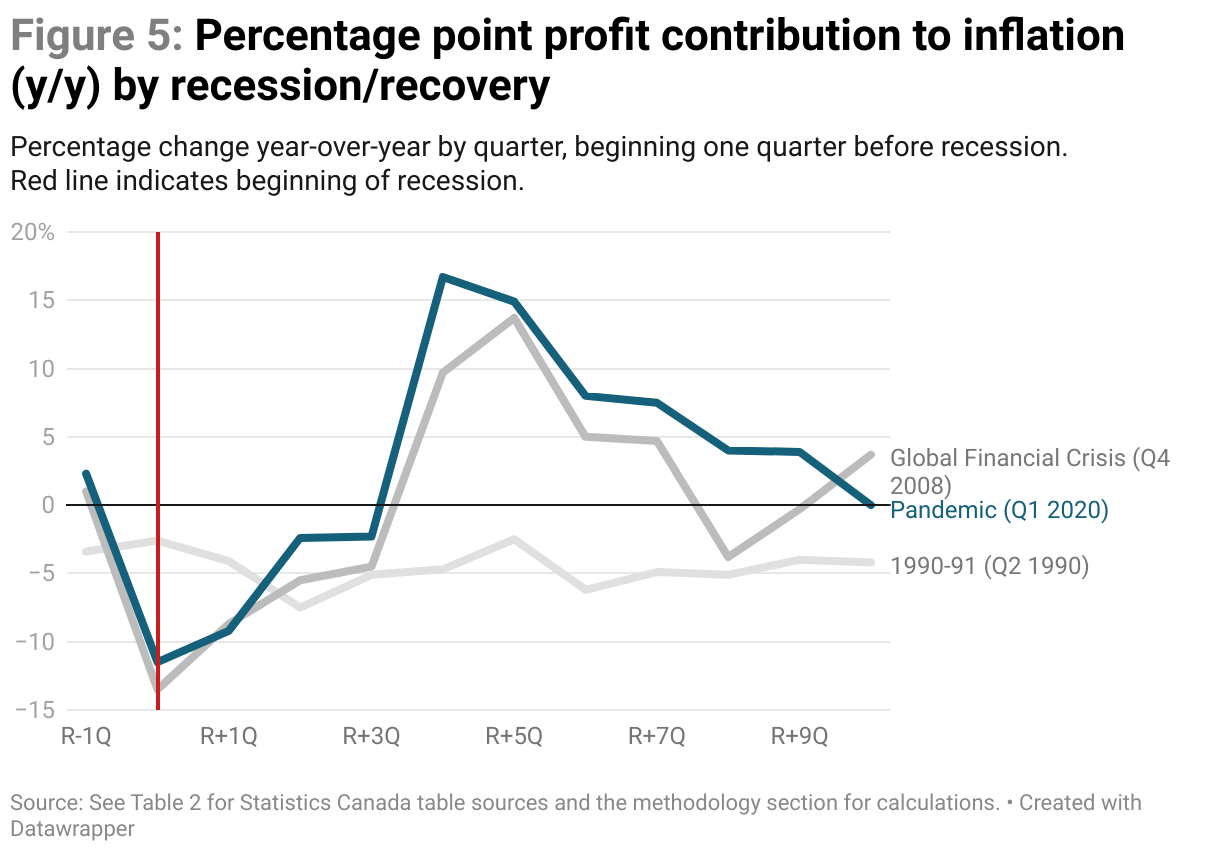

Inflation drivers over the past three recessions

There are common trends in recessions when it comes to profits and wages: profits drop faster than wages but rebound much faster. The data set for this paper only goes back to 1988. However, within this period, there are three recessions to examine: the 1990–91 recession, the global financial crisis (GFC) and the pandemic recession. This section looks at the GDP deflator for the business sector, which is broken down by profits and worker compensation across these three recessions.

At almost every quarter, corporate profits during the pandemic recession and recovery were contributing more to inflation than in any other recession. The profits percentage point contribution to inflation peaks at over 15 percentage points four quarters after the pandemic hits.

During both the 2008–09 global financial crisis and the 2020–21 pandemic recession there was plenty of inflation that went to corporate profits, but during the 1990–91 recession there was almost no inflation pressure from corporate profits. Put another way, during the global financial crisis and pandemic recoveries, profits rose much faster than output (real GDP) in the business sector.

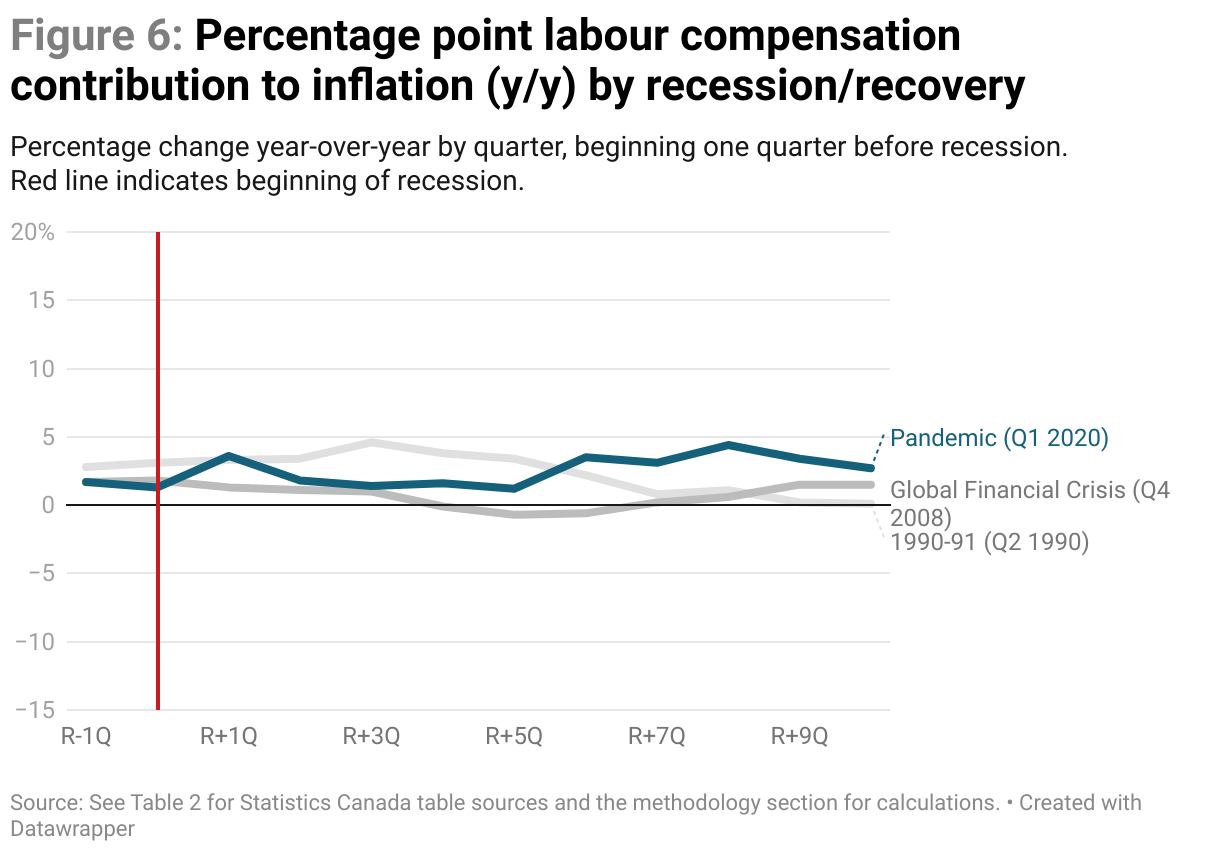

Figure 6 is on the same scale as Figure 5 to highlight how labour compensation is much less important in explaining inflation, regardless of any recessionary period. During the global financial crisis of 2008–09, wages played a particularly unimportant role in driving inflation for the business sector; when profits were driving inflation (at the fourth and fifth quarter after the recession started) wages actually became deflationary.

In the first year-and-a-half of the pandemic, workers’ compensation was adding less to inflation than during the global financial crisis. However, by the third quarter of 2021 (R+6Q), workers’ compensation pressure on inflation exceeded the other two recessions. Again, workers’ compensation was a far less important contributor to inflation in the business sector than profit, but it was still higher, reflecting a tight labour market following the pandemic re-opening.

Conclusion and policy recommendations

Canada needs a new dataset that combines the unit cost of labour and unit profits of the business sector as a whole and by industry in order to glean deeper insight into where inflation dollars go. To properly understand inflation, the focus needs to be broadened from the change in the retail price of goods and services sold to consumers to include the entirety of the business sector. Policy-makers need to understand the changes in the intermediate prices all the way up the supply chain to better understand the change in the final retail price. Inflation, as judged by the GDP deflator for the business sector, allows us to do that.

Unfortunately, the synthesization of two broad data series from Statistics Canada isn’t ideal, as discussed in the methodology section. A properly constructed series on unit costs for labour and profits—including the components that make “other costs” like net interest, depreciation, indirect taxes and subsidies—is critical for further study. Given the turmoil that inflation is causing in Canada, Statistics Canada should endeavour to produce such a series on the business sector in the aggregate and at the subsector level, or three-digit NAICS, as is available in the United States. This would allow a better understanding, for example, of the causes of higher grocery store prices9Ie. NAICS 445: Food and beverage stores. vs. higher gas station prices, which are otherwise grouped together in a broad “retail trade” category.10Ie. NAICS 447: Gasoline stations.

Since 2020, inflation dollars have gone more to corporate profits than to labour compensation. On the corporate profits side, only three industries—oil and gas, mining, manufacturing and financial services/insurance captured almost all of the inflation dollars. On the labour side, the largest inflationary industry was construction, where there seems to be an explosion of management costs related to residential construction.

Inflation places a heavy burden on Canadians and most of it is ending up in corporate profits. The surge in international prices of oil, gas and refined petroleum products, such as gasoline and diesel, has driven inflation as well as profits for Canadian corporations operating in these sectors. The reasons for these higher profits have nothing to do with Canadian companies—they were driven by international events like Russia’s illegal war in Ukraine.

In the 2022 federal budget, a new corporate surtax was applied to the banking and insurance industries, one of the three industries that have been taking 40% of every inflationary dollar spent and declaring it as profit. However, this surtax has yet to be applied to the other two industries—oil, gas and mining and manufacturing, including refining—that have been converting inflationary spending into corporate profits. Companies profiting from inflation are one of the best candidates for a surtax because these profits are pure rent seeking without productive merit. The proceeds for a corporate surtax can be recycled to help consumers, particularly lower-income households that have to pay those higher prices.

Despite the clear harm that rampant inflation is causing Canada’s economy and the macroeconomic disruption it entails, there is too little focus on the causes: mainly, high oil and transport fuel prices for Canadians. Natural gas and electricity companies are not allowed to profit off of Canadians like oil companies are due the recognized deleterious effect of high prices for these inputs. The Atlantic provinces and Quebec regulate gasoline prices to consumers, which at least examines allowable margins for wholesalers and retailers, even though it doesn’t protect consumers from feedstock price increases.11Natural Resources Canada, Why Canada Doesn’t Regulate Crude Oil and Fuel Prices. It is time to start examining these types of controls further up the energy supply chain to the producers of crude and refiners for Canadian markets. Prior to 1985, various export and import limits were placed on these commodities in Canada. Given the damaging impact of inflation on our economy today, driven in large part by these industries, it is time to re-examine these policies. This could allow Canadian companies to enjoy fair margins on their products in Canada without driving the dangerous inflationary spiral that we’ve seen over the past two years.

Methodology

The focus of this report, unless otherwise noted, is on price changes in the corporate sector of the Canadian economy, which excludes small businesses that are considered “mixed income” in the GDP accounts. It also excludes price changes for goods and services provided by government and non-profits.

The goal of this analysis is to construct a data series that calculates a unit cost of labour, unit profits and other unit costs. The general formula for income-based GDP in the business sector is:

GDP of the business sector = labour compensation + profits + net interest income + depreciation + indirect taxes less subsidies

In this paper, wages and profits could be reliably separated, but the other cost drivers were grouped into an “other costs” category.

The GDP deflator approach divides the nominal value of the item in question (profits or compensation or GDP) by real GDP in a given industry to create an index. The GDP deflator grows if the nominal value of the item in question is increasing faster than output, as judged by real GDP. Unit cost of labour or unit profits are simply nominal total compensation / real GDP and nominal pre-tax profits / real GDP. The general GDP deflator is nominal GDP / real GDP. Adding up the unit costs of labour, unit profits and unit other costs produces the GDP deflator.

In order to properly calculate the parts in the aggregate for the business sector or for a particular industry, we need real GDP, nominal pre-tax profits, nominal total labour compensation and either nominal other costs or nominal GDP (from which other costs can be calculated as a residual). A consistent data series containing all of these pieces isn’t available in Canada, but is available in the United States, both in dollar terms as well as indexes at unit costs.12From NIPA Table 1.15. See tab T11500-Q U.S. Bureau of Economic Analysis, National Income and Product Accounts, Section 1, “Table 1.15 Price, Costs, and Profit Per Unit of Real Gross Value Added of Nonfinancial Domestic Corporate Business”. The American series is much more detailed in terms of industries, with the Canadian data only available at the two-digit NAICS level, whereas American data is available at the three-digit level.

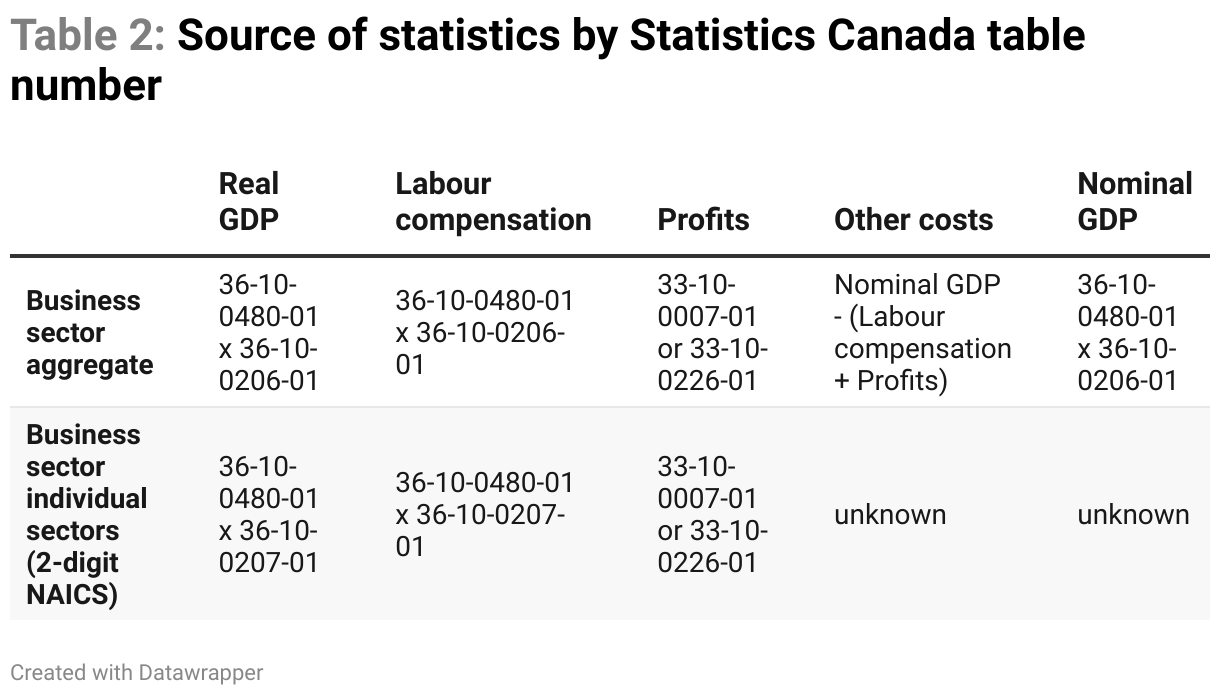

A consistent series in Canada had to be constructed with each variable obtained from the Statistics Canada tables, as outlined in Table 2. In general, two data series are combined: one looking at labour productivity, which contains nominal GDP, real GDP and total labour compensation, and one looking at corporate income statements, which contains corporate profits.

In the aggregate for the business sector and by industry, annual dollar values are available for real GDP, nominal GDP (with a significant lag time) and nominal total labour compensation.13Statistics Canada, Table 36-10-0480-01 Labour productivity and related measures by business sector industry and by non-commercial activity consistent with the industry accounts. For the business sector as a whole, seasonally adjusted quarterly indexes exist in a separate table, which allows for the creation of a quarterly series of nominal total compensation, real GDP and nominal GDP for the business sector as a whole.14Statistics Canada, Table 36-10-0206-01 Indexes of business sector labour productivity, unit labour cost and related measures, seasonally adjusted.

However, the missing piece is still corporate pre-tax profits, which are unavailable in a reconciled way in these labour productivity tables. However, nominal corporate profits exist in a set of quarterly corporate income statement tables. There is an unfortunate series break across all corporate income statement tables between the fourth quarter of 2019 and the first quarter of 2020. Prior to the first quarter of 2020, corporate profit before income tax is only available without seasonal adjustment.15 From the first quarter of 2020 onward, corporate income or loss before income taxes are available in a different table, seasonally adjusted.15Statistics Canada, Table 33-10-0226-01 Quarterly balance sheet and income statement, by industry, seasonally adjusted (x 1,000,000).

Parts of this data series disaggregating the GDP deflator into its parts of labour compensation, profit and other costs can be calculated down to the industry level within the business sector. Again, real GDP and nominal total labour compensation are available from the labour productivity tables, and profit from the income statement tables. However, we don’t know nominal GDP by industry in the business sector and there is no other reliable way of calculating it. As such, we don’t know the contribution of “other costs” to inflation by industry and that part of inflation at the industry level appears as “unknown” in Figure 4 as a result.

Despite missing the “other costs” contribution for each industry, we can still calculate the unit costs of labour and unit profits by industry because we have real GDP as well nominal total compensation and nominal pre-tax profits by industry.

There are also some industry match up issues between the labour productivity and income statement datasets. The industries of educational services as well as health care and social assistance have profit data but are missing labour productivity data for real GDP and labour compensation (in Table 36-10-0207-01) and so that had to be excluded from the industry breakdown. These excluded industries are also grouped in the unknown bar in Figure 3. Profits from holding companies (NAICS 55) don’t seem to be properly included in the income statement tables, although their total compensation does seem to be included on the labour compensation side. Both datasets do seem to have finance and insurance companies.

Obviously, a data series on unit costs consistent across all cost categories and industries would be preferable. Statistics Canada should produce such a table to erase the inconsistencies discussed above. The odd bias toward labour and its productivity excludes the productive or non-productive outcomes for profits and other costs. It is a disservice to only report statistics on workers and not include profits, particularly given the preliminary results of the importance of unit profits in driving the GDP deflator of the business sector.

As a check on the compatibility of combining the labour productivity and the income statement data series, it is worth comparing these series where they overlap. Re-arranging the equation in the business sector for nominal GDP above and moving the terms available from the labour productivity series to one side and those available from the income statement to the other, we arrive at the following:

Nominal GDPLabour productivity– labour compensationLabour productivity = ProfitIncome statement + net interestIncome statement + depreciationIncome statement

Each side of this equation should represent non-labour costs. The one key term that’s missing is indirect taxes less subsidies. This isn’t known consistently on the income statement side. In some cases, subsidies are reported in the income statement tables for non-financial companies, although not prior to 2020. They aren’t broken out at all for financial companies and, in any case, are never available on a seasonally adjusted basis.

On the labour productivity side, nominal GDP is reported at basic prices, excluding the impact of indirect taxes and subsidies. Given the size of federal supports, like the Canada Emergency Wage Subsidy, for the business sector during the pandemic, which were considered “subsidies”, properly disaggregated data would be interesting to review.16Statistics Canada, Table 36-10-0687-01 Federal government COVID-19 support measures in the System of Macroeconomic Accounts, quarterly (x 1,000,000).

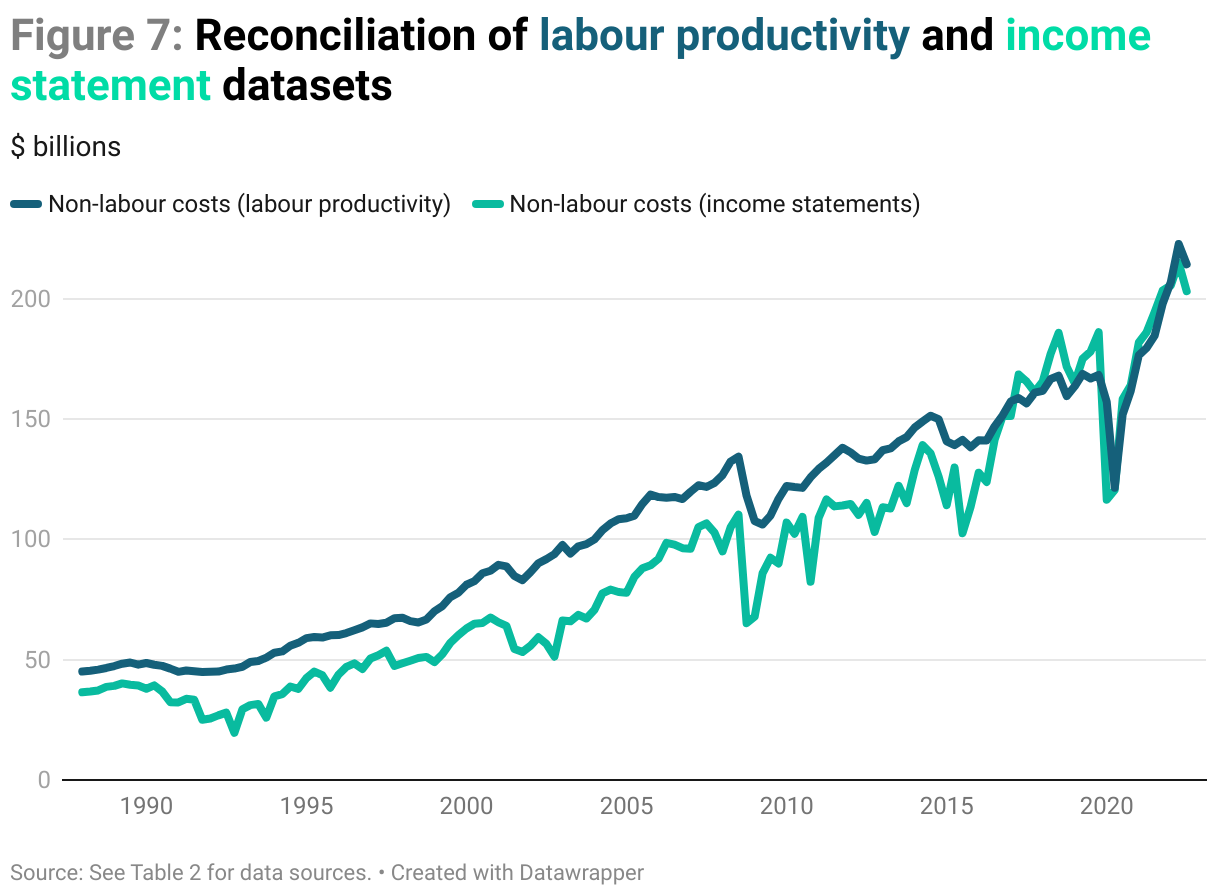

Figure 7 graphs the results of the above equation with a line for the labour productivity data and a second for the income statements in the business sector. Clearly, the two series where they overlap are measuring something similar, although not exactly the same. Some of the differences include:

- Labour productivity is seasonally adjusted but income statement data prior to the first quarter of 2020 is not.

- Depreciation on income statements likely has a different definition than in the GDP accounts because it includes depletion on the income statement side, which GDP accounts do not.

- Net interest costs in income statements are not available before 2020, at which point only gross interest payments are included in Figure 7.

- As noted above, indirect taxes net of subsidies are included on the labour productivity side but not on the income statement side.

Despite these points, the correlation between these series is high, with an R-squared of 0.94 and the match up in nominal values have been particularly close since 2017. This provides confidence that these two series can be broadly combined in the manner above.

While imperfect, the broad match up of these two series justifies their combination in the calculation of the beneficiaries of inflation dollars, as produced in this paper. While a proper reconciliation would be preferable, hopefully this analysis sets the groundwork for Statistics Canada to produce a consolidated dataset as is already available in the United States.

Acknowledgements

The author would like to thank Sheila Block, Chris Roberts, Jim Stanford and Kaylie Tiessen for their helpful comments on an earlier draft of this paper.

Notes

About the author

David Macdonald

David joined the CCPA as its Senior Ottawa Economist in 2011, although he has been a long time contributor as a research associate. Since 2008, he has coordinated the Alternative Federal Budget, which takes a fresh look at the federal budget from a progressive perspective. David has also written on a variety of topics, from child care to income inequality to federal fiscal policy. He is a regular media commentator on national policy issues, often speaking to the CBC, Globe and Mail, Toronto Star and Canadian Press. David received his BA from the University of Windsor and his MA from the University of Guelph, both in Philosophy. Follow David on Bluesky at @davidmaccdn.bsky.social